When you hear the term “grantor trust,” don’t let the legal jargon intimidate you. At its heart, it’s a specific type of trust where you, the creator, keep just enough control over the assets that the IRS still sees you as the owner for income tax purposes.

Think of it like having a financial remote control. You've placed assets into a separate legal bucket (the trust), but you haven't fully let go of the reins. This structure isn't a loophole; it’s a deliberately designed and incredibly powerful feature used in modern estate and tax planning.

What Exactly Is a Grantor Trust?

Simply put, a grantor trust creates a split in how assets are viewed. For legal purposes, the trust is the official owner. But for tax purposes, the IRS essentially "looks through" the trust and points right back at you, the person who set it up—the grantor.

This means all the trust's financial activity—any income, deductions, and credits—flows directly onto your personal Form 1040. The trust itself doesn't have to file a complicated tax return or pay taxes at the often much higher rates that apply to trusts. It’s a seamless pass-through.

The Key Players in a Grantor Trust

Every trust, grantor or not, involves three main roles. Getting a handle on who does what is the first step to understanding how these powerful tools work.

To make it easier, here's a quick reference guide to the individuals involved and what they're responsible for.

Key Players and Roles in a Grantor Trust

| Role | Description | Key Tax Implication |

|---|---|---|

| The Grantor | The architect. This is the person who creates the trust, sets the rules, and transfers assets into it. | Retains specific powers that cause the trust's income to be taxed to them personally. |

| The Trustee | The manager. This person or institution administers the trust assets according to the rules. They have a legal duty to act in the best interest of the beneficiaries. | Manages the assets but is not responsible for the income tax on trust earnings. |

| The Beneficiary | The recipient. This is the person, people, or entity who will eventually receive the benefit of the trust's assets, either as income or principal. | Receives trust assets without the income being taxed to them (since the grantor pays it). |

Understanding these roles is fundamental to seeing how a grantor trust can achieve its goals, whether that’s privacy, professional asset management, or sophisticated wealth transfer strategies.

This structure has been a cornerstone of U.S. tax strategy for decades. A grantor trust is a powerful estate planning tool where the grantor is treated as the owner for income tax purposes under Internal Revenue Code Sections 671-679, meaning the trust's income flows directly onto the grantor's personal tax return. If you're interested, you can discover more about the historical context of these tax rules and their application in estate planning.

By design, the grantor trust simplifies tax reporting while enabling complex estate planning maneuvers. The grantor pays the taxes, which allows the assets inside the trust to grow for the beneficiaries without being diminished by an annual income tax burden—an effect the IRS views as a tax-free gift.

How Grantor Trust Tax Rules Create Powerful Opportunities

The real magic behind a grantor trust isn't some obscure loophole. It's a direct result of a specific set of rules tucked away in the Internal Revenue Code—specifically, IRC Sections 671-679. These rules spell out certain "strings" or powers a person can keep over a trust.

If the person creating the trust (the grantor) holds onto even one of these powers, it triggers grantor trust status. The immediate effect? The IRS looks right through the trust and taxes all its income directly to the grantor, not to the trust or the beneficiaries. Think of it as a series of tripwires. A skilled estate planning attorney intentionally drafts the trust document to step on one of these tripwires, activating the exact tax treatment we want. It’s a deliberate and strategic move.

The "Tripwire" Powers That Make It All Work

So, what are these powers? While the tax code lists several technical provisions, a few are commonly used to create a grantor trust. These powers give the grantor just enough of a connection to the assets that the IRS says, "For income tax purposes, you're still the owner," even if the trust is irrevocable and the assets are legally out of their hands.

Here are a few of the most popular powers used:

- The Power to Substitute Assets: This is a big one. The grantor keeps the right to swap out trust assets for other assets of equal value. It’s a fantastic way to trigger grantor status without giving the grantor so much control that the assets get pulled back into their taxable estate.

- The Power to Borrow Without Adequate Security: If the trust document allows the grantor to take a loan from the trust without putting up proper collateral, that can also flip the switch to grantor status.

- The Power to Benefit a Spouse: Naming the grantor’s spouse as a potential beneficiary is often enough to do the trick. This is a foundational feature of a popular strategy known as a Spousal Lifetime Access Trust (SLAT).

Choosing the right power is a crucial decision made with your attorney. It depends entirely on your family's goals and the types of assets you're putting into the trust.

Turning a "Tax Defect" Into a Huge Advantage

In planning circles, you'll often hear these trusts called an "Intentionally Defective Grantor Trust" or IDGT. The word "defective" sounds bad, but here, it’s the secret sauce. The trust is only "defective" in the eyes of the IRS for income tax purposes.

But for estate tax purposes, it works perfectly. A properly designed IDGT successfully removes the assets and all their future growth from the grantor's taxable estate. This creates a powerful disconnect that allows high-net-worth families to pass wealth down the line with incredible efficiency.

The core strategy is simple yet profound: By paying the income tax on the trust's earnings, the grantor is effectively making an additional, tax-free gift to the beneficiaries each year. This allows the assets inside the trust to grow completely unburdened by income taxes, supercharging their compounding potential for the next generation.

Best of all, the IRS doesn't consider these tax payments a gift, so they don't eat into the grantor's lifetime gift tax exemption. This lets you move significant wealth completely outside the gift and estate tax system.

For example, let's say a trust earns $100,000 in a year. The grantor pays the $37,000 tax bill from their own pocket. They have just boosted the trust's value by $37,000—essentially giving an extra $37,000 to their heirs without filing a gift tax return. Over decades, these tax-free transfers can add up to millions, preserving a massive amount of wealth for the family.

Grantor Trust vs. Non-Grantor Trust: A Tale of Two Trusts

To really get a handle on what a grantor trust is, it helps to look at what it’s not. Its counterpart is the non-grantor trust, and while both are powerful tools for managing family wealth, they operate in completely different universes, especially when it comes to taxes.

I like to use a simple analogy. Think of a grantor trust as a pane of perfectly clear glass. When the IRS looks at it, they see right through the trust and straight to you, the grantor. The non-grantor trust, on the other hand, is more like a solid wall—it’s a completely separate taxpayer in the eyes of the law.

This single distinction drives almost every strategic decision we make. A grantor trust’s income is reported on your personal tax return using your Social Security Number. In sharp contrast, a non-grantor trust has to get its own Employer Identification Number (EIN) and file its own, separate tax return (Form 1041) every year.

It All Comes Down to Taxes

The most critical difference between these two trust types is how they’re taxed. This isn’t just a small detail; it’s the engine that powers the entire estate planning strategy.

A non-grantor trust is its own taxpayer, and that’s often a problem. Why? Because trust tax brackets are incredibly compressed. In 2024, a trust will hit the highest federal tax rate of 37% after earning just $15,450 in income. To put that in perspective, a married couple filing jointly doesn't hit that same 37% bracket until their income tops $731,200. Ouch.

This punishing tax structure makes non-grantor trusts a poor choice for growing wealth over the long term, as high taxes can quickly eat away at your returns. A grantor trust sidesteps this problem entirely since all the income flows through to you and is taxed at your personal marginal rates, which are often much lower.

A non-grantor trust is a separate taxpayer, stuck with brutally high, compressed tax brackets. A grantor trust is designed to be "invisible" for income tax purposes, passing the tax bill directly to its creator.

This so-called "tax defect" is precisely what makes a grantor trust such a brilliant wealth transfer tool. When you, the grantor, pay the income tax on behalf of the trust, the IRS views it as you simply paying your own tax bill—it is not considered a gift to the trust beneficiaries. This allows the assets inside the trust to grow completely unburdened by income taxes, compounding far more effectively over time.

Control and Flexibility: Who’s in the Driver’s Seat?

Control is the other major fork in the road. Grantor trust status is triggered precisely because the person who created it kept certain strings attached—powers like the ability to swap assets or add a spouse as a beneficiary. This gives you a degree of ongoing influence that can be very comforting.

To create a non-grantor trust, you have to cut those strings completely. The grantor must give up all those specified powers, resulting in a much more rigid and permanent structure. Once it’s set up, you have no say in how it's managed.

This table neatly sums up the key differences.

Grantor Trust vs. Non-Grantor Trust At a Glance

The best way to see the practical differences is to compare them side-by-side. The choice between them depends entirely on your goals for tax efficiency, control, and wealth transfer.

| Feature | Grantor Trust | Non-Grantor Trust |

|---|---|---|

| Taxpayer ID | Uses the Grantor's Social Security Number (SSN). | Must obtain its own Employer Identification Number (EIN). |

| Tax Reporting | Income is reported on the grantor's personal Form 1040. | Files its own separate tax return, Form 1041. |

| Tax Liability | The grantor pays all income taxes on trust earnings. | The trust itself pays taxes on undistributed income. |

| Primary Use | Strategic wealth transfer, estate freezing, and asset protection. | Asset management, creditor protection, and specific legacy planning. |

| Grantor Control | Grantor retains specific powers defined in the tax code. | Grantor relinquishes control over assets and administration. |

Ultimately, a grantor trust is a sophisticated tool for moving wealth out of your estate tax-free, while a non-grantor trust is more of a standalone entity for managing assets for others.

Don't Confuse it With a Simple Revocable Trust

I see this all the time. People hear "grantor trust" and immediately think of the basic revocable living trust they set up to avoid probate. It's a common mix-up, so here’s a simple rule to remember: all revocable trusts are grantor trusts, but not all grantor trusts are revocable.

A revocable trust is the most common type of grantor trust because you can change or cancel it at any time. That absolute control automatically makes it a grantor trust for tax purposes. But the real magic in high-level estate planning comes from using irrevocable grantor trusts. These are the vehicles that let you make tax-free gifts and "freeze" asset values for estate tax purposes—something a revocable trust can never do.

Using Grantor Trusts for Strategic Wealth Transfer

Alright, let's move from the textbook definitions to where the rubber really meets the road. The true power of a grantor trust shines brightest when it's put to work by high-net-worth individuals and family offices looking to move significant wealth to the next generation as efficiently as possible.

These aren't just legal documents; think of them as specialized financial engines. And it's a growing field. The U.S. trusts and estates industry, which is built around tools like these, is on track to hit $290.1 billion in revenue by 2025. That represents a powerful 8.8% compound annual growth rate since 2020, driven by families who are getting serious about planning ahead. If you're curious about the numbers, IBISWorld offers some great insights into this trend.

The Power of an "Estate Freeze" with an IDGT

One of the most effective techniques in an advisor's toolkit is the "estate freeze," and the go-to vehicle for it is the Intentionally Defective Grantor Trust (IDGT). The concept is actually pretty simple: you lock in the current value of an asset that's poised for major growth, ensuring all that future appreciation happens outside your taxable estate.

Imagine you own a thriving family business, a hot tech startup, or a portfolio of investment properties. You just know its value is going to climb over the next decade. Instead of letting that growth add to your future estate tax bill, you can sell the asset to a specially designed IDGT. From that day forward, every dollar of appreciation belongs to the trust—and ultimately, your beneficiaries—completely shielded from estate taxes down the road.

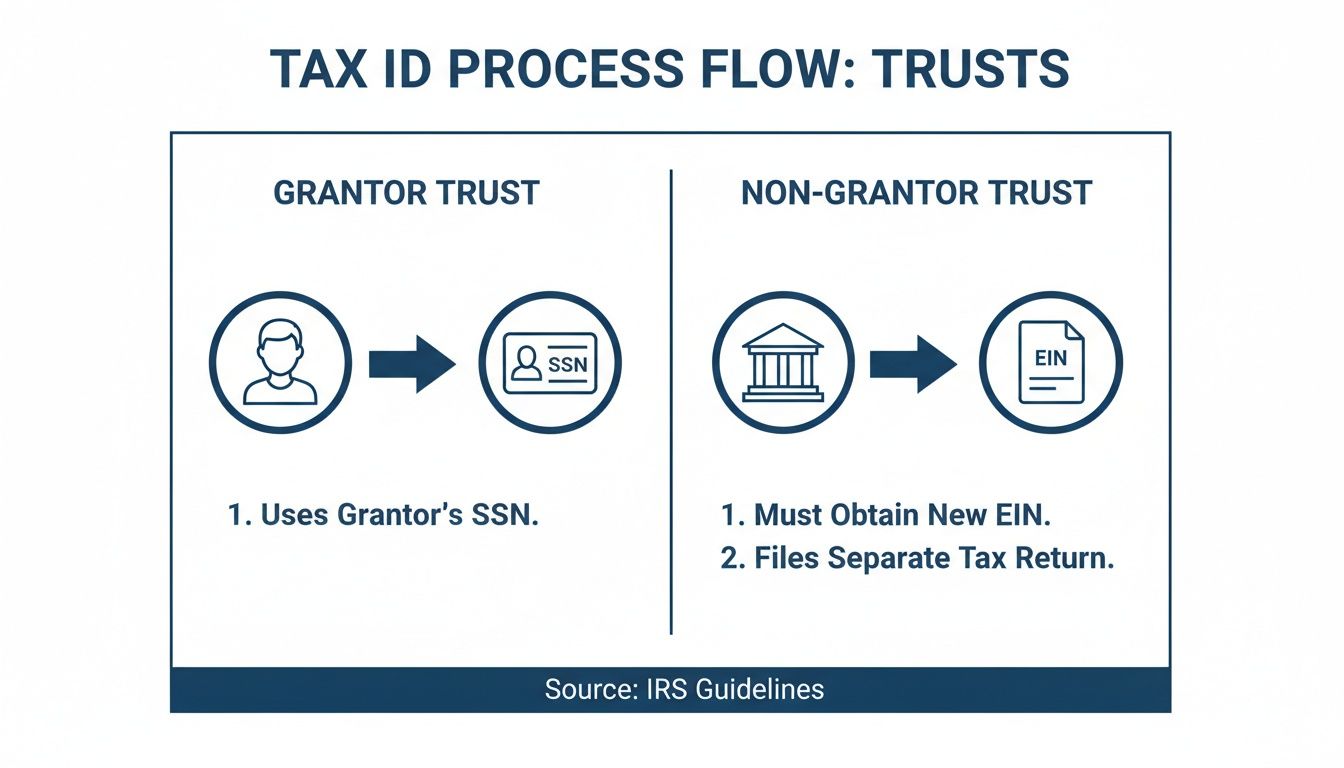

This is where the unique tax structure of a grantor trust becomes critical. The flowchart below shows the fundamental difference in how the IRS sees a grantor trust versus a non-grantor trust.

As you can see, for income tax purposes, the grantor trust is basically you—it uses your Social Security Number. The non-grantor trust, on the other hand, is a separate taxpayer with its own ID. This distinction is the secret sauce that makes these advanced strategies work.

A Real-World Example: Putting the Freeze into Practice

Let's walk through a scenario to make this tangible.

Meet Sarah, a sharp entrepreneur in New York. She owns a commercial building currently worth $5 million, but her projections show it could easily be worth $15 million in 10 years. Her estate is already large enough to be hit by the federal estate tax.

Working with her advisory team, she executes the following plan:

- Seed the Trust: First, Sarah makes a tax-free gift of $500,000 to a new IDGT she's created for her children. This "seed money" (10% of the asset's value) gives the trust real economic footing and acts as a down payment.

- Sell the Asset: Next, she sells the $5 million building to her IDGT. The trust doesn't pay cash; instead, it gives her back a promissory note for $4.5 million (the sale price less the seed money). The note carries a modest interest rate dictated by the IRS, called the Applicable Federal Rate (AFR).

- The "Tax-Free" Sale: Here’s the magic. Because the IRS views Sarah and her grantor trust as the same taxpayer, this sale is a non-event for income tax. She pays zero capital gains tax, which is a huge immediate savings.

- Handle the Income Taxes: The building continues to generate rental income, which now flows into the trust. But because it's a grantor trust, Sarah is still responsible for paying the income taxes on that rent out of her own pocket.

- Watch It Grow: Over the next 10 years, the property's value soars to $15 million. Meanwhile, the trust uses some of its rental income to make the required interest payments to Sarah on the note.

By paying the trust's income taxes each year, Sarah is essentially making additional, gift-tax-free contributions to her children. She's strategically lowering her own taxable estate while letting the trust assets grow and compound without being dragged down by taxes.

Fast forward 10 years, and the results are stunning. The entire $10 million of appreciation happened outside of Sarah's taxable estate. If she had simply held onto the property, that growth would have faced a potential 40% federal estate tax, costing her heirs a staggering $4 million. With the IDGT, she has successfully transferred that wealth completely tax-free, creating a powerful legacy. This is what a well-played grantor trust strategy can do.

Grantor Trusts: Weighing the Pros and Cons

A grantor trust is a powerful tool in the world of estate planning, but it's certainly not the right fit for everyone. Think of it as a specialized instrument—in the right hands, it can create incredible results for wealth transfer, but it comes with its own set of rules and responsibilities.

Before you jump in, it's crucial to look at both sides of the coin. The tax benefits can be fantastic, but they don't come for free. Let's break down the good, the bad, and what you really need to consider.

The Clear Advantages

Why do so many high-net-worth families turn to grantor trusts? It really comes down to a few key benefits centered on tax-savvy wealth growth and control.

-

A "Tax-Free" Gift Every Year: This is the headline benefit. When the trust earns income, you, the grantor, pay the income tax bill. Here's the magic: the IRS doesn't see that tax payment as a gift to the beneficiaries. This means you're essentially making an additional, tax-free gift to the trust each year, allowing the assets inside to grow without being chipped away by taxes. It’s a powerful way to supercharge the wealth you pass on.

-

No Extra Tax Return: Tax time is complicated enough. With most grantor trusts, you don't have to file a separate, often complex Form 1041 trust tax return. All the trust's income and deductions simply flow through to your personal Form 1040. It keeps the paperwork much cleaner.

-

Creditor Protection: If you set up the trust as an irrevocable grantor trust, the assets you put into it are generally shielded from your personal creditors down the road. Once you legally transfer those assets to the trust, they are no longer considered yours, giving your family an important layer of financial protection.

Potential Drawbacks and What to Watch Out For

While the upsides are compelling, you have to be realistic about the challenges. These aren't deal-breakers, but they absolutely require careful planning.

The biggest hurdle is a practical cash-flow issue: you are legally on the hook to pay taxes on income you don’t actually get to spend.

The central trade-off is simple: you must have enough cash on hand, from sources outside the trust, to cover the tax bill the trust's assets generate each year. If you can't, the strategy can quickly turn into a financial burden.

Imagine the trust holds a rapidly growing investment. The tax liability could become quite large over time. You have to run the numbers and make sure you can comfortably handle that obligation year after year without putting a strain on your own lifestyle.

Beyond that, the devil is in the details. The trust document has to be drafted perfectly by an experienced attorney. One wrong phrase or missed clause could mean the trust doesn't qualify for grantor status or, worse, the assets get pulled back into your estate for tax purposes—completely undermining the goal.

Finally, remember that tax laws are not set in stone. What works today might be different tomorrow. A good advisory team will keep you ahead of any legislative changes that could affect your plan.

Is a Grantor Trust Right for You?

So, how do you connect the dots between the technical rules of a grantor trust and your own financial life? This is where the rubber meets the road. Think of a grantor trust not as some abstract legal document, but as a specific tool designed to solve real-world problems for families with growing wealth.

To see if it’s a good fit, we need to shift from theory to a bit of self-reflection. The questions below are designed to get you thinking and set you up for a much more productive chat with your advisors.

A Quick Checklist for Your Financial Picture

This isn't a replacement for professional advice, of course. But spending a few minutes thinking through these points will give you a pretty good idea if a grantor trust should be on your radar. Your answers will highlight the exact issues these trusts are built to address.

-

Do you own assets that are poised for serious growth?

This is the classic starting point. If you own a business, real estate, or a stock portfolio that you expect to appreciate significantly, a grantor trust is a powerful way to get that future growth out of your taxable estate. -

Is your estate value creeping up toward the estate tax exemption limits?

The federal exemption is historically high, but it's set to get cut by about 50% at the end of 2025. And if you're in a state like New York, the local exemption is much lower. If your net worth is in that ballpark, you need a plan.

The real magic of a grantor trust is its ability to transfer future growth. You essentially "freeze" an asset's value for gift tax purposes today, letting all the appreciation from that point forward benefit your heirs—not the IRS.

-

Are you trying to pass wealth to the next generation in the most efficient way possible?

One of the most unique perks is that you, the grantor, pay the trust's income taxes. This might sound strange, but it's essentially a tax-free gift you're making to your beneficiaries every single year, allowing the assets inside the trust to grow and compound much faster. -

Can you comfortably afford to pay taxes on income you won't actually touch?

Here’s the reality check. This strategy only makes sense if you have enough cash flow from other sources to cover the tax bill from the trust's assets without cramping your own lifestyle.

If you found yourself nodding "yes" to a few of these questions, it’s a strong signal that it's time to have a serious conversation about grantor trusts with your team. A firm like Blue Sage Tax & Accounting Inc. can help you model out the specific numbers and see if this powerful strategy aligns with your long-term goals.

Answering Your Top Grantor Trust Questions

As we round out this discussion, let's clear up a few of the most common questions that pop up. These are the things people often wonder about when they first dive into grantor trusts, and getting them sorted out is crucial to seeing the big picture.

Can I Be the Trustee of My Own Grantor Trust?

The short answer is: it depends entirely on why you set up the trust in the first place.

If you have a straightforward revocable living trust designed just to keep your assets out of probate court, then yes, absolutely. It's standard practice for the person who creates the trust (the grantor) to also be the trustee. You keep complete control over everything, which is exactly the point.

But the rules change completely when you're dealing with more sophisticated irrevocable grantor trusts used for estate tax planning, like an IDGT. In that world, making yourself the trustee is a huge misstep. It gives you too much power over the assets, which could lead the IRS to disregard the trust and pull everything right back into your taxable estate. That torpedoes the entire strategy. For these powerful planning tools, an independent trustee is almost always non-negotiable.

Deciding on a trustee isn't just a small detail—it's a critical decision that can make or break the tax advantages of an advanced grantor trust. It all comes down to whether your goal is simple asset management or complex wealth transfer.

What Happens When the Grantor Dies?

The second the grantor passes away, the trust's special "grantor" status vanishes. A revocable trust, for instance, automatically becomes irrevocable. From that moment on, the trust becomes its own separate taxpayer—what’s known as a non-grantor trust.

The successor trustee then takes the reins, following the playbook left in the trust document. This means getting a new tax ID number (EIN) for the trust, filing a final tax return for the person who passed away, and then filing a separate trust income tax return (Form 1041) every year going forward. Their main job is to manage the trust's assets and distribute them to the beneficiaries exactly as the grantor intended.

How Is a Grantor Trust's Income Reported?

This is where things get refreshingly simple, and it's a feature many people love. For income tax purposes, the IRS effectively "looks through" the trust and sees the assets as still belonging to the grantor.

This means all the trust’s financial activity—any income, deductions, or credits—is reported directly on the grantor's personal Form 1040. The trust itself doesn't even file its own income tax return. The trustee simply gives the grantor a statement detailing all the numbers for the year, and the grantor plugs them into their personal return using their own Social Security number. It’s a pass-through system that avoids the headache of a separate, and often more complex, trust tax filing.

Navigating the specifics of grantor trusts requires careful planning and expert guidance. The team at Blue Sage Tax & Accounting Inc. specializes in helping high-net-worth families and businesses structure these tools to meet their long-term financial goals. Explore our tax planning services to see how we can help you build a more secure financial future.