At its core, Unrelated Business Taxable Income (UBTI) is the income a tax-exempt organization generates from activities that aren't directly tied to its core mission. Think of it this way: while the income from your main, mission-driven work is tax-free, any profits from a "side hustle" that looks and acts like a commercial business could be taxed.

This whole concept was created to keep things fair. It prevents a nonprofit from using its tax-exempt status to gain an unfair advantage over for-profit businesses doing the exact same thing.

The Core Concept of Unrelated Business Income

For anyone leading a nonprofit, getting a firm grip on UBTI is fundamental to staying compliant and making smart financial decisions. It’s a common mistake to assume that as long as you pour the profits back into your mission, the activity that generated them is automatically tax-exempt. That’s just not how the IRS sees it.

Let's use a real-world example. Imagine a tax-exempt animal shelter that decides to open a public pet grooming salon. The salon is a big success, and all the profits go directly to supporting the shelter's rescue operations. Even so, that grooming service is a commercial venture competing head-on with local for-profit groomers who have to pay taxes. The income from that salon would almost certainly be flagged as unrelated business income.

Why Does the IRS Tax This Income?

The logic here is all about leveling the playing field. If a nonprofit could run a commercial business tax-free, it could easily undercut the prices of its for-profit competitors, creating an unfair market. The tax on unrelated business income ensures that when a nonprofit steps into the commercial world, it plays by the same rules as every other business.

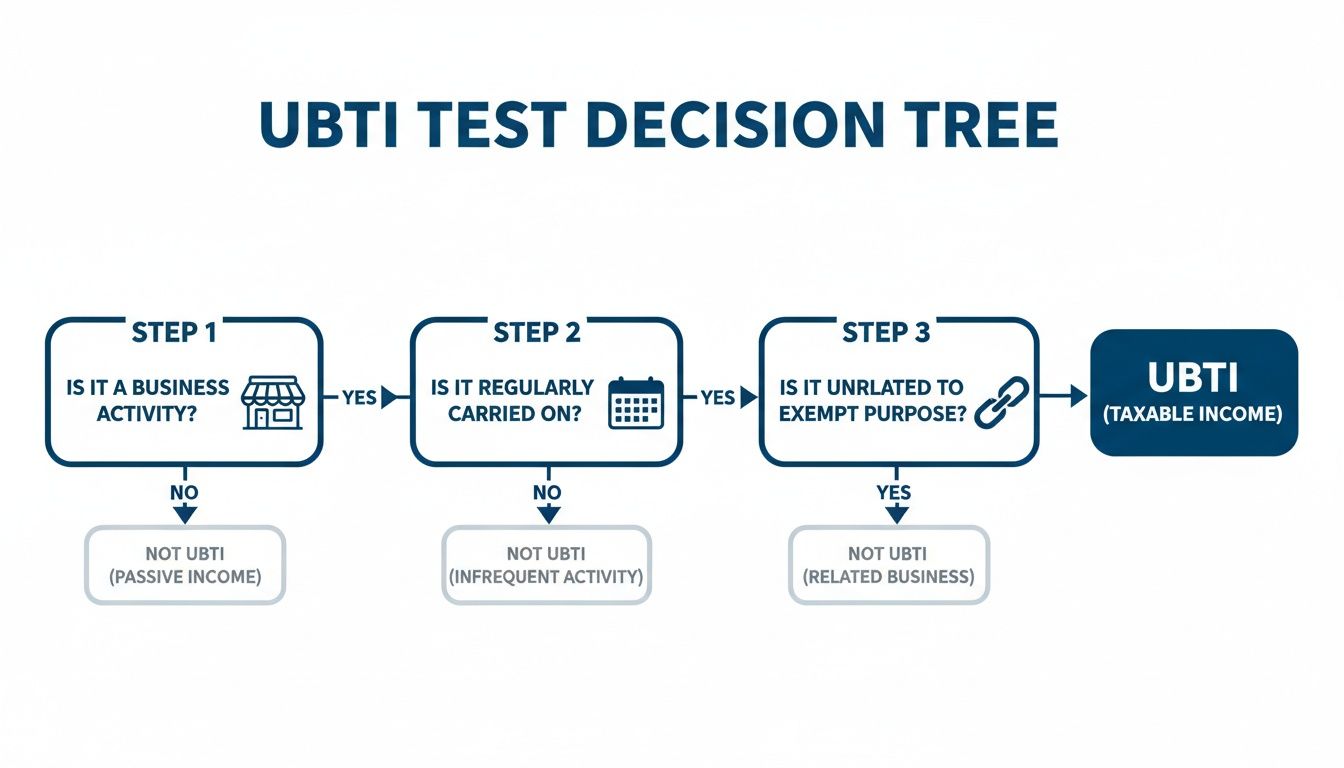

To figure out if an activity triggers UBTI, the IRS uses a simple three-part test. For an activity's income to be considered unrelated, it must meet all three of these conditions.

The IRS has a clear, three-part test to determine if an activity generates unrelated business income. It's not about what you do with the money, but about the nature of the activity itself. Let's break it down.

| The UBTI Three-Part Test At a Glance | ||

|---|---|---|

| IRS Criteria | What It Really Means | A Simple Example |

| It is a trade or business. | The activity involves selling goods or services to generate income, just like a regular for-profit company. | A university bookstore selling computers and software to the general public, not just students. |

| It is regularly carried on. | You're doing this activity consistently, not just as a one-off fundraiser. It looks like a normal business operation. | A museum operating a public parking lot every single day, year-round. |

| It is not substantially related to the organization's exempt purpose. | The business activity itself doesn't contribute importantly to achieving your mission (beyond providing funds). | A children’s charity selling advertising space in its monthly journal to car dealerships. |

If your organization has an activity that checks all three of these boxes, the net income from it is subject to tax. Understanding this framework is absolutely critical for protecting your organization’s financial health and, ultimately, its tax-exempt status.

Applying the IRS Three-Pronged Test for UBTI

So, how does the IRS actually decide if a nonprofit's side hustle is taxable? They use a surprisingly straightforward, three-part test. Think of it as a series of hurdles an activity must clear. If it stumbles on any one of them, the income it generates is not considered UBTI. But if it clears all three, you're looking at a tax liability.

This simple decision tree lays out the path the IRS follows. As you can see, you only get to the end if the answer is "yes" every step of the way.

If you hit a "no" at any point in this process, the analysis stops, and the income is not UBTI. It’s only when an activity checks all three boxes that it triggers the tax.

Prong 1: Is It a Trade or Business?

First, the IRS asks a simple question: are you selling goods or services to make money? This isn't about whether you actually turn a profit, but whether the activity is set up with a profit motive, just like any commercial enterprise.

Take a university that runs a laundromat on campus for students. They’re providing a service for a fee. That's a classic trade or business. The IRS is looking for the kind of commercial character that puts you in the same arena as for-profit companies.

Prong 2: Is It Regularly Carried On?

Next up is the "frequency" test. Is this a one-off fundraiser or an ongoing commercial venture? To be considered regularly carried on, an activity has to happen often enough and with enough continuity to be comparable to how a for-profit business would operate.

Let’s put this into practice:

- Annual Gala: A once-a-year fundraising dinner doesn't fit the bill. It’s an isolated event, a far cry from a restaurant that’s open every night.

- Weekly Bake Sale: If your nonprofit sets up a bake sale at the farmer's market every single Saturday, you're likely crossing into "regularly carried on" territory. That consistency starts to look a lot like a commercial bakery's operation.

- Parking Lot Operation: A historical society that runs a public parking lot next to its museum every weekend is a textbook example. Since for-profit lots operate with similar frequency, this is a clear "yes."

The real question here is this: "Does the way we run this activity put us in direct competition with taxable businesses?" If the answer is yes, you've met the "regularly carried on" standard.

This is why the annual Girl Scout cookie sale, despite its massive scale, generally avoids this classification. It’s a short-term, seasonal campaign, not a year-round cookie shop.

Prong 3: Is It Substantially Unrelated to Your Mission?

Here’s where things get tricky. This final prong is often the most subjective part of the test. An activity is substantially related only if it directly contributes to your organization’s tax-exempt purpose in a meaningful way—and no, just making money for the mission doesn't count.

The activity itself has to further your cause.

Let's use a museum gift shop to see this in action:

- Related Sales: Selling prints of the art on display, books about the artists, or educational kits tied to an exhibit are all substantially related. These items enhance the visitor's experience and directly support the museum's educational mission.

- Unrelated Sales: Now, what if that same gift shop starts selling generic city souvenirs, branded coffee mugs, or t-shirts with no connection to the art? That income is almost certainly UBTI. These sales are purely for generating revenue and do nothing to advance the museum's core purpose.

Don't underestimate the financial impact of getting this wrong. In 2017 alone, over 80,000 exempt organizations filed Form 990-T, reporting a staggering $15.4 billion in gross unrelated business income and paying $871.4 million in taxes. You can discover more insights about what not-for-profits need to know about UBIT in our detailed guide.

Successfully navigating this three-pronged test comes down to careful analysis and, crucially, solid documentation. The best way to defend your revenue streams is to keep detailed records that show exactly how an activity contributes to your exempt purpose.

Common UBTI Sources and Key Exemptions

Knowing the three-part test for UBIT is one thing; seeing how it plays out in the real world is another. Identifying potential unrelated business taxable income is often a matter of spotting common patterns that the IRS tends to focus on. Some revenue streams, from selling ad space to renting out a mortgaged building, are simply more likely to raise a red flag.

At the same time, the tax code carves out some powerful exemptions that act as safe harbors for nonprofits. Understanding where the IRS draws these lines is the key to structuring your activities smartly. It’s all about striking that delicate balance between generating much-needed revenue and staying true to your tax-exempt mission.

Frequent Triggers for Unrelated Business Income

While the specifics always matter, some activities show up on Form 990-T filings over and over again. These are the areas where nonprofit leaders absolutely need to tread carefully.

1. Paid Advertising Revenue

This is probably the most common UBTI culprit out there. If your organization sells ad space in its journal, on its website, or in a program guide, that income is generally taxable. The critical difference here is between advertising and qualified corporate sponsorship. Advertising actively promotes a company's products or services, whereas a sponsorship is just a simple acknowledgment of their support.

2. Sales of Merchandise Unrelated to Your Mission

Just like our museum gift shop example, selling items that don't directly further your exempt purpose will generate UBTI. An environmental group selling branded reusable water bottles is likely in the clear. But if that same group started selling smartwatches? That’s almost certainly taxable. The product itself must have a tangible connection to your core mission.

3. Income from Debt-Financed Property

This one trips up a lot of organizations. Passive rental income is normally exempt from UBIT, but that protection vanishes if the property has a mortgage. If you own a building with an outstanding loan and rent it out, a portion of that rental income becomes taxable. The taxable percentage is directly tied to the ratio of the outstanding debt to the property's cost basis.

The Good News: Key Statutory Exemptions from UBTI

Fortunately, the IRS has built several clear exemptions into the tax code. These carve-outs can shield certain income from tax, even if it looks like it would fail the three-part test. For savvy financial planners, these are essential tools.

The big idea behind most exemptions is that the activity is either inherently passive or it relies on resources—like volunteer labor or donated goods—that don't create an unfair advantage over for-profit businesses.

Let's walk through some of the most important safe harbors.

-

Activities Run by Volunteers: If an activity is performed with substantially all volunteer labor (the IRS generally considers this 85% or more of the work), the income it generates is exempt. The classic example is a church bake sale run entirely by volunteers; all the profits are tax-free.

-

Sale of Donated Merchandise: Any income you make from selling merchandise that was 100% donated is not considered UBTI. This is the bedrock principle that allows thrift stores run by groups like Goodwill or The Salvation Army to operate tax-free.

-

For the Convenience of Members: A business activity that exists mainly for the convenience of your members, students, patients, or employees is exempt. Think of a hospital cafeteria serving staff and visitors or a university bookstore selling textbooks and school supplies to students.

-

Qualified Sponsorship Payments: As we touched on earlier, payments from corporate sponsors are not UBTI as long as you don't provide a "substantial return benefit" beyond using their name or logo. This allows you to build valuable fundraising partnerships, but you have to be careful not to cross the line into providing actual advertising services.

Common Taxable Activities vs Exempt Income Sources

To make this distinction even clearer, it helps to see some common examples side-by-side. The left column shows activities that often create a tax liability, while the right shows income sources that are generally safe.

| Potentially Taxable Activity (UBTI) | Generally Exempt Income (Not UBTI) |

|---|---|

| Selling paid advertisements in a monthly journal or on a website. | Receiving qualified corporate sponsorship payments for an event. |

| Operating a gift shop that sells items unrelated to the organization's mission. | Selling merchandise that was entirely donated to the organization (e.g., a thrift store). |

| Renting out office space in a building that has an outstanding mortgage. | Collecting rent from real estate that is owned free-and-clear (no debt). |

| Providing travel tour services to the general public for a fee. | Running a fundraising event where substantially all the work is done by unpaid volunteers. |

| Selling data or mailing lists to commercial entities. | Earning passive income from dividends, interest, or royalties. |

| Operating a public parking lot on weekdays that competes with commercial lots. | Operating a business primarily for the convenience of members or employees, like a university staff fitness center. |

Of course, the details of each situation matter immensely, but this table gives you a solid starting point for spotting potential red flags in your own revenue streams.

The Power of Passive Income

Perhaps the most significant exemption for many organizations, especially those with endowments, is the one for passive investment income. The tax code generally excludes this revenue from UBIT because it doesn't involve active competition with commercial businesses.

This protection allows nonprofits to grow their financial reserves without tax getting in the way. Key types of exempt passive income include:

- Dividends and Interest: Earnings from stocks, bonds, and savings accounts.

- Royalties: Income from licensing intellectual property like patents, copyrights, or mineral rights.

- Certain Rents: Income from renting real property, so long as it isn't debt-financed and you aren't providing significant personal services (like hotel-style maid service).

- Capital Gains: Profits from selling property, unless that property is inventory you regularly sell to customers.

By getting a firm handle on both the common triggers and the powerful exemptions, you can shift from worrying about UBIT to proactively managing it. This knowledge turns the complex rules of what is unrelated business taxable income from a potential landmine into a manageable part of your financial strategy.

How to Calculate and Report UBTI

Once you've identified an activity that generates unrelated business income, the real work begins: figuring out what you actually owe. This isn't just about adding up the revenue. It’s a careful process of pinpointing and subtracting all the legitimate expenses to land on your final taxable income.

The basic formula for Unrelated Business Taxable Income (UBTI) is pretty simple on the surface:

Gross Income from Unrelated Business – Directly Connected Deductions = Unrelated Business Taxable Income

The net amount is what you'll be taxed on. But the devil, as they say, is in the details—specifically, in what counts as a "directly connected deduction." This is where meticulous record-keeping goes from being a good habit to an absolute necessity. It's your best defense for minimizing your tax bill and backing up your numbers if the IRS comes knocking.

Calculating Your Taxable Income

The heart of the UBTI calculation lies in subtracting the costs you incurred to run the unrelated activity. For an expense to be deductible, it needs to have a direct, causal link to earning that income. It can't be a fuzzy, indirect relationship.

Let’s go back to our nonprofit gift shop example. The obvious, clear-cut deductions would be things like:

- The cost of goods sold (what you paid for the merchandise).

- Salaries for the employees who only work in the gift shop.

- Marketing costs spent specifically to promote the shop's products.

But things get tricky when you have shared expenses. What about the building's rent? Or the salary of an executive who splits their time between mission-related programs and overseeing the gift shop? You can't just deduct the whole amount. You have to allocate a reasonable portion.

This requires a logical and consistent method. For instance, you could allocate rent based on the percentage of square footage the shop occupies. For a shared employee, you could track their hours and allocate their salary based on the time they spend on the unrelated business. This is why detailed timesheets and clear internal records are so critical—they are the proof that justifies your allocations.

Filing and Reporting Requirements

After you've done the math and calculated your UBTI, you have to report it to the IRS. This isn’t handled on your standard annual information return (like Form 990). It requires a separate, dedicated tax form.

The Key Form: IRS Form 990-T

Any organization that brings in $1,000 or more in gross unrelated business income for the year must file Form 990-T, Exempt Organization Business Income Tax Return. Notice the emphasis on "gross" income. This means that even if your activity ultimately lost money after expenses, you still have to file if your top-line revenue hit that $1,000 mark. The due date for Form 990-T is typically the same as your main Form 990.

Filing a 990-T is more common than you might think. Back in 1995, nearly 10,000 charities were already filing returns for unrelated business activities, and that landscape has only grown more complex. Understanding the historical context can offer valuable insights into how UBIT has been applied over the years.

Understanding Tax Rates and Payments

Once you've reported your net UBTI on Form 990-T, that income is taxed. The rate you pay depends on how your organization is structured. For most nonprofits set up as corporations, UBTI is taxed at the flat corporate income tax rate, which currently stands at 21%. If your organization is a trust, you'll be subject to the trust tax rates, which are often higher and kick in at lower income levels.

Don't forget about paying throughout the year. If you expect your organization to owe $500 or more in tax for the year, you’re required to make quarterly estimated tax payments. These are generally due on the 15th day of the 4th, 6th, 9th, and 12th months of your fiscal year. Missing these deadlines can lead to underpayment penalties, which is just an unnecessary extra cost.

Properly calculating, reporting, and paying tax on UBTI is a fundamental part of maintaining your tax-exempt status. It takes diligence, but a methodical approach ensures you meet all your obligations while only paying what you rightfully owe.

Advanced Strategies for Managing UBTI

Once you’ve got a handle on the basics of unrelated business taxable income, the real work begins. True strategic management means digging into the more complex scenarios that pop up as your organization's activities and investments grow. The standard three-part test won't always give you a clear answer, especially when dealing with nuanced situations like partnership income or multi-state operations.

Getting ahead of these issues is the only way to protect your organization's assets and secure its long-term financial health. When you master the tricky areas—from income passed through partnerships to the specific rules on debt-financed real estate—UBTI shifts from being a potential threat to just another manageable part of your financial strategy.

Navigating UBTI from Partnerships and Investments

Many nonprofits invest in partnerships as a way to generate returns and diversify their portfolios. But this common strategy can open a direct pipeline for UBTI. If a partnership you’ve invested in runs a trade or business unrelated to your mission, your share of that income flows directly to you as UBTI.

That means your organization is on the hook for the tax, even though you weren’t the one directly operating the business. It’s a classic flow-through concept that can easily catch nonprofits off guard. This is why thorough due diligence on any potential partnership investment is absolutely non-negotiable.

Understanding Unrelated Debt-Financed Income

One of the trickiest corners of the UBTI world involves income from property financed with debt. This is formally known as Unrelated Debt-Financed Income (UDFI). Under normal circumstances, passive income streams like rent are exempt from UBTI. But that all changes if you used debt—like a mortgage—to buy or improve the property.

The IRS sees this as using your tax-exempt status to get a leg up in the commercial real estate market. The taxable portion of the income is then calculated based on the property’s debt-to-basis percentage.

Here’s a quick example:

- Property Cost: $1,000,000

- Average Mortgage Balance (during the year): $600,000

- Debt-Financed Percentage: 60% ($600,000 / $1,000,000)

In this case, 60% of the net rental income would be subject to UBTI. If you sell the property, 60% of the capital gain would be taxable, too. This rule demands careful, year-over-year tracking of your debt levels and property basis.

Don't underestimate the scale here. Back in 2017, over 80,000 organizations filed a Form 990-T, reporting a combined $15.4 billion in gross unrelated business income and paying $871.4 million in taxes. While deductions lowered the bill for many, these numbers show just how significant this tax can be. For a closer look, you can explore more data on the taxation of unrelated business income to see the broader impact.

Using a Blocker Corporation for UBTI Management

For organizations with substantial or potentially risky unrelated business activities, one of the most powerful tools in the playbook is a taxable C corporation subsidiary, often called a "blocker corporation." The idea is simple: the nonprofit creates and owns a separate, for-profit company that houses and operates the unrelated business.

This structure acts as a clean and effective shield.

By isolating the unrelated business activity within a separate legal entity, the nonprofit protects its tax-exempt status from being jeopardized by a large or dominant commercial venture. The blocker corporation pays corporate income tax on its profits, and any dividends it passes up to the parent nonprofit are generally received tax-free.

This approach brings several key advantages to the table:

- Risk Containment: It firewalls the financial and legal liabilities of the business, keeping them separate from the nonprofit parent.

- Tax Simplification: The nonprofit can avoid filing a complicated Form 990-T, since all the taxable activity is handled within the C corp.

- Clarity of Purpose: It creates a clean distinction between your mission-driven work and your for-profit ventures, a separation the IRS tends to look upon favorably.

While setting up a blocker corporation comes with legal and administrative costs, it’s an essential strategy for organizations looking to scale their revenue-generating activities responsibly. It provides a formal structure to manage growth, mitigate risk, and ensure that commercial success never puts the core mission in jeopardy. That's what proactive, financially sound leadership looks like.

When to Bring in a Tax Advisor for UBTI

This guide gives you a great starting point, but the world of unrelated business taxable income gets complicated, fast. Knowing when to stop DIY-ing and call in a professional is key to protecting both your organization’s bottom line and its precious tax-exempt status.

Honestly, trying to navigate the gray areas on your own can lead to some painful mistakes—think missed deductions, a surprise tax bill, or even an IRS audit.

Red Flags That Scream "Get an Expert"

A good tax advisor does more than just fill out forms; they provide strategic advice that can save you headaches and money down the road. If you find yourself in any of these situations, it’s probably time to make that call.

Think of it as a financial health check-up. You should definitely engage a professional if you're:

- Launching a new revenue-generating program: Before a single dollar comes in, an advisor can help you structure the new venture to minimize, or even avoid, potential UBTI. This proactive step is always cheaper than cleaning up a mess later.

- Investing in a partnership or LLC: These "pass-through" entities can be a minefield. You need someone who can dig into the details and tell you exactly what kind of UBTI might flow up to your organization from the investment.

- Acquiring property with debt: The rules for Unrelated Debt-Financed Income (UDFI) are notoriously tricky and loaded with exceptions. This isn't something you want to handle with a spreadsheet and a prayer; it requires precise calculations.

- Expanding operations across state lines: As soon as you cross a state border, you open up a whole new can of worms with different state tax laws and filing requirements.

Even a single consultation can give you the clarity you need to move forward with confidence. It’s an investment in peace of mind.

UBTI FAQs: Answering Your Pressing Questions

When you’re running a nonprofit, the rules around unrelated business income can feel like a minefield. Let's walk through some of the most common questions we hear from leaders just like you.

Does a One-Time Fundraiser Generate Taxable Income?

Probably not. For an activity to trigger UBTI, the IRS says it must be “regularly carried on.” Think of it this way: if you’re running a business, you’re open consistently. An annual gala, a one-off charity auction, or a seasonal bake sale just doesn’t fit that description.

The IRS often looks at whether the activity is conducted with the same frequency and continuity as a comparable for-profit business. A yearly event simply doesn't meet that bar.

Could We Actually Lose Our Tax-Exempt Status Over This?

It’s a valid concern, but it’s not common for small amounts of UBTI. The real danger arises when the unrelated business becomes a substantial part of your organization's total activities.

Your primary purpose must always be your exempt mission. If your commercial venture grows so large that it starts to look like your main focus, the IRS might begin to question whether you’re still operating as a true nonprofit. That’s when your tax-exempt status could be put at risk, making careful management essential.

We Rent Out Extra Office Space. Is That a Problem?

This is a classic "it depends" scenario. Generally, passive rental income from real estate is exempt from UBTI. But there are a couple of major tripwires to watch out for.

- Debt-Financed Property: If you still have a mortgage on the building, a portion of that rent is likely taxable. The taxable amount is directly tied to the ratio of your outstanding debt to the property's value.

- Providing Extra Services: The exemption is for rent, not for services. If you start offering tenants things beyond basic utilities and maintenance—like regular cleaning, clerical support, or catering—the IRS may see it as service income, which is taxable.

The key is whether the income is truly passive. The moment you introduce debt or substantial services, it starts to look a lot more like an active business in the eyes of the IRS.

What’s the Line Between Sponsorship and Advertising?

This distinction is absolutely critical. A "qualified sponsorship payment" is not considered UBTI. This is when a business gives you money and, in return, you provide a simple acknowledgment—like putting their name or logo on a banner or in a program.

It crosses the line into taxable advertising the second you start promoting their products or services. Using comparative or qualitative language ("the #1 realtor in the city"), listing prices, or including a call to action ("visit their showroom today!") turns a tax-free sponsorship into taxable advertising revenue. You have to structure these agreements very carefully.

Getting a handle on UBTI is about more than just following the rules; it requires smart, forward-thinking strategy. For organizations in real estate, finance, and the nonprofit world, having an expert partner in your corner can change everything. Blue Sage Tax & Accounting Inc. delivers the specialized guidance you need to stay compliant and protect your mission. See how our advisory services can bring clarity and confidence to your financial management by visiting us at https://bluesage.tax.