An irrevocable trust is a legal arrangement where you permanently hand over assets, giving up control for good. Think of it like putting your most valuable possessions in a high-security vault, giving the only key to a trusted manager, and telling them exactly how to distribute the contents to your family down the line. The critical part? You can't just ask for the key back.

Understanding the Core Concept of an Irrevocable Trust

At its heart, an irrevocable trust isn't just a document; it's a separate legal entity designed to hold your assets. Once you move property—whether it's real estate, a stock portfolio, or cash—into the trust, it's no longer legally yours. This finality is precisely where the trust gets its power, but it's also its biggest trade-off.

This arrangement always has three key players:

- The Grantor: That's you—the person creating the trust and funding it with your assets.

- The Trustee: This is the manager you pick to run the show. They have a strict legal duty (a fiduciary duty) to manage the trust's assets exactly as you’ve instructed, always acting in the best interests of the beneficiaries.

- The Beneficiaries: These are the people or organizations, like your kids, grandkids, or a favorite charity, who will eventually benefit from the trust.

The Fundamental Trade-Off

The bargain is straightforward: you give up control and access to your assets, and in return, you get powerful protections. Because the assets are no longer in your name, they are generally shielded from your personal creditors, lawsuits, and—perhaps most importantly—from being counted as part of your taxable estate.

This makes the irrevocable trust a cornerstone of sophisticated estate planning, especially for high-net-worth individuals in competitive arenas like New York City. For professionals in fields like real estate and finance who face a higher risk of litigation, this kind of asset protection is invaluable. In fact, a 2020 survey found that 63% of estate planning attorneys saw a major uptick in clients using irrevocable trusts amid economic uncertainty. You can dig deeper into these strategies in this detailed analysis of irrevocable trust benefits.

By design, an irrevocable trust creates a clean break between you and your assets. It’s this very separation that provides a robust defense against future financial threats and tax liabilities—a level of protection a simple will or revocable trust just can't match.

Ultimately, choosing an irrevocable trust is a long-term play. You're prioritizing multi-generational wealth preservation and asset protection over having immediate flexibility. It’s a permanent move that locks in your strategy, ensuring your legacy is secure for the generations to come, shielded from the risks of the outside world.

The Real Payoff of an Irrevocable Trust

Why on earth would anyone willingly lock their assets in a vault and hand over the key? That’s the core question everyone asks about an irrevocable trust. The answer isn’t about losing something; it’s about what you gain. The trade-off unlocks three powerful layers of protection that are absolutely essential for serious, long-term wealth preservation.

For many people, the decision to give up control is justified by the immense security they get in return.

Building a Financial Fortress

The biggest draw is creating a fortress around your wealth. When you move assets into an irrevocable trust, they legally aren't yours anymore. This separation is the entire point—it puts those assets far beyond the reach of potential creditors or future lawsuits.

If you're a doctor, a real estate developer, or an entrepreneur, this isn't just a nice perk; it's a fundamental part of a smart financial plan. It means a lawsuit stemming from your business can't wipe out the nest egg you’ve built for your family.

Shrinking Your Estate Tax Bill

Another huge advantage is the tax savings. When you fund a properly designed irrevocable trust, those assets are officially removed from your estate. The result? You can drastically reduce, or even completely wipe out, the estate tax bill your family would otherwise have to pay.

With the federal estate tax rate hovering around 40% for assets above the exemption limit, this is a game-changer. For families with significant wealth, an irrevocable trust can mean millions of dollars passed to the next generation instead of to the IRS.

Think of it this way: an irrevocable trust lets you move appreciating assets out of your name now, essentially "freezing" their value for tax purposes. All the growth that happens from that point on occurs outside of your taxable estate, directly benefiting your heirs.

This is more important now than ever. The current federal estate tax exemption is set to be slashed almost in half in 2026. Getting ahead of that change with an irrevocable trust is one of the most effective moves you can make to protect your family's future.

Planning for Long-Term Care Needs

On a more practical level, an irrevocable trust is a critical tool for long-term care planning. The cost of a nursing home or assisted living can be catastrophic, easily burning through a lifetime of savings in just a few years. To qualify for government aid like Medicaid, your personal assets must be below a very strict threshold.

By placing assets into a specialized irrevocable trust—often called a Medicaid Protection Trust—you can legally bring your "countable" assets down to a level that meets the program's eligibility rules.

But this isn't something you can do at the last minute. There's a big catch:

- The Five-Year Look-Back: Medicaid scrutinizes all asset transfers made within five years of your application. If you moved assets into a trust during that window, you'll face a penalty period where you are ineligible for benefits.

- Plan Ahead: For this strategy to work, the trust must be set up and funded more than five years before you need care. It's a classic case where foresight pays off immensely.

The Big Trade-Off: You Give Up Control

While these benefits are powerful, they come with a non-negotiable price tag: you lose control. Once the trust is created and funded, you can't just change your mind, tweak the terms, or pull the assets back out. The decision is permanent.

This rigidity is exactly what makes the trust so effective for asset protection and tax savings. It’s also why establishing one is a major life decision that absolutely requires expert guidance. You're setting a plan in stone, so it needs to be built to last. Working with a knowledgeable team, like the experts at Blue Sage Tax & Accounting Inc., is crucial to make sure the structure is perfectly aligned with your goals before you turn the key.

Choosing the Right Type of Irrevocable Trust

There’s no such thing as a one-size-fits-all irrevocable trust. Think of it less like a single product and more like a specialized toolkit. Each tool is engineered to solve a very specific financial problem—whether that’s slashing your estate tax bill, building a legacy that lasts for generations, or simply making sure your spouse is taken care of.

The first step is always to pinpoint what you’re trying to accomplish. From there, you can explore the different variations and find the one that aligns perfectly with your family’s needs. Let's walk through some of the most common and powerful types of irrevocable trusts we see used today.

The Irrevocable Life Insurance Trust (ILIT)

One of the most popular tools in the estate planning world is the Irrevocable Life Insurance Trust, or ILIT. Its primary job is simple but brilliant: it keeps your life insurance death benefit from being counted as part of your taxable estate.

Here’s the problem many people don't realize: if you personally own a life insurance policy, the entire payout gets added to your estate's value when you pass away. For a multi-million-dollar policy, this can trigger a surprisingly large tax bill for your heirs.

An ILIT neatly sidesteps this issue by becoming the owner of the policy on your behalf. You contribute money to the trust each year (as gifts), and the trustee uses those funds to pay the premiums. Because you don't technically own the policy, the death benefit bypasses your estate entirely, allowing the full amount to pass to your loved ones, 100% estate-tax-free.

Real-World Example: Imagine a NYC-based entrepreneur with a $10 million life insurance policy. If she owns it herself, that payout could stick her family with a $4 million federal estate tax bill (assuming a 40% tax rate). By putting the policy in an ILIT, the entire $10 million goes directly to her children without losing a dime to estate taxes.

The Dynasty Trust

For families who think in terms of generations, not just years, the Dynasty Trust is the ultimate legacy tool. This trust is specifically designed to hold and grow assets for your children, grandchildren, and even great-grandchildren, all while protecting that wealth from estate taxes at each generational leap.

Normally, when assets pass from a parent to a child, and later from that child to a grandchild, estate taxes can take a bite out of the inheritance each and every time. A Dynasty Trust puts a stop to that. The assets are held in trust for the benefit of each generation, meaning they are never legally "owned" by any individual. This lets the wealth compound over decades, shielded from repeated taxation, creditors, and even divorce settlements.

While many states have rules limiting how long a trust can exist, a well-crafted Dynasty Trust can be set up to last for a very, very long time—sometimes even in perpetuity, depending on the state’s laws.

The Spousal Lifetime Access Trust (SLAT)

A Spousal Lifetime Access Trust (SLAT) is a clever strategy for married couples who want to have their cake and eat it, too. It offers a great mix of tax reduction and indirect access to the funds you've gifted away.

Here’s the basic idea: one spouse (the "grantor") gifts assets into an irrevocable trust that names the other spouse as the primary beneficiary. This move gets the assets out of the grantor's taxable estate immediately. But here's the key—the beneficiary spouse can still receive distributions from the trust. This gives the couple a safety net; they can still tap into the funds if needed, all while those assets are protected from creditors and sit outside their combined taxable estate.

Setting up a SLAT requires careful execution. It’s crucial that the trust is funded with the grantor spouse’s separate property, not joint assets. It's also common for couples to set up SLATs for each other, but the two trusts must be structured differently enough to avoid scrutiny from the IRS.

Which Irrevocable Trust Is Right for You?

Feeling a bit overwhelmed by the options? That’s perfectly normal. This summary table can help you match your main financial goal to the trust designed to achieve it.

| Your Primary Goal | Recommended Trust Type | Best For |

|---|---|---|

| Maximize a life insurance payout for heirs | Irrevocable Life Insurance Trust (ILIT) | Individuals with large life insurance policies who want to avoid estate taxes on the death benefit. |

| Preserve wealth for many future generations | Dynasty Trust | Families focused on creating a long-term legacy and protecting assets from estate taxes for 100+ years. |

| Remove assets from your estate but maintain indirect access | Spousal Lifetime Access Trust (SLAT) | Married couples looking to reduce their combined estate tax exposure while retaining some flexibility. |

Remember, each of these structures is a specialized instrument. The best path forward always involves a conversation with an experienced advisor, like the team at Blue Sage Tax & Accounting Inc., to clarify your objectives and design the trust that will get you there.

Navigating the Tax Implications

Let's talk taxes. It's impossible to discuss irrevocable trusts without getting into the nitty-gritty of how they're taxed. After all, minimizing taxes is often a huge reason for setting one up in the first place. Get this part right, and you can make a massive difference in how much wealth actually makes it to the next generation.

When you move assets into an irrevocable trust, you're interacting with the tax system in a few key ways. We're mainly looking at gift taxes, income taxes, and, of course, the big one: estate taxes. Each has its own rules, and they all work together.

Gift and Estate Taxes: The Main Event

This is where irrevocable trusts really shine. Their biggest superpower is getting assets out of your taxable estate. When you transfer property into the trust, you're making a completed gift. That means the asset—and, crucially, all of its future growth—is no longer on your personal balance sheet when the IRS calculates estate taxes.

For families with significant wealth, this is a game-changer. Think about it: the federal estate and gift tax exemption is $13.99 million per person in 2024, but any amount over that gets hit with a 40% tax. By moving assets into an irrevocable trust, you can protect millions from that tax. This strategy is becoming even more critical because the current high exemption is scheduled to get cut in half in 2026, dropping to around $7 million. You can find more insights on evolving financial trust at the 2025 Edelman Trust Barometer.

By gifting assets now, you effectively "freeze" their value for tax purposes. All the appreciation from that point forward happens inside the trust, completely outside your taxable estate. That move alone can save your heirs a fortune.

So how does it work? You use your lifetime gift tax exemption. Any gifts to the trust above the annual exclusion amount simply get chipped away from your lifetime exemption. The whole idea is to use this exemption strategically while it's still so high.

How Trust Income Is Taxed

Once assets are in the trust, they might start earning income from investments, dividends, or rent. Who pays the tax on that income? It depends on how the trust was structured.

- Grantor Trusts: With this common setup, you, the grantor, continue to pay the income taxes on the trust's earnings. This might sound strange, but it's actually a powerful planning tool. By covering the tax bill yourself, you allow the trust assets to grow completely unburdened by taxes, which is like giving an extra, tax-free gift to your beneficiaries every single year.

- Non-Grantor Trusts: In this case, the trust is its own taxpayer. It files a separate tax return (Form 1041) and pays taxes on any income it holds onto. If income is paid out to beneficiaries, they report it on their personal returns. One word of caution: trusts have very compressed tax brackets, meaning they hit the highest tax rates far more quickly than individuals do.

The Generation-Skipping Transfer (GST) Tax

If your goal is to create a long-lasting legacy for your grandkids or even great-grandkids, you need to know about the Generation-Skipping Transfer (GST) Tax. This is an extra layer of federal tax that kicks in when you transfer wealth to someone who is two or more generations younger than you. It was designed to stop families from sidestepping estate taxes for generations on end.

The GST tax has its own lifetime exemption, which happens to be the same amount as the estate tax exemption. When you're creating something like a Dynasty Trust, it's absolutely vital that your attorney properly allocates your GST exemption to the trust. That's the move that makes the whole structure tax-proof for future generations.

Finally, there’s a crucial trade-off to consider: the "step-up in basis." Typically, when you inherit an asset directly, its cost basis gets "stepped up" to its market value at the time of death, wiping out any capital gains. Assets inside an irrevocable trust, however, generally do not get this step-up. This means if your heirs later sell an asset that has grown in value, they could be looking at a hefty capital gains tax bill. It’s a key conversation to have with your team at Blue Sage Tax & Accounting Inc. to decide which assets are the right fit for a trust.

How to Create and Fund Your Trust Correctly

Setting up an irrevocable trust isn't a casual weekend project—it's a meticulous process that demands clear thinking, professional legal guidance, and precise execution. When done right, it safeguards your assets and solidifies your legacy for decades to come.

Think of it as a four-step journey. It starts with a clear vision of what you want to accomplish and ends with the physical transfer of your assets into the trust. Nail each step, and you'll unlock the true potential of this powerful estate planning tool.

Defining Your Goals and Working with an Attorney

First things first: you need to know why you're creating the trust. Are you trying to slash a future estate tax bill? Shield your assets from potential lawsuits? Or maybe you're planning ahead for Medicaid eligibility. Your specific end game dictates the type of trust you'll need and how it must be structured.

With your goals in hand, it's time to bring in an experienced estate planning attorney. They are the architects who will translate your wishes into a rock-solid legal document. They'll tailor every clause and provision to your unique family dynamics and financial picture, creating a blueprint for your trust's future.

Selecting the Right Trustee

Choosing a trustee is easily one of the most important decisions in this whole process. This individual or institution holds the keys to the kingdom—they manage the trust's assets and distribute them according to your instructions. You essentially have two paths you can go down:

- A Family Member or Friend: This can be a great option if you have someone in your circle who is not only trustworthy but also financially astute and has the bandwidth to take on the role. The only catch is that it can sometimes inject tension or conflict into family relationships.

- A Corporate Trustee: A professional entity like a bank or trust company brings impartiality, deep expertise, and continuity. They live and breathe the complex legal and tax rules, ensuring professional management that can span generations.

The trustee has a fiduciary duty—the highest legal standard of care—to act solely in the best interests of the beneficiaries. This isn't a small favor; it's a serious responsibility that demands integrity, diligence, and a thorough understanding of your wishes.

The Most Important Step: Funding the Trust

An unfunded trust is like a car with no engine. The legal document itself is just paper until you actually transfer your assets into it. This crucial step, known as funding, is where many well-intentioned plans fall apart.

Funding means legally changing the ownership of your assets from your name to the trust's name. This process, called retitling, looks different for different assets:

- Real Estate: You'll need to prepare and record a new deed that officially transfers the property from you to the trustee of your trust.

- Bank and Brokerage Accounts: This involves working directly with your financial institutions to retitle the accounts in the name of the trust.

- Business Interests: Ownership stakes in an LLC, partnership, or other business must be formally assigned over to the trust.

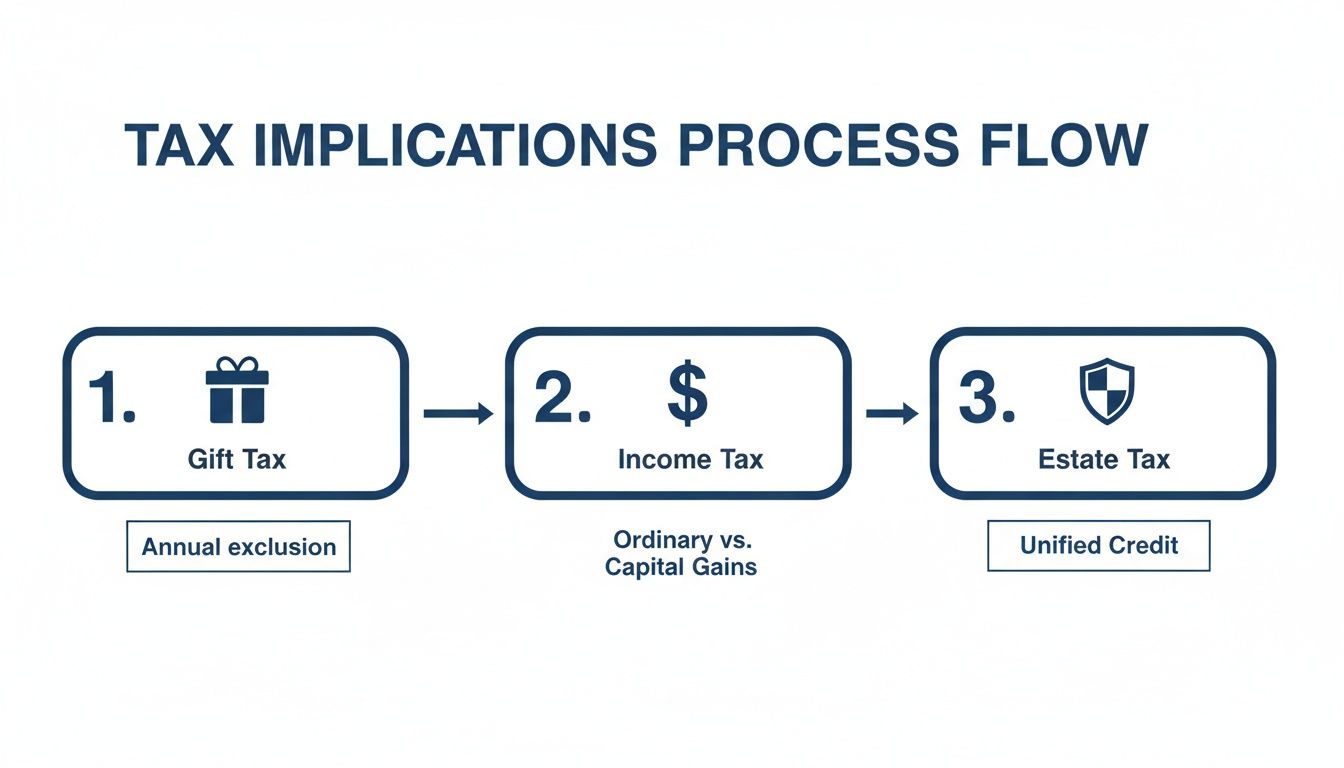

This flowchart gives you a clearer picture of how this funding process kicks off the tax implications.

As the diagram shows, the moment you fund the trust, you trigger potential gift tax consequences, change how income from those assets is taxed, and, most importantly, start the process of removing them from your taxable estate.

Let's be clear: properly setting up a trust is an investment. Initial legal fees can run anywhere from $2,000 to over $20,000, depending on how complex your situation is. There are also ongoing annual costs for trustee services and tax filings. But for high-net-worth families, these expenses are often a drop in the bucket compared to the massive tax savings and protection benefits. You can learn more about how the cost of an irrevocable trust is broken down.

Common Mistakes to Avoid When Setting Up Your Trust

Creating an irrevocable trust is a powerful way to protect your legacy, but it's surprisingly easy to get it wrong. A few simple oversights can completely undermine the whole point. Think of it like building a fortress—a well-designed trust is impenetrable, but a poorly executed one is full of holes. Steering clear of these common pitfalls is the key to making sure your trust actually works the way you imagine.

The biggest and most damaging mistake we see is failing to properly fund the trust. An irrevocable trust is just an empty legal shell until you formally transfer assets into it. People will spend thousands on the perfect legal document, then never take the final, critical step of retitling their house, brokerage accounts, or business interests. An unfunded trust protects absolutely nothing.

Choosing an Unsuitable Trustee

Another huge misstep is picking the wrong trustee. It feels natural to name a spouse or your oldest child, but do they really have the financial savvy, impartiality, or sheer time to do the job right? A trustee has a strict legal obligation—a fiduciary duty—to manage the assets prudently, and they can be held personally liable for messing up.

Here’s a real-world cautionary tale: a business owner appointed his son as trustee for his other children. The son, trying to help his struggling sister, made an improper loan from the trust. This move violated the trust's specific terms, blew up in a bitter family lawsuit, and cost everyone a fortune. The lesson is you need a trustee who is not just trustworthy, but also fully capable of handling complex duties without letting emotions get in the way.

Overlooking Critical Timelines and Rules

Many irrevocable trusts have deadlines and rules that are set in stone. The classic example is the five-year Medicaid look-back period. If you create a trust to shield assets so you can qualify for long-term care, any transfers you make within five years of applying for Medicaid can trigger a penalty, delaying your benefits. It's a strategy that demands you plan far, far ahead.

An irrevocable trust is a forward-looking tool. Last-minute planning rarely works, whether you're trying to qualify for Medicaid or protect assets from a looming lawsuit. Courts can and will "claw back" assets if a transfer looks like it was done to defraud a creditor.

Finally, don't make the trust terms too rigid. Life is unpredictable. Tax laws change, families evolve, and your beneficiaries' needs will shift over time. Drafting a document with zero flexibility can lock your family into a structure that no longer makes sense. A smart move is to build in provisions for a "trust protector" or allow for specific modifications down the road. This gives the trust a crucial safety valve, ensuring it remains a source of security for generations to come.

Your Irrevocable Trust Questions, Answered

Even with a solid grasp of the basics, it's natural to have questions about how an irrevocable trust might fit into your own financial life. Let's walk through some of the most common ones that come up.

Can an Irrevocable Trust Ever Be Changed?

It’s the question everyone asks, and the name "irrevocable" can be a little intimidating. While it does mean you, the creator, can't just wake up one day and decide to change the terms, there are a few exceptions.

In some situations, a trust can be modified with the unanimous consent of every single beneficiary, and often, you'll need a judge to sign off on it too. Modern trusts also sometimes include a "trust protector"—a designated third party who has the limited power to make administrative tweaks, like adapting to a change in tax law. But the bottom line is, once you create it, your direct control is gone.

Who Is on the Hook for Taxes on Trust Income?

This really boils down to how the trust is set up. Is it a grantor trust or a non-grantor trust?

With a grantor trust, you (the grantor) are still responsible for paying the annual income taxes on whatever the trust earns. This might sound like a downside, but it's often a strategic move. By covering the tax bill, you allow the assets inside the trust to grow unburdened, which is essentially like giving an extra, tax-free gift to your beneficiaries each year.

For a non-grantor trust, the trust itself becomes its own taxpayer. It files its own return and pays taxes on any income it holds onto. If the trust distributes income to the beneficiaries, they're the ones who will report it and pay the taxes on their personal returns.

Choosing between a grantor and non-grantor setup is a major strategic decision. It's one of the most important conversations you’ll have with your advisors, as the tax consequences are significant.

What Assets Should I Put Into the Trust?

The ideal assets for an irrevocable trust are the ones you believe have the most potential to grow. Think of it as moving future appreciation out of your taxable estate.

Great candidates often include:

- Stocks and investment portfolios: Any future gains happen outside of your estate.

- Real estate: This is perfect for investment properties or a beloved family vacation home you want to pass down through the generations.

- A stake in a family business: This effectively "freezes" the value of your business interest for estate tax purposes.

- Life insurance policies: An Irrevocable Life Insurance Trust (ILIT) is a classic strategy to ensure the entire death benefit passes to your heirs completely free of estate tax.

One thing to be careful about is funding a trust with assets that have a very low cost basis. Your heirs would lose the "step-up in basis" they'd normally get at your death, which could trigger a hefty capital gains tax if they decide to sell.

How Exactly Does a Trust Protect My Assets From a Lawsuit?

The protection comes from a simple, powerful concept: you no longer own the assets. By legally transferring property to the trust, it's no longer yours. That means if you were to face a lawsuit down the road, those assets are generally shielded from personal creditors or a court judgment.

But there's a catch—timing is everything. The protection isn't instant. If a court finds that you moved assets into a trust specifically to dodge a known creditor, they have the power to "claw back" those assets. That's why it's so important to set up and fund an asset protection trust long before any hint of legal trouble appears on the horizon.

Navigating the specifics of irrevocable trusts requires expert guidance. At Blue Sage Tax & Accounting Inc., we partner with high-net-worth families and businesses in NYC to structure estate plans that protect assets and minimize tax burdens. Schedule a consultation with our team today to ensure your legacy is secure.