Let's get right to it. Tax loss harvesting is a pretty straightforward, yet powerful, strategy. At its core, it's about selling an investment that's in the red to help offset the taxes you'd otherwise owe on your winners. Think of it as finding a tax-related silver lining when one of your assets takes a hit.

How to Turn Portfolio Losses Into a Tax Win

I like to think of a portfolio as a team of players. Some are having a great season (your winners), while others are underperforming (your losers). Tax loss harvesting is like being a smart general manager—you strategically trade the struggling player.

By selling that losing investment, you "realize" the loss. It’s no longer just a number on your screen; it becomes a real financial event that you can put to work on your tax return. The main idea is to use this loss to cancel out the taxable gains you've locked in from your star players.

Tax Loss Harvesting At a Glance

To make this even clearer, let's break down the essential components. The table below gives you a quick snapshot of the concept.

| Concept | Description |

|---|---|

| The Strategy | Selling an investment at a loss to reduce your capital gains tax liability. |

| The Goal | Lower your overall tax bill, which improves your after-tax investment returns. |

| Who It's For | Primarily investors with taxable brokerage accounts (not retirement accounts like 401(k)s or IRAs). |

Basically, you’re taking a loss that already happened and making it work for you. It's a proactive move to manage your tax burden.

The Core Ideas, Simplified

To really get how tax loss harvesting works, you just need to be clear on two concepts:

- Capital Gain: This is just the profit you make from selling something—a stock, a fund, real estate—for more than you paid for it. If you buy a stock for $1,000 and sell it for $1,500, that $500 profit is your capital gain, and the IRS wants a piece of it.

- Realized Loss: This is the flip side. You lock in a loss when you sell an asset for less than you bought it for. Say you bought another stock for $2,000 and had to sell it for $1,200. That gives you an $800 realized loss.

Tax loss harvesting simply connects these two events. You use that $800 loss to completely wipe out the taxes you would have owed on your $500 gain. It's a direct and immediate way to lower your tax bill.

The whole point is to use losses in one area of your portfolio to cut the tax drag from gains in another. It's a savvy move that can boost your real-world, after-tax returns without messing with your long-term investment plan.

The Basic Steps in Practice

So, what does this look like day-to-day? It's a simple, repeatable process.

First, you scan your taxable investment accounts for any positions currently trading below what you paid for them. Then, you pull the trigger and sell that asset to officially "harvest" the loss for tax season.

Next, you use that documented loss to offset any capital gains you've racked up in the same year. And here’s a nice bonus: if your losses are bigger than your gains, you can use up to $3,000 of the excess to lower your regular income, like your salary.

If there's still a loss left over after all that? No problem. You can carry it forward to use in future tax years. It’s a fantastic way to turn a market dip into a tangible financial benefit.

How the Tax Loss Harvesting Process Works

Theory is one thing, but seeing how tax loss harvesting actually plays out is what makes the concept really click. Let's walk through a simple, step-by-step example to see how this strategy unfolds and leads to real tax savings.

We’ll follow an investor, Sarah, who’s looking to get ahead of her tax bill.

Step 1: Identify an Investment with a Loss

Sarah takes a look at her portfolio and spots a technology ETF she originally bought for $20,000. After a market downturn, it's now only worth $15,000. That’s a $5,000 "unrealized" loss sitting on paper.

Meanwhile, earlier in the year, she sold a different stock that did quite well. She bought it for $10,000 and sold it for $15,000, locking in a $5,000 capital gain. If she does nothing, she'll owe capital gains tax on that entire profit.

Step 2: Sell the Asset to Realize the Loss

To make that paper loss work for her, Sarah has to sell the underperforming tech ETF. The moment she sells it for $15,000, her $5,000 loss becomes “realized.” It’s now an official tax event she can report to the IRS.

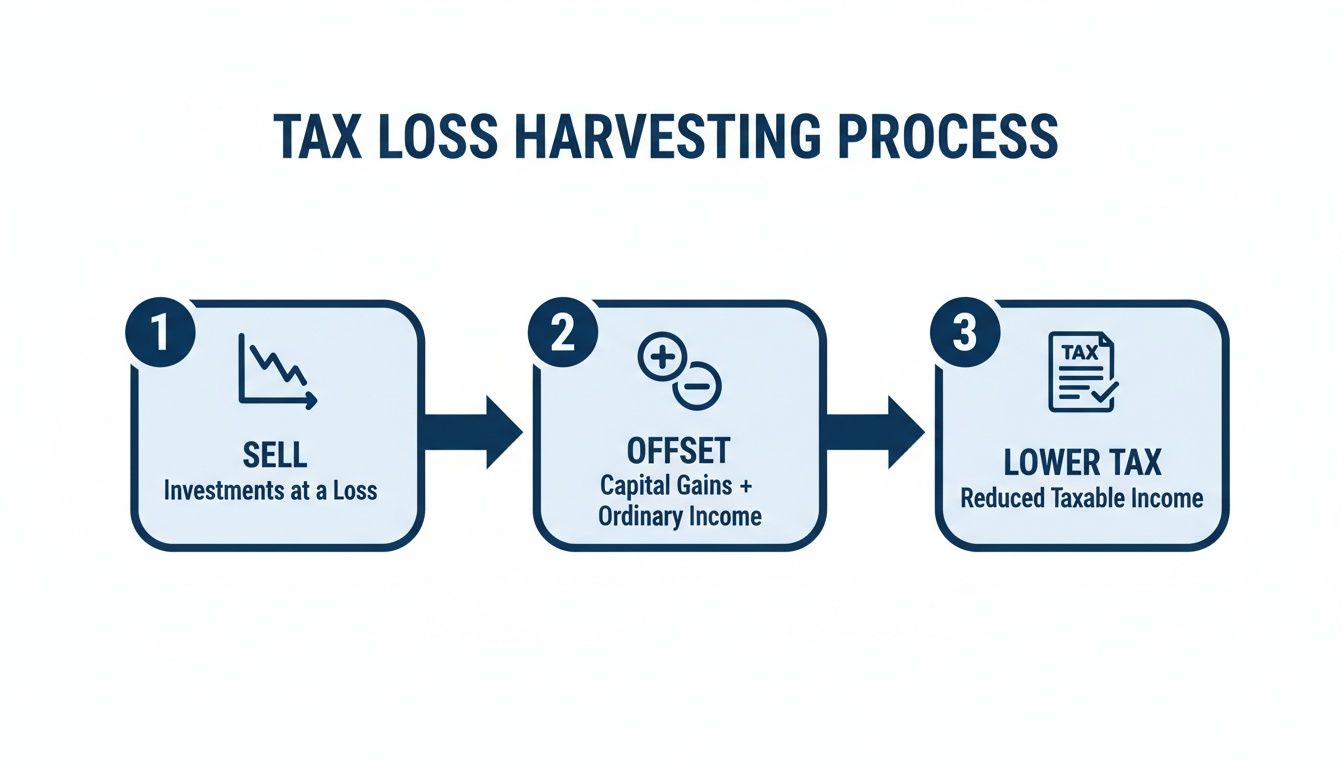

This step is key. An unrealized loss is just a number on your screen; a realized loss is a tool you can actively use to lower your taxes. The whole idea is a straightforward flow: sell, offset gains, and reduce your tax burden.

This graphic really simplifies the core actions involved.

As you can see, you’re moving from selling an asset to directly canceling out gains, which means you end up with a smaller tax bill.

Step 3: Offset Gains and Reduce Taxes

Now for the good part. Sarah applies her $5,000 realized loss directly against her $5,000 realized gain.

- Capital Gain: +$5,000

- Realized Loss: -$5,000

- Net Capital Gain: $0

Just like that, she’s completely wiped out her taxable gain for the year. If her capital gains tax rate was 20%, this one move just saved her $1,000. The power of this strategy really shines in volatile markets. To give you a sense of scale, one firm harvested over $5.5 billion in losses for its clients during a turbulent period, creating a potential tax benefit of more than $2 billion. You can read more about how market volatility creates harvesting opportunities on Parametric's blog.

Step 4: Reinvest and Avoid the Wash-Sale Rule

Sarah doesn’t want the $15,000 from the sale just sitting in cash. She wants to stay invested in the tech sector to catch any potential rebound. But first, she has to navigate a critical IRS regulation: the wash-sale rule.

The Wash-Sale Rule Explained: The IRS won't let you claim a tax loss if you buy the same or a "substantially identical" security within 30 days before or after selling it. This 61-day window (30 days before, the day of the sale, and 30 days after) is there to stop people from selling a stock just for the tax break and then immediately buying it back.

To stay invested without breaking this rule, Sarah makes a smart move.

- She avoids buying back the exact same tech ETF.

- Instead, she reinvests her $15,000 into a different technology ETF that tracks a similar—but not identical—index.

This lets her maintain her exposure to the tech market and benefit from any recovery, all while keeping her tax loss valid. She successfully turned a portfolio loss into a real financial win, keeping her investment strategy on track the whole time.

Understanding the Ground Rules of Tax Loss Harvesting

To get the most out of tax loss harvesting, you have to play by the IRS's rules. Think of them less as roadblocks and more as the rulebook for a game you want to win. Knowing these rules inside and out is what separates a smart idea from a powerful, money-saving strategy.

First up is the big one: the wash-sale rule. This rule exists purely to stop people from selling a stock to claim a tax loss and then immediately buying it right back.

The IRS says you can't claim a loss if you buy the same or a "substantially identical" security within 30 days before or after you sell it. This effectively creates a 61-day window around the sale. If you sell a losing ETF on June 15th, for example, you have to wait until at least July 16th to repurchase it if you want that tax loss to count.

Short-Term vs. Long-Term: Why It Matters

Next, you need to get a handle on the difference between short-term and long-term gains and losses. It’s a simple distinction with big tax implications.

- Short-Term: This applies to any investment you've held for one year or less. Gains here are taxed at your regular income tax rate, which is often much higher.

- Long-Term: This is for assets you've owned for more than one year. The tax rates on these gains are much friendlier—0%, 15%, or 20%, depending on your income bracket.

The IRS is very particular about how you net these out. You can't just mix and match however you'd like.

The IRS has a strict order of operations: you must first use losses to cancel out gains of the same type. Short-term losses have to go against short-term gains first, and long-term losses have to go against long-term gains. You can't skip this step, but it also gives you a clear roadmap for planning.

The IRS Offsetting Order

Once you've matched up losses and gains of the same type, you can use any leftover losses to offset the other category. It works like this:

- Short-term losses get applied to short-term gains.

- Long-term losses get applied to long-term gains.

- If you still have losses remaining, you can cross them over. For instance, any leftover short-term losses can then be used to wipe out long-term gains.

This sequence is crucial because your biggest tax bang-for-your-buck comes from knocking out those high-tax short-term gains.

The $3,000 Ordinary Income Deduction

So, what if you have more losses than gains at the end of the year? Here's where another nice perk kicks in. You can use up to $3,000 of your net capital loss to lower your ordinary income, like the salary from your job.

This is a fantastic benefit because it directly reduces your overall taxable income, saving you even more money. For married couples filing separately, the limit is $1,500 each.

Carried Forward Losses: A Gift That Keeps on Giving

And if your net capital loss is more than the $3,000 you can deduct against your income? Don’t worry, that extra loss isn’t gone forever.

The IRS lets you carry forward any excess losses to future tax years, and they never expire. A big loss you harvest this year can become a valuable asset, ready to offset gains or income for years, even decades, down the road. For example, if you have a $10,000 net loss, you can deduct $3,000 this year and carry the remaining $7,000 forward to slash your tax bill in the future.

When Is the Best Time to Harvest Losses?

Most people think of tax loss harvesting as a year-end scramble, something you rush to do between Thanksgiving and New Year's. This is probably the single biggest mistake investors make. The best time to harvest isn't December 31st; it's whenever the market gives you the opportunity.

Treating this strategy as a holiday chore is a trap. Market volatility doesn't follow a calendar. A great harvesting opportunity in March or July might completely vanish by the time you're thinking about your tax return. A stock that’s down 15% in the summer could easily rebound by winter, erasing that potential tax benefit before you even look.

A Year-Round Proactive Approach

The smart move is to treat tax loss harvesting as a year-round discipline. Instead of reacting to a deadline, you should be ready to act whenever a good opportunity pops up. It’s a simple but powerful shift from being reactive to being proactive.

Being proactive just means you’re keeping an eye out for harvesting candidates all the time, not just when the taxman is knocking. This lets you lock in losses when they're actually there, rather than hoping they stick around for months.

This vigilance pays off even when the market is soaring. For example, a recent analysis found that while the market was up overall, about 40% of the 1,000 largest U.S. stocks had actually dropped in value over the past year. As experts at State Street have noted, it's critical to harvest when losses appear because stocks that are down early in the year often bounce back, taking the tax-saving opportunity with them. You can discover more about finding harvesting opportunities no matter what the market is doing.

Triggers for Harvesting Losses

So, if not the calendar, what should tell you it's time to act? The real triggers are market movements, big and small. Staying alert to these events is the key.

- Broad Market Downturns: When the whole market takes a hit, even your strongest long-term investments can go into the red. These are golden opportunities to harvest substantial losses across your portfolio.

- Sector-Specific Volatility: Sometimes, it’s not the whole market but just one industry—like tech or energy—that hits a rough patch. This allows for very targeted harvesting in that one corner of your portfolio.

- Individual Stock Declines: A bad earnings report or some company-specific news can send a single stock tumbling. Acting on these isolated drops is just as important as capitalizing on wider market trends.

Waiting until December is like trying to catch fish in a pond that has been shrinking all year. The best opportunities are often found when the water is high—during periods of volatility—not when it's most convenient for your tax filing schedule.

Establishing a Review Cadence

Look, checking your portfolio every day isn't practical for most people. What you need is a sustainable routine.

A quarterly portfolio review is a fantastic starting point for almost everyone. It’s frequent enough to catch major market swings without feeling like a full-time job. That said, if the market gets particularly choppy, you might want to bump that up to a monthly check-in. The goal is to build a system that keeps you in the loop and ready to turn a paper loss into a real tax advantage.

Advanced Strategies and Portfolio Integration

While the basic idea of tax loss harvesting is pretty straightforward, its real power comes alive when you weave it into a larger wealth plan using more sophisticated tools. For anyone with a complex financial life, this isn't just a year-end cleanup task. It becomes a year-round engine for boosting your after-tax returns.

The key is to move beyond manually checking a handful of ETFs or mutual funds. The more individual stocks you own, the more chances you have to find and harvest losses. This is where owning the market directly, rather than through a fund, becomes a total game-changer.

Unlocking Precision with Direct Indexing

Think about this: instead of owning a single S&P 500 ETF, what if you owned tiny pieces of all 500 companies in that index? That’s the core concept behind direct indexing. You own the individual stocks directly in what's called a separately managed account (SMA), not a pre-packaged fund.

This one shift creates a massive advantage for tax loss harvesting. Even when the overall market is climbing, there are almost always a few companies inside the index that are having a bad day, week, or month. Direct indexing lets you pinpoint those specific losers and sell them to harvest a loss, even in a raging bull market.

With a normal ETF, your hands are tied—you can only sell when the entire fund is trading at a loss. But with direct indexing, you can chip away at losses from dozens of individual stocks all year long. You're essentially creating a steady stream of tax assets that you couldn't access otherwise.

This proactive approach is crucial. For instance, think about the quick, sharp market dips we've seen triggered by things like tariff news. As Natixis Investment Managers pointed out, investors using disciplined, tech-driven strategies could harvest those losses in the moment before the market bounced back. They captured a benefit that slower, reactive investors completely missed. You can learn more about their insights on timely tax management.

By owning the underlying stocks, you transform a blunt instrument (an ETF) into a surgical tool. This allows for more frequent, precise, and impactful loss harvesting, systematically improving your portfolio's tax efficiency.

Integrating Tax Loss Harvesting with Your Full Financial Picture

Smart tax loss harvesting doesn't happen in a vacuum. It has to be connected to your entire financial world, especially if you're dealing with taxes in multiple states or countries.

A loss you harvest for federal taxes doesn't just stop there. It creates ripples. You have to think about how it affects your state and local taxes, where the rules and rates can be completely different. For someone living in New York City, for example, the combined state and city tax bite adds another layer to the math, making each harvested loss potentially even more valuable.

Tax Loss Harvesting Methods Comparison

Choosing the right way to harvest losses really comes down to how complex your portfolio is and how much precision you need. The old-school manual approach is simple but doesn't get you very far. Modern automated tools, on the other hand, offer a lot more firepower.

Here's a quick breakdown of how the different methods stack up.

| Feature | Manual DIY | Robo-Advisor | Direct Indexing |

|---|---|---|---|

| Harvesting Frequency | Typically year-end | Automated, often daily or when thresholds are met | Continuous, daily monitoring of individual stocks |

| Precision | Low; based on entire fund positions | Medium; limited to the platform's set of ETFs | High; targets individual securities within an index |

| Opportunity | Limited to when entire funds are down | More frequent, but only within a limited ETF menu | Maximized; finds losses even in up-markets |

| Customization | High, but labor-intensive | Low; uses pre-set portfolios | High; can exclude specific stocks or sectors |

As you can see, the level of sophistication and opportunity grows significantly as you move toward direct indexing.

For international clients, things get even trickier. You're juggling tax treaties, foreign tax credits, and currency swings. A loss harvested in a U.S. brokerage account could have totally different consequences for your tax bill back home. It takes careful, coordinated planning to make sure a tax win in one country doesn't accidentally cause a problem in another. The goal is to make sure every move is optimized across your entire global footprint.

Common Mistakes to Avoid

Executing tax loss harvesting is one thing; executing it well is another. While the concept seems straightforward, a few common tripwires can easily undermine your efforts or, worse, get you in trouble with the IRS. Knowing what to watch out for is the key to turning a good idea into a great tax-saving strategy.

The single biggest and most frequent mistake is accidentally triggering the wash-sale rule. This rule is much broader than many people think. It doesn't just apply to the account where you sold the loser; it looks across all of your accounts.

For example, let’s say you sell a losing S&P 500 ETF in your brokerage account. If you then buy a nearly identical S&P 500 ETF in your IRA within 30 days (before or after the sale), that tax loss is disallowed. The IRS is wise to that move.

Letting the Tax Tail Wag the Investment Dog

Another classic blunder is becoming so focused on tax savings that you lose sight of your actual investment plan. Remember, the primary goal of your portfolio is to grow your wealth. Tax efficiency is the sidekick, not the hero.

It’s easy to fall into this trap. You might hold onto a fundamentally weak investment just to avoid realizing a gain, or you might sell a great one prematurely just to book a small loss. The tax savings from a minor harvest often pale in comparison to the long-term gains you could miss by making a poor investment decision.

Key Takeaway: Your investment strategy must always be in the driver's seat. Tax loss harvesting is a powerful tool to enhance your returns on an already solid plan, not an excuse to abandon it.

Practical Errors That Chip Away at Your Gains

Beyond the major strategic missteps, a handful of smaller, practical errors can quietly eat away at the benefits of your harvesting strategy. It’s the little details that often count.

- Chasing Pennies: Selling a position to capture a tiny loss often isn't worth the hassle. After you factor in trading commissions or bid-ask spreads, the meager tax savings can completely disappear.

- Sitting on the Sidelines: After selling a security for a loss, some investors get nervous and leave the money in cash. This is market timing, and it’s a dangerous game. If the market bounces back while you’re waiting, you’ll miss the recovery, and those lost gains can easily wipe out any tax benefit you just created.

- Getting Emotional: Let's be honest—selling for a loss feels bad. It’s tough psychologically. This can lead investors to procrastinate or react emotionally to market dips. The best defense is a pre-set plan, like deciding to harvest any position that falls by a specific percentage. This removes emotion and ensures you act with discipline.

By steering clear of these common mistakes, you can execute your tax loss harvesting strategy with confidence, effectively turning market downturns into a valuable financial opportunity.

Your Questions, Answered

Even when you've got the basics down, tax loss harvesting can bring up some tricky questions. Let's walk through a few of the most common ones that clients ask to clear up the details.

Can I Use Tax Loss Harvesting in My 401(k) or IRA?

That’s a great question, but the short answer is no. Tax loss harvesting only works for your taxable investment accounts, like a standard brokerage account.

Think of it this way: retirement accounts like 401(k)s and IRAs already come with their own powerful tax benefits. Their growth is either tax-deferred or tax-free, so you're not paying capital gains taxes on your investment wins inside the account anyway. Since there are no capital gains to offset in the first place, harvested losses have no job to do.

How Do I Report Harvested Losses on My Tax Return?

Reporting these losses is a normal part of filing your taxes each year. You’ll just need to lay out the details of your trades on a couple of specific IRS forms.

It boils down to two main forms:

- IRS Form 8949 (Sales and Other Dispositions of Capital Assets): This is where you get into the nitty-gritty, listing each sale with its purchase date, sale date, cost basis, and sale price.

- Schedule D (Capital Gains and Losses): This form acts as the summary. It takes the totals from Form 8949 and nets everything out to give you one final number for your net capital gain or loss for the year.

The process is straightforward, but accuracy is everything. Working with a tax pro can give you peace of mind that all the details are handled correctly.

A quick tip: keep meticulous records of your trades as you make them. It makes tax time so much smoother and gives you a clean paper trail if the IRS ever comes knocking with questions.

What’s a Good Replacement Investment to Avoid a Wash Sale?

This is where the art and science of this strategy really come together. To sidestep a wash sale, you need to buy a replacement asset that is similar enough to keep your portfolio on track, but not "substantially identical" to the one you just sold.

For instance, say you sell an S&P 500 ETF from Vanguard. You could immediately buy an S&P 500 ETF from iShares. They both track the same index, but because they're issued by different companies, the IRS generally doesn't consider them substantially identical. Another smart move could be swapping an S&P 500 fund for an ETF that tracks a different but closely related index, like the CRSP US Large Cap Index. You stay invested in large-cap stocks but have successfully harvested the loss.

Making tax loss harvesting work within your broader financial plan takes careful planning and a deep understanding of the rules. At Blue Sage Tax & Accounting Inc., we help individuals and businesses translate complex tax strategies into clear, actionable steps that boost their after-tax returns. Schedule a consultation with our team to optimize your tax strategy today.