If you own commercial or residential rental property, you're likely familiar with depreciation—that slow, steady tax deduction you take over decades. But what if you could speed that up and get your tax savings much, much sooner? That's exactly what cost segregation lets you do.

It’s a sophisticated, IRS-approved tax strategy that can dramatically increase your cash flow by accelerating depreciation deductions.

Unlocking Your Property's Hidden Value

Without a cost segregation study, the IRS views your building as one single asset. That means you’re stuck depreciating commercial properties over a long 39-year period and residential properties over 27.5 years. It’s a painfully slow trickle of tax benefits.

A cost segregation study changes the game. Think of it this way: instead of seeing one giant building, a study "unbundles" it into all its individual components. It’s like taking apart a complex machine to see all the gears, wires, and bolts that make it work.

Reclassifying Assets for Faster Depreciation

This detailed analysis identifies and separates all the non-structural elements and land improvements from the core building itself. Suddenly, a single 39-year asset becomes dozens of smaller assets with much shorter depreciable lives.

This is where you find the hidden value. Many of these components can be reclassified into faster depreciation categories:

- 5-Year Property: Things like carpeting, dedicated electrical outlets, specialty plumbing, and decorative lighting.

- 7-Year Property: This often includes office furniture, cabinetry, and other fixtures.

- 15-Year Property: This covers exterior assets like parking lots, sidewalks, fencing, and landscaping.

By moving assets out of the 39-year bucket and into these 5, 7, and 15-year buckets, you can claim a much larger chunk of your depreciation expense right away.

To better illustrate the difference, here's a simple breakdown of the two approaches.

Cost Segregation at a Glance

This table compares traditional depreciation with the accelerated method used in cost segregation, highlighting the immediate financial advantages for property owners.

| Concept | Traditional Depreciation | Accelerated Depreciation with Cost Segregation |

|---|---|---|

| Asset Treatment | Entire building treated as a single asset. | Building is "unbundled" into multiple components. |

| Depreciation Timeline | 27.5 years (residential) or 39 years (commercial). | Components are moved to 5, 7, and 15-year schedules. |

| Tax Deductions | Small, even deductions spread over decades. | Large, front-loaded deductions in the early years. |

| Cash Flow Impact | Minimal near-term impact. | Significant increase in immediate, after-tax cash flow. |

As you can see, the shift in timing is what makes this strategy so powerful for real estate investors.

The Impact on Your Bottom Line

On average, a quality cost segregation study can reallocate 20% to 40% of a property's total cost basis into these shorter-lived asset classes.

This reclassification is the engine that drives your tax savings. By generating massive non-cash deductions in the early years of ownership, you significantly lower your taxable income. The result? A much smaller tax bill and more cash in your pocket.

That extra capital can be put to work immediately—reinvested in the business, used to upgrade the property, or saved for your next acquisition. It’s all about the time value of money. Cost segregation puts your own money back in your hands today, instead of making you wait 39 years to see the full benefit.

How Cost Segregation Actually Works

To really get what cost segregation is all about, you have to stop thinking of your property as just one big building. It’s actually a collection of hundreds of different parts, and each of those parts has its own lifespan. Standard tax depreciation completely ignores this reality.

The IRS usually lumps a commercial building into a single asset and makes you write it off over a painfully slow 39 years. For residential rentals, it’s a little better at 27.5 years, but you're still waiting decades to get your tax benefits. Cost segregation is the key to breaking up that outdated, slow-moving model.

It all comes down to a detailed, engineering-based study that meticulously identifies and reclassifies parts of your property into shorter depreciation schedules. This isn't some accounting loophole; it's a recognized, precise way to align your tax deductions with the real economic life of your assets.

Breaking Down the Building, Piece by Piece

At its heart, a cost segregation study is about sorting. The goal is to move as much of your property's cost as possible out of that long-term "building" category and into shorter-term ones.

This deep dive separates the property's components into four main buckets:

- Personal Property (5-Year & 7-Year Life): These are the things not essential to the building's basic function. Think about decorative lighting, special wiring for equipment, custom millwork, carpeting, and even certain plumbing hookups. These items wear out much faster than the foundation.

- Land Improvements (15-Year Life): This is everything outside the building's footprint. We're talking about parking lots, sidewalks, retaining walls, fencing, storm drainage, and landscaping.

- Building Structure (27.5-Year or 39-Year Life): This is what's left over. It’s the true "bones" of the building—the foundation, structural frame, roof, walls, and windows.

By carefully sorting every last component, a study frees up massive depreciation deductions that were otherwise locked away for decades.

The real power here is in timing. Moving an asset from a 39-year schedule to a 5-year schedule means you get to claim that tax deduction more than 7 times faster. The result is an immediate and powerful boost to your cash flow.

How Reclassifying Drives Real Savings

Let's talk numbers, because that’s where this gets exciting. The main benefit comes from just how much of a property's cost can be moved. We're not talking about small adjustments; it's a major shift in how the asset is viewed for tax purposes, and that shift creates big savings.

Typically, a study can reclassify 20% to 40% of a property’s total cost into those faster 5, 7, or 15-year categories. For a $1 million commercial property, that means $200,000 to $400,000 could be moved, generating accelerated deductions that can save owners tens of thousands of dollars in the very first year. You can learn more about how these studies work from foundational tax resources.

This gets even better when you factor in bonus depreciation. In some years, the IRS allows you to write off 100% of the cost of eligible property (anything with a life of 20 years or less) in the year it's placed in service. A cost segregation study is what officially identifies all those eligible assets.

Without a study, you might only spot a few obvious items. But with a proper engineering analysis, you can legally reclassify hundreds of thousands of dollars in assets, making them all eligible for that huge first-year write-off. It turns a slow trickle of tax savings into a tidal wave of upfront cash.

The Cost Segregation Study Process

Knowing the financial perks of cost segregation is one thing, but understanding how a study actually works is another. This isn’t just some accounting maneuver; it's a sophisticated, engineering-driven analysis that meticulously dissects a property into all its individual pieces. The goal is to produce a rock-solid report that maximizes your tax savings and can stand up to any IRS questions.

So, what does this look like from your perspective as a property owner? It all starts with a no-risk assessment and follows a clear, step-by-step path.

Phase 1: The Feasibility Check

First things first, we need to see if a study even makes sense for your property. A qualified firm will take a quick look at your building's basic details—its cost basis, when it was placed in service, and any renovation history—to give you a solid estimate of the potential tax savings.

This initial review is almost always done at no cost. It’s designed to give you a clear snapshot of the projected benefits, the fee for the full study, and your likely return on investment before you spend a dime. You get all the numbers upfront, so you can make a smart, informed decision with no pressure.

Phase 2: Kicking the Tires and Gathering the Docs

Once you give the green light, the real work begins. The cost segregation team will collect all the documents they need to get a complete picture of your property. This usually includes things like:

- Architectural Blueprints: The roadmap for the building’s structure and design.

- Construction Invoices: These provide the hard costs for individual components.

- Appraisal Reports: Often contain great details on the property’s condition and unique features.

- Depreciation Schedules: Shows how the property has been depreciated up to this point.

After the paperwork is sorted, a specially trained engineer will conduct an on-site inspection. This is where the engineering-based approach really proves its worth. The engineer will walk every inch of the property, documenting, photographing, and measuring everything from the custom light fixtures in the lobby to the landscaping and asphalt in the parking lot.

Phase 3: Allocating Costs and Delivering the Report

With all the data in hand, the team dives into the heart of the study: allocating costs. Drawing on industry-standard cost estimation guides and their own engineering expertise, they assign a specific value to every single component they identified. Each asset is then carefully sorted into its correct depreciation category—5-year, 7-year, 15-year, or the leftover 39-year structural property.

This is the key step that transforms a single, monolithic building asset into a detailed list of reclassified components ready for accelerated depreciation.

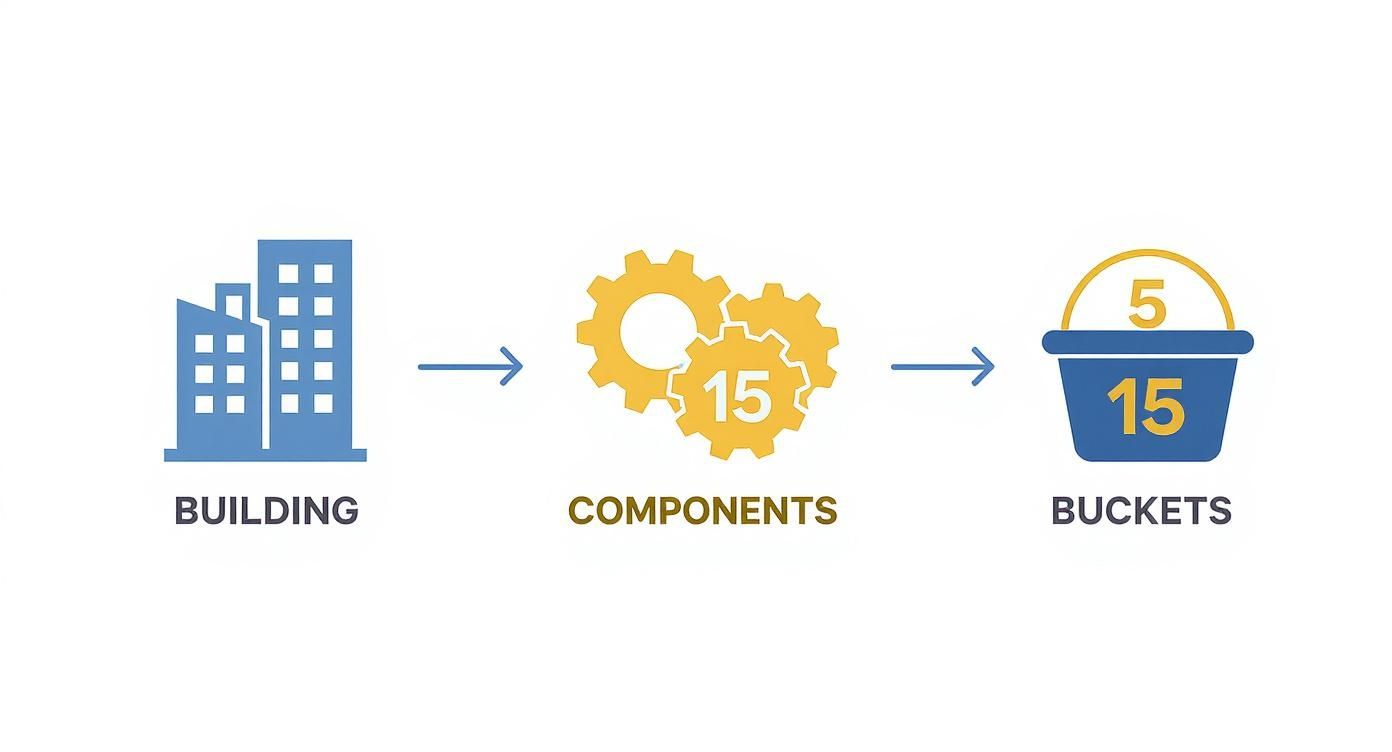

The diagram below gives you a great visual of this process, showing how a building is broken down and its components are sorted into different depreciation "buckets."

As you can see, the study essentially "unbundles" the property's value, pulling assets out of that slow 39-year schedule and moving them into much faster ones.

The final report is far more than a simple summary. It’s a comprehensive, audit-proof document detailing the methodology, a complete breakdown of every reclassified asset, and all the support you’d ever need.

This final report is delivered to your CPA, ready for immediate implementation. It includes all the necessary schedules and documentation to support the new depreciation figures, making it seamless for your accounting team to claim your tax savings without any extra legwork.

Seeing the Financial Impact in Action

Talking about the theory behind cost segregation is one thing, but seeing the numbers come to life is where it really clicks. The true power of this strategy is the immediate cash flow it puts back in your pocket. Nothing shows this better than running through a couple of real-world examples.

Let's dive into two common scenarios. First, we’ll look at a commercial office building and then a multifamily property to show you the kind of tangible, first-year tax savings investors can actually achieve.

The Power of Reclassification: A Commercial Building Example

Imagine you've just acquired a commercial office building for $2 million. If you leave it as is, the IRS makes you depreciate the entire building over a painfully long 39-year period. That gives you a slow, steady, but pretty small annual deduction.

But what happens when you bring in a team to conduct a cost segregation study? The results are night and day.

Let's look at a quick side-by-side comparison to make the impact crystal clear.

Example Tax Savings on a $2M Commercial Property

| Metric | Without Cost Segregation | With Cost Segregation |

|---|---|---|

| Property Cost Basis | $2,000,000 | $2,000,000 |

| Depreciation Method | Straight-line over 39 years | Assets broken into 5, 15, & 39-year lives |

| 1st-Year Depreciation | $51,282 | $110,897 |

| Additional Deduction | – | $59,615 |

| 1st-Year Tax Savings (35% bracket) | $17,949 | $38,814 |

| Net Savings in Year One | – | $20,865 |

As you can see, the study more than doubled the first-year depreciation deduction. That extra $59,615 in deductions translates directly to $20,865 in tax savings—money you can reinvest, use for capital improvements, or simply put back in your bank account. In most cases, the study pays for itself several times over in the very first year.

Supercharging Savings with Bonus Depreciation: A Multifamily Example

Now, let's take it up a notch by throwing bonus depreciation into the mix. This is where cost segregation becomes an absolute game-changer.

Let's say you bought a multifamily apartment building for $3 million (not including the land). A cost segregation study finds that 25% of the building's cost, or $750,000, can be reclassified into 5-year and 15-year property components.

Under current tax law, these shorter-lived assets are eligible for bonus depreciation, which lets you write off a huge chunk of their cost immediately. Assuming an 80% bonus depreciation rate is available, the math looks incredible:

- Bonus Depreciation Deduction: $750,000 in reclassified assets x 80% = $600,000

- Standard Depreciation: You still get to depreciate the remaining structural and component costs.

- Total First-Year Deduction: You're looking at a total deduction north of $700,000.

Without the study, your first-year deduction would have been a mere $109,091 ($3M / 27.5 years). By combining cost segregation with bonus depreciation, you've just created nearly $600,000 in extra deductions in year one.

One analysis from 2018 showed that a $2 million property could easily uncover $600,000 in assets eligible for accelerated depreciation, resulting in $40,000 to $60,000 in first-year tax savings. You can learn more about how these benefits apply to multifamily properties.

These examples prove that cost segregation isn't just a minor accounting tweak—it's a core financial strategy for maximizing your return on investment right from the start.

Is My Property a Good Fit? Navigating Eligibility and IRS Rules

Once you see the financial power of cost segregation, two big questions immediately pop up: "Is my property a good candidate for this?" and "What does the IRS think about it?"

It’s true, not every property is a perfect fit. And trying to cut corners on the process can turn a brilliant tax-saving move into a massive headache. The best way to protect yourself and ensure your tax savings are secure is to insist on a high-quality, engineering-based study. It’s your best defense, building your claims on a rock-solid foundation that can easily stand up to scrutiny.

The goal is simple: make sure the tax savings you unlock are significantly more than the cost of the study itself. That’s how you get a clear and immediate return on your investment.

Zeroing In on Ideal Property Candidates

While just about any income-producing property can get some benefit, some are simply home runs for cost segregation. As a general rule of thumb, the best candidates are properties that were bought, built, or significantly renovated for $750,000 or more, not including the land value.

Certain types of buildings consistently deliver the biggest wins because they are packed with non-structural and specialized components. Think of places like:

- Commercial Real Estate: Office buildings and retail centers are full of 5-year assets, from the carpeting and decorative lighting to all the specialty electrical wiring.

- Hospitality: Hotels and resorts are a goldmine of 5- and 7-year assets. We're talking furniture, fixtures, kitchen equipment, and all the decorative touches that create the guest experience.

- Healthcare Facilities: Medical offices and hospitals are loaded with specialized plumbing, high-tech electrical systems for equipment, and custom exam room cabinetry—all prime for reclassification.

- Industrial Properties: Manufacturing plants and warehouses have process-related infrastructure, heavy-duty electrical systems, and special equipment foundations that can be written off much faster than the building itself.

The Hidden Gem: A "Look-Back" Study

One of the biggest myths is that cost segregation is only for buildings you just bought. Thankfully, that's not true. The IRS allows you to perform a "look-back" study, which lets you go back and capture all the depreciation you missed in prior years.

This is one of the most powerful features in the tax code. You can have a study done on a property you’ve owned for years and then claim all the “catch-up” depreciation in a single tax year. You do this by filing an IRS Form 3115, "Application for Change in Accounting Method"—no need to go back and amend old tax returns.

This means the window of opportunity hasn't closed. A look-back study can create a huge, one-time deduction that slashes your current tax bill and injects a serious amount of cash back into your business. It's like finding a treasure chest of tax savings you never knew you had.

Staying on the Right Side of the IRS

Let's be clear: the IRS absolutely recognizes cost segregation as a legitimate tax strategy. But they have very specific expectations about how the study is done. You can't just guess at the value of your assets or use a generic checklist; that’s a surefire way to attract an audit.

The IRS even published a guide, the Cost Segregation Audit Techniques Guide, which lays out their preferred method. It’s what we call an "engineering-based" approach. This requires a detailed physical inspection of the property, a thorough review of blueprints and construction documents, and a methodical cost allocation process done by qualified professionals. A flimsy report that skips these steps is a major red flag for an auditor.

What Happens When You Sell? Understanding Depreciation Recapture

It’s critical to see the full picture, and that includes what happens down the road when you sell the property. When that day comes, the IRS requires you to "recapture" the depreciation you've taken over the years.

In simple terms, a portion of the profit from your sale will be taxed at your higher ordinary income tax rate (up to 37%) instead of the lower capital gains rate (usually 15% or 20%). The amount that gets recaptured is based on the accelerated depreciation you claimed on all those shorter-lived personal property assets (the 5- and 7-year items).

This might sound like a downside, but it rarely cancels out the benefit. The time value of money is a powerful force. The enormous upfront tax savings and improved cash flow you get from cost segregation almost always outweigh the future tax hit from recapture. Having that cash in your hands today—to reinvest, pay down debt, or expand your portfolio—is far more valuable than a slightly smaller tax bill many years from now.

Taking the Next Step for Your Portfolio

So, there you have it. You’ve seen how cost segregation in real estate works—it’s not some loophole, but a proven, IRS-accepted strategy to speed up depreciation. The goal is simple: lower your tax bill now, not 39 years from now, and seriously improve your cash flow in the process.

This isn't just a paper exercise. By correctly reclassifying parts of your property, you pull forward tax benefits that would otherwise be locked away for decades. Think of it as gaining immediate access to your own capital. That cash can then be put to work—funding a new renovation, paying down a high-interest loan, or even helping you acquire that next property on your list.

How to Get Started

Getting the ball rolling is actually pretty straightforward and doesn't require a huge commitment upfront. It all starts with a simple conversation.

-

Connect with a Specialist: The first move is to talk to someone who lives and breathes this stuff. That could be your CPA or a specialized firm like Blue Sage that focuses on real estate tax planning.

-

Request a Preliminary Analysis: This is a quick, no-obligation look at your property. You'll just need to provide some basic details like the building's cost, when you bought it, and what type of property it is.

-

Review Your Potential Savings: From that info, a specialist can put together a solid estimate of your potential tax savings and what the return on your investment would be for a full study.

Think of this initial assessment as your roadmap. It takes the abstract concept of cost segregation and puts real numbers to it, showing you the potential dollar-for-dollar impact on your finances before you decide to move forward.

Don't let this opportunity pass by. Getting a preliminary analysis is the single best way to see if this powerful strategy is a good fit for your portfolio. Reach out to a trusted advisor today and start putting your capital back in your pocket.

Common Questions We Hear About Cost Segregation

Even after seeing the potential savings, it's natural to have questions about how this all works in the real world. Let's tackle some of the most common ones we get from property owners just like you.

Can I Do a Study on a Property I Bought Years Ago?

Absolutely. This is one of the best features of cost segregation. The IRS allows you to perform a "look-back" study on a property you acquired or built in a previous year.

You get to catch up on all the accelerated depreciation you missed out on, and you can claim it all in the current tax year. It’s done by filing a Form 3115, Application for Change in Accounting Method. The great thing is you don't have to go back and amend old tax returns, which simplifies the process immensely.

What Does a Cost Segregation Study Actually Cost?

There's no single price tag, as the fee really depends on the size and complexity of your property. A study could cost a few thousand dollars for a smaller residential rental, but it can be significantly more for something like a large hotel or a complex manufacturing facility.

Think of it as an investment, not an expense. A well-executed study should pay for itself many times over, often just in the first year. The immediate tax savings and improved cash flow should easily outweigh the upfront cost.

What Kind of Properties Benefit the Most?

Just about any property can benefit, but the sweet spot is typically for buildings that were purchased, constructed, or had major renovations costing over $750,000. The real winners are properties with a lot of "stuff" inside them that isn't part of the core structure.

We see the biggest impact with properties like hotels, medical offices, restaurants, and manufacturing plants. Why? Because they're filled with specialized equipment, wiring, plumbing, and decorative finishes that can be reclassified into shorter-lived assets (5, 7, and 15-year property), generating huge deductions upfront.

The best way to know for sure is to get a preliminary analysis. A specialized firm can give you a solid estimate of your potential savings, usually at no cost, to see if a full study is worthwhile for your specific building.

Ready to see how a cost segregation study could impact your real estate portfolio? The team at Blue Sage Tax & Accounting Inc. can provide the expert analysis you need to unlock hidden value and improve your cash flow. Schedule a consultation to explore your tax-saving opportunities.