A family office is, at its heart, a private company created to manage the financial life of a single, exceptionally wealthy family. It’s a way to bring all the moving parts of significant wealth—investments, taxes, estate planning, even philanthropy—under one single, professional roof.

The Command Center for Family Wealth

Imagine a family office as the personal headquarters for your family's entire financial enterprise. Instead of you or your family members coordinating with a dozen different professionals—accountants, lawyers, investment advisors, insurance agents—the family office does it for you. It pulls all those functions together.

This structure creates a powerful, unified strategy. Every decision, whether it’s about selling a piece of real estate or funding a charitable cause, is made with a full, 360-degree understanding of the family’s complete financial picture.

This is a world away from traditional wealth management. A private banker might do a great job managing your stock portfolio, but a family office takes a much wider view. It oversees everything: the family’s operating businesses, real estate portfolio, private investments, art collections, and even the family's philanthropic foundation. It's a truly custom-built operation designed to protect and grow wealth for generations to come.

Core Purpose and Function

The main job of a family office is to professionalize how a family’s wealth is managed. When you're dealing with substantial assets, you need a structure that ensures everything is handled strategically and can continue smoothly from one generation to the next.

What does that look like in practice?

- Holistic Oversight: It’s all about connecting the dots. The family office makes sure the tax strategy works with the investment strategy, and that the estate plan properly reflects the family’s charitable goals.

- Dedicated Service: Unlike a big bank or advisory firm juggling hundreds of clients, a family office is completely focused on the needs of just one or a small handful of families. Their success is your success.

- Long-Term Vision: The perspective here isn't about hitting quarterly targets. It's about preserving the family's legacy for the next 50 or 100 years.

A well-run family office is like having a personal CFO, CIO, and COO dedicated solely to your family. It's the engine that drives the entire financial enterprise, navigating complex challenges with a deep understanding of your family’s unique values and goals.

Ultimately, a family office delivers three things that are hard to get anywhere else: total control, absolute privacy, and a level of personalized service that’s simply unmatched.

The table below provides a quick snapshot of these core ideas.

Family Office at a Glance

Here’s a simple breakdown of what defines a family office and its primary role.

| Characteristic | Description |

|---|---|

| Structure | A private company dedicated to managing a family's wealth. |

| Primary Goal | Multi-generational wealth preservation, growth, and transfer. |

| Scope | Manages all financial aspects, from investments to personal affairs. |

| Key Benefit | Centralized control, heightened privacy, and customized service. |

This centralized model is the key to simplifying complexity and building a lasting financial legacy.

Single-Family Versus Multi-Family Office Structures

Once you start exploring the idea of a family office, you'll quickly run into a fundamental choice: should you build a single-family office (SFO) or join a multi-family office (MFO)? These are the two main models, and each offers a very different path to managing significant wealth. The right answer really comes down to your family's specific needs, the complexity of your assets, and what you want for the future.

Think of a single-family office as building your own private, bespoke wealth management firm from the ground up. It's an entire company dedicated to serving just one family—yours. This gives you the ultimate say in everything, from the staff you hire to the investment philosophy you follow. It’s all yours.

On the other hand, a multi-family office is more like an exclusive, members-only club. It’s a professional firm that provides the full suite of family office services to a select group of affluent families. By pooling resources, families get access to top-tier talent and institutional-grade opportunities that would be incredibly expensive to secure on their own.

The Single-Family Office: A Bespoke Approach

A single-family office is the pinnacle of control and privacy. Since it serves only one client, the family is in the driver's seat for every decision. You set the investment strategy, define the risk tolerance, shape the company culture, and steer the philanthropic mission. This dedicated structure means every service can be perfectly customized to your family's unique circumstances.

Of course, that level of personalized service comes with a hefty price tag. Setting up and running an SFO means covering significant costs for salaries, technology, rent, and other overhead. It’s a real business, and it requires serious governance and hands-on oversight from the family.

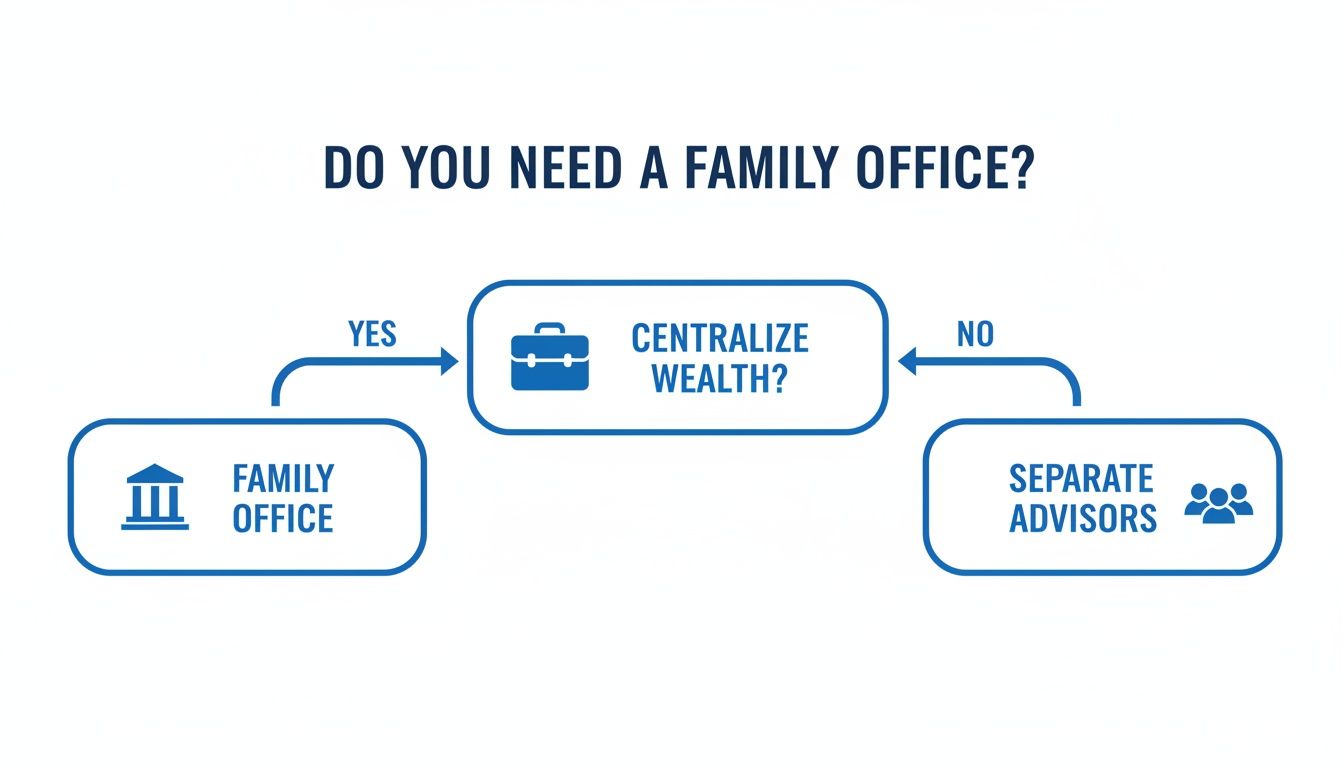

But for families with immense and complex wealth, the cost is often justified by the benefits. This decision tree can help visualize that initial thought process.

As you can see, the core driver is often the simple desire to bring all the pieces of your financial life under one, centrally-managed roof.

The Multi-Family Office: A Collaborative Model

For those who want the benefits without the burden of running their own company, a multi-family office is a fantastic alternative. You get a suite of services very similar to an SFO, but the costs are shared across all the client families. MFOs also have collective bargaining power, which can lead to better pricing on investment platforms and access to exclusive deals you might not see otherwise.

What's the trade-off? You give up a bit of control and total customization. While the services are still highly personalized, they operate within the MFO's established framework. Your family's sensitive information is also managed by a firm that serves other clients, though confidentiality is, of course, a top priority for any reputable MFO.

For many, an MFO hits the sweet spot between expert, comprehensive service and cost-efficiency. This is especially true for families with assets below the $250 million to $500 million threshold typically needed to make a dedicated SFO sustainable.

Comparing Single-Family and Multi-Family Offices

Choosing between an SFO and an MFO really boils down to what your family values most. The table below lays out the key differences to help you see which model best aligns with your goals and financial complexity.

The scale of wealth is often the deciding factor. While some family offices manage as little as $25 million, a recent global survey found the average wealth managed by a family office was $1.8 billion. In that same study, 60% of respondents held $500 million or more in assets. That kind of scale can make an in-house SFO make a lot more sense. You can learn more about family office operational scales to get a feel for the landscape.

| Attribute | Single-Family Office (SFO) | Multi-Family Office (MFO) |

|---|---|---|

| Control | Absolute control over staff, strategy, and culture. | Limited control; services operate within the MFO’s existing framework. |

| Cost | Very high fixed costs for dedicated staff, tech, and infrastructure. | More affordable; costs are shared among multiple client families. |

| Customization | Completely bespoke; services are built from scratch around one family. | Highly personalized, but within a somewhat standardized service menu. |

| Privacy | The highest level of privacy and confidentiality possible. | Excellent privacy, but your information is held by a third-party firm. |

| Services | Can offer a limitless range of services, including very personal tasks. | Core wealth services are comprehensive, but niche concierge services may be limited. |

Ultimately, there's no single "best" answer. The right choice is the one that fits your family's unique DNA—your wealth, your values, and your vision for the future.

What Does a Family Office Actually Do? The Core Services

Think of a family office not as a single service provider, but as the central hub for your family's entire financial world. It’s the command center that ensures every decision—from investments to charity to estate planning—is part of one cohesive strategy designed to protect and grow your wealth for generations.

This integrated approach is where the real value lies. Instead of getting fragmented advice from a separate accountant, lawyer, and investment advisor, a family office brings everyone to the same table. It connects the dots, creating efficiencies and spotting opportunities that are easily missed when your experts work in silos.

Tax and Accounting Oversight

For wealthy families, taxes aren't a once-a-year headache; they're a 365-day strategic game. A family office handles the proactive tax planning and meticulous accounting that are the bedrock of wealth preservation. This is miles beyond just filing returns.

The team navigates a maze of complex compliance issues, especially for families with assets in different states or countries. For instance, a family with homes in New York and Florida has to contend with radically different state and local tax (SALT) rules. The office works to optimize residency, manage property taxes, and legally minimize the family’s overall tax burden.

This also means managing all the financial reporting—from tracking distributions from a private equity fund to pulling together consolidated financial statements for the entire family enterprise.

Investment Management and Strategy

While managing investments is a crucial function, a family office does it with a uniquely long-term view. The goal isn't just to chase short-term market gains but to build sustainable, multi-generational wealth. The investment strategy is built from the ground up to match the family’s specific risk tolerance, values, and need for cash.

A huge perk is getting access to investment opportunities that are off-limits to most people. Family offices are often the first call for exclusive private equity deals, venture capital funds, and direct real estate investments. Their ability to commit significant capital and move quickly makes them highly desirable partners.

A family office's investment mandate is uniquely patient and flexible. It can invest across the entire capital stack, from senior debt to equity, allowing it to structure deals that align perfectly with the family's long-term financial objectives and legacy goals.

Estate and Legacy Planning

One of the most profound roles of a family office is to ensure wealth passes smoothly and efficiently across generations. The office coordinates the entire intricate process of estate and legacy planning, working with top attorneys to draft and maintain wills, trusts, and other essential legal structures.

But it’s about much more than just documents. A key responsibility is preparing the next generation to handle the opportunities and challenges of wealth. The office might facilitate family meetings, lead financial education sessions, or help create a "family constitution" that outlines the family's values and guides future decision-making, helping to keep disputes at bay.

This deep focus on stewardship ensures that the family’s values—not just its assets—are passed down to the next generation.

Philanthropic Advisory and Execution

Many families see their wealth as a powerful tool for making a difference. A family office helps turn that passion for giving into real, measurable impact.

This often involves:

- Setting Up the Right Vehicle: Establishing and managing private foundations or donor-advised funds.

- Giving Strategically: Researching charities to ensure donations align with the family's mission and are put to good use.

- Measuring What Matters: Developing ways to track the social return on philanthropic investments.

By bringing a professional touch to their giving, families can create a charitable legacy that is both meaningful and lasting.

Lifestyle and Concierge Management

Finally, a family office often takes on a whole host of personal and administrative tasks that simplify the family’s day-to-day life. This "lifestyle management" frees up family members' time and mental energy so they can focus on what they truly care about.

These services can be incredibly broad, covering everything from managing household staff and paying personal bills to overseeing property management for multiple homes. It might also include administration for a private jet or yacht, managing an art collection, or even arranging personal security. This high-touch support system is the final piece that provides true, all-encompassing peace of mind.

Governance and Operational Realities

Running a family office is about so much more than just managing money. It’s about building an institution designed to last for generations. The bedrock of that institution is a solid governance structure—think of it as a "family constitution."

This document is the blueprint that guides decisions, heads off potential conflicts, and keeps everyone marching to the same beat, all aligned with a shared mission and values. Without this essential framework, even the most brilliant financial strategies can unravel under the strain of family disagreements or fuzzy leadership.

It lays out everything: how investment decisions get made, how the next generation is brought into the fold and educated about their financial lives, and even how to handle disagreements. It’s the operating system that keeps the family’s wealth engine running smoothly for decades.

Building the Leadership Team

There’s no one-size-fits-all staffing model for a family office. The structure is entirely bespoke, shaped by the family's assets, their complexity, and their long-term vision. A smaller office might run a tight ship with a lean, highly effective team led by a Chief Investment Officer (CIO) and a Chief Financial Officer (CFO), outsourcing specialized tasks as needed.

On the other hand, a larger, more intricate family office might build a powerful in-house team that includes:

- An in-house general counsel for all things legal.

- Dedicated tax and accounting professionals.

- Specialists focused on private equity or real estate investments.

- A philanthropic director to steer the family’s charitable efforts.

The real art is striking the perfect balance between in-house talent and strategic outsourcing. Even the biggest offices lean on external partners for highly specialized advice, ensuring they get top-tier guidance without bloating their payroll.

The right operational structure isn’t about size—it’s about strategic alignment. A successful family office is built to match the family’s unique financial DNA, ensuring that every role and responsibility directly supports the core mission of preserving and growing wealth across generations.

Staffing and Operational Scale in Practice

The reality on the ground is that most family offices, even those managing incredible wealth, are run by deliberately small teams. Research shows that more than half (58%) of single-family offices have fewer than 20 employees, and it's common to see them operating with fewer than five full-time investment professionals.

This lean approach has a major downstream effect, especially when it comes to complex compliance. With such small internal teams, it's just not practical to have deep expertise in every niche, particularly tricky multi-state tax planning involving places like NYC. This is exactly what drives the need for specialized external advisors to fill those critical knowledge gaps. You can discover more insights about family office operations in recent industry reports.

Make no mistake, this operational commitment is significant. Building a family office demands careful thought about not just the services you need, but the people and processes required to deliver them day in and day out. It's a true commitment to building a professional organization that can stand the test of time and serve as the ultimate guardian of your family’s legacy.

How to Build Your Family Office

Deciding to create a family office is a huge transition. You’re moving from a collection of separate advisors to a single, dedicated organization designed to manage your family's wealth and legacy for generations. This isn't just about hiring a team; it's about building a bespoke institution from the ground up.

The first step has nothing to do with money or logistics. It's about looking inward. Before you ever think about legal structures or hiring staff, the family needs to sit down and answer some tough questions. What’s our purpose? What are the core values that will drive every decision we make?

Think of this as creating a "family constitution." This document becomes your North Star, guiding everything from investment choices to philanthropic giving.

The Foundational Checklist for Your Family Office

Getting a family office off the ground is a deliberate, step-by-step process. Every family’s journey is different, of course, but following a structured plan ensures you don’t miss any crucial pieces of the puzzle. This checklist will help you turn the idea of a family office into a functioning reality.

-

Define the Family Mission and Vision: This is the bedrock. Hold a series of family meetings to create a shared purpose, define long-term goals, and agree on the principles that will guide you. This document will shape your entire operation.

-

Establish a Formal Legal Entity: A family office is a real business, and it needs to be treated like one. You'll need to work with legal counsel to set up the right structure, usually a limited liability company (LLC) or a C-corporation, which acts as the central hub for all activities.

-

Create a Comprehensive Business Plan: Map out the services the office will offer, build a detailed budget, and forecast your operating costs for the next three to five years. Be sure to account for startup expenses, salaries, technology, and professional fees.

-

Develop a Governance Framework: You need to decide who has the final say. Will there be an investment committee? A board of directors? An advisory council? Clearly define everyone's roles and responsibilities, and establish a clear process for resolving disagreements.

The most resilient family offices are built on a foundation of clear communication and documented governance. This framework isn't about restriction; it's about creating a predictable, transparent process that preserves both wealth and family harmony.

Deciding What to Handle In-House Versus Outsourcing

Here’s a secret: no family office, no matter how large, does everything themselves. The key to running an efficient and effective office is finding the perfect balance between what you handle internally and what you hand off to outside experts. The goal is to keep your core, mission-critical functions close and get specialized help for everything else.

A smart way to start is by building a lean internal team—often just a CEO or CIO—to manage the big-picture strategy and daily oversight. They are the quarterback.

From there, you can decide what makes sense to delegate:

- Specialized Tax Planning: Your internal CFO can handle the day-to-day finances, but complex issues like multi-state tax (SALT) planning—especially for families with ties to NYC—are almost always outsourced to a specialist firm.

- Advanced Accounting: The accounting for direct investments in private equity or real estate can get incredibly tricky, with complex partnership allocations and reporting. This is a classic area where you bring in external support.

- Legal Counsel: Most offices have a general counsel for oversight but rely on outside law firms for specific needs like litigation, M&A, or crafting sophisticated estate plans.

The decision to outsource isn't just about saving money. It's about getting access to world-class expertise when you need it, without carrying the heavy burden of high, fixed salaries. This hybrid model keeps the family office nimble and powerful.

This strategic thinking is more critical than ever. With nearly 60% of family offices expecting a leadership transition in the next decade and 56% planning to make six or more direct investments a year, the need for specialized advice is exploding. These trends add layers of complexity to tax reporting and estate planning, making expert external partners an indispensable part of any successful family office. You can read the full research about these family office trends to better understand this evolving world.

Your Top Questions About Family Offices Answered

When families start thinking about a family office, a lot of practical questions pop up. It's a big step, so it's natural to wonder about the costs, the right time to start, and how it all works. Let's tackle some of the most common questions we hear.

How Much Money Do You Need for a Family Office?

There's no magic number, but the conversation for a single-family office (SFO)—one built just for your family—usually starts when you have $100 million or more in liquid assets. Anything less, and the steep costs of running a dedicated operation can eat away at the benefits.

But you don't have to wait until you hit that mark. A multi-family office (MFO) is a fantastic route for families with $20 million to $50 million in investable assets. You get access to a full suite of services and expertise, sharing the overhead with other families.

What Does It Actually Cost to Run a Family Office?

The costs can really vary. For a single-family office, you should plan on annual expenses running somewhere between 0.75% and 1.5% of the assets you're managing. If you have a $200 million portfolio, that means a yearly budget of $1.5 million to $3 million to cover everything from staff salaries to technology and legal fees.

Multi-family offices offer a more economical path. Their fees are also based on the assets they manage but are typically lower, often in the 0.50% to 1.00% range. This makes the model much more approachable for a wider range of families.

Remember, it’s not just about the size of your assets; it's about their complexity. A family with $75 million tied up in intricate international businesses might need a family office far more than a family with $150 million parked in simple stocks and bonds.

Is a Family Office Just a Fancy Wealth Manager?

That's a great question, and the answer comes down to scope. A wealth manager is a specialist, laser-focused on one critical job: managing your investment portfolio. They are experts in asset allocation, picking investments, and financial planning directly tied to your portfolio's growth.

A family office, on the other hand, is the quarterback for your family's entire financial life. It manages investments, yes, but it also coordinates everything else—tax strategies, estate plans, charitable giving, and even day-to-day administrative needs.

Think of it this way: a wealth manager is a world-class heart surgeon, while a family office is the chief of medicine for the entire hospital, ensuring every specialist works together seamlessly.

Handling these details is where we shine. Blue Sage Tax & Accounting Inc. delivers the specialized tax and accounting foundation that family offices depend on to protect and grow wealth effectively. Find out how our deep expertise can bring confidence and clarity to your financial life at https://bluesage.tax.