A complex trust is an estate planning powerhouse, giving a trustee a remarkable amount of discretion over how assets are managed and distributed. Unlike its more straightforward counterparts, a complex trust isn't forced to distribute all its income every year.

This key feature means it can accumulate wealth inside the trust, distribute principal when needed, and even make charitable donations. It's this built-in adaptability that makes it such an effective vehicle for growing and protecting wealth across generations.

The Framework of a Complex Trust

Let's move past the dense legal jargon for a moment. Think of a simple trust like a direct deposit—the income hits the account every year, on schedule, without fail. It's predictable and serves a single, clear purpose: pass all income directly to the beneficiaries.

A complex trust, however, is more like a sophisticated investment portfolio. The trustee, acting like a skilled portfolio manager, can decide whether to reinvest the earnings (accumulate income), sell off some core holdings to fund a major life event (distribute principal), or even allocate a portion to a philanthropic cause (make a charitable donation).

This dynamic control is what truly defines a complex trust. The trustee isn't just a courier following a fixed route; they are a strategist making real-time decisions to best serve the long-term vision of the person who created the trust.

Defining Features of a Complex Trust

So, what flips the switch from "simple" to "complex" in a given tax year? A trust is considered complex if it does any one of the following:

- It accumulates income. The trust is allowed to retain some or all of its income rather than paying it all out. This is a game-changer for long-term growth and tax planning.

- It distributes principal. The trustee has the power to give beneficiaries a portion of the trust's core assets (also known as the corpus).

- It makes charitable contributions. The trust instrument permits donations to qualified charities.

A simple trust, by contrast, must distribute all its income annually, cannot touch the principal, and is barred from making charitable gifts. The ability to do any of these three things is precisely what gives the complex trust its name—and its strategic advantage.

A complex trust stands out in estate planning as a flexible legal structure that doesn't follow the rigid rules of a simple trust, offering trustees significant discretion in managing assets. This flexibility allows trustees to strategically hold income during high-tax years or distribute principal to heirs without depleting liquidity, making it a potent tool for high-net-worth families. Discover more insights about trust structures on LegalZoom.com.

For high-net-worth individuals, family offices, and real estate investors—especially in high-tax areas like New York City—this isn't just a minor feature. It’s the cornerstone of sophisticated tax planning, robust asset protection, and the successful execution of a multi-generational financial strategy.

Complex Trust Versus Simple Trust: A Strategic Comparison

To really get a handle on what a complex trust does, it helps to put it side-by-side with its more straightforward cousin, the simple trust. The differences aren't just technical jargon; they represent fundamentally different strategies for managing wealth, protecting assets, and planning for what lies ahead. Pinpointing these distinctions is the first step toward figuring out which structure truly fits your long-term financial goals.

A simple trust is just what it sounds like—it operates on one strict, unbreakable rule. It must distribute all income it earns within the year to its beneficiaries. That’s it. It can't hold onto earnings to grow, and it can't make donations to charity. This structure is predictable but very rigid, trading flexibility for simplicity.

A complex trust, on the other hand, is all about operational freedom. It's defined by what it can do: accumulate income, distribute principal, and make charitable gifts. This flexibility empowers the trustee to make strategic financial moves that can have a massive impact on both the trust and its beneficiaries for years to come.

Income Distribution: Mandatory Versus Discretionary

The most critical difference comes down to how each trust handles its income. A simple trust's mandatory payout rule can sometimes backfire. Imagine a large, required distribution that shoves a beneficiary into a much higher personal tax bracket, effectively shrinking the net value of their inheritance for that year.

A complex trust sidesteps this problem entirely by giving the trustee discretion. The trustee can look at the whole picture—the beneficiary's financial situation, the trust's tax position—and then decide whether to pay out the income or keep it. If holding onto the income is more tax-efficient, they can do just that, letting those funds compound within the trust. This ability to accumulate income is a powerful tool for smart tax planning and long-term wealth growth.

The real power of a complex trust is its ability to adapt. By retaining income or distributing principal, a trustee can react to changing tax laws, beneficiary needs, and market shifts—a level of strategic agility a simple trust just can't match.

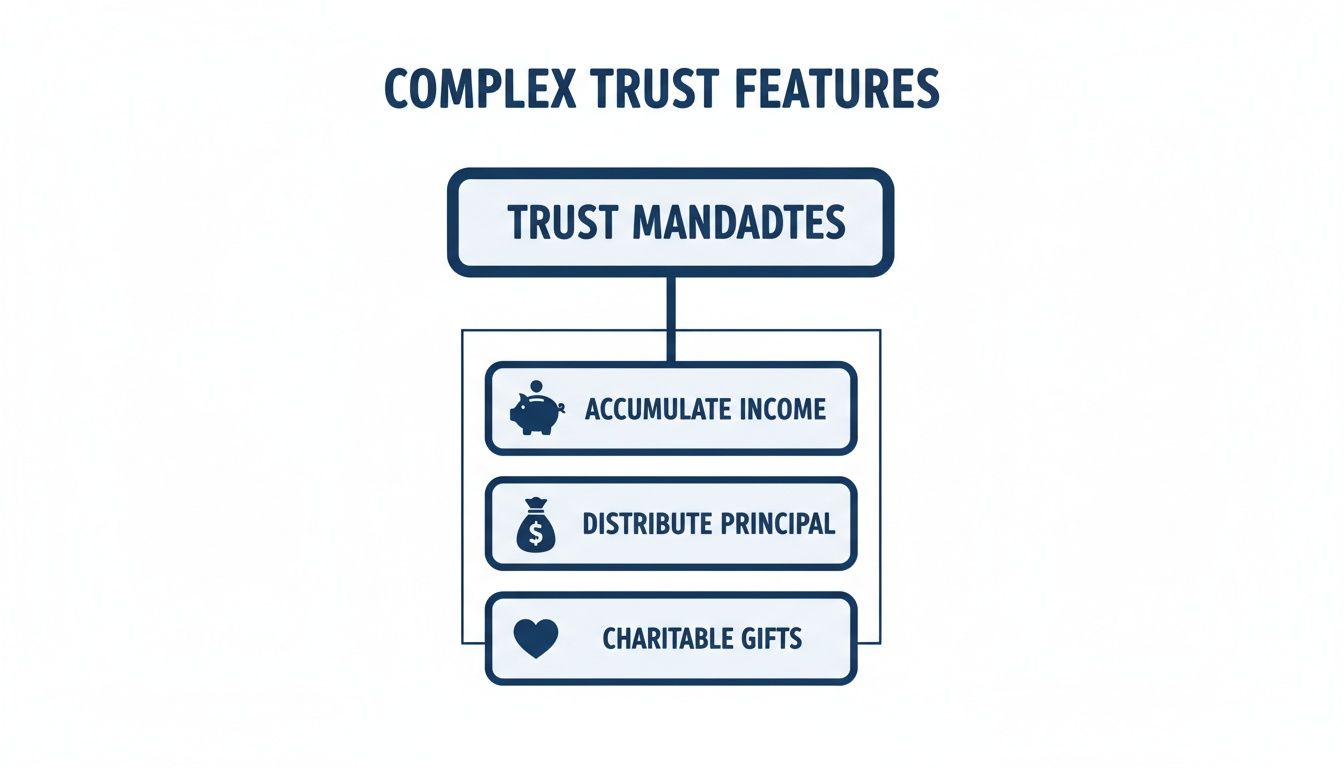

The infographic below highlights the three core capabilities that give a complex trust its unique flexibility.

As you can see, these three powers—accumulating income, distributing principal, and making charitable gifts—are what turn a complex trust from a simple pass-through entity into a dynamic financial tool.

To make these differences crystal clear, let's break them down in a simple table.

Key Differences Between Complex and Simple Trusts

This table offers a side-by-side look at the core features and rules that define these two trust structures, helping to clarify their distinct roles in estate planning.

| Feature | Simple Trust | Complex Trust |

|---|---|---|

| Income Distribution | Must distribute all annual income to beneficiaries. | May accumulate income or distribute it at the trustee's discretion. |

| Principal Distribution | Cannot distribute principal (the "corpus") at any time. | May distribute principal to beneficiaries as needed. |

| Charitable Contributions | Cannot make charitable donations. | May make contributions to qualified charitable organizations. |

| Personal Exemption | $300 | $100 |

| Flexibility | Rigid and predictable. | Highly flexible and adaptable to changing circumstances. |

| Common Use Case | Straightforward wealth transfer where beneficiaries need regular income. | Complex estate planning, wealth preservation, and philanthropic goals. |

This comparison highlights that the choice isn't about which trust is "better," but which one is the right instrument for a specific set of financial and personal objectives.

Principal Distributions: Prohibited Versus Permitted

Another sharp dividing line is how the trust's principal, or corpus, is handled. A simple trust is legally walled off from ever touching its principal assets. Its only job is to pass along the income those assets generate.

A complex trust, however, allows the trustee to distribute the principal itself. This is a game-changer for handling major life events and providing real-world support.

- Helping a Beneficiary: A trustee could distribute principal to help a beneficiary make a down payment on a home, get a new business off the ground, or cover unexpected medical bills.

- Tax-Free Transfers: Principal distributions are generally received tax-free by the beneficiary, providing a way to transfer wealth without triggering a new tax liability for them.

- Strategic Asset Management: The trustee has the option to sell certain assets within the trust and distribute the cash to meet a specific, timely need.

This single capability transforms the trust from a passive income source into an active financial safety net for beneficiaries when they need it most.

Charitable Giving: Disallowed Versus Allowed

For families with a passion for philanthropy, the ability to give back is a major factor in their planning. Simple trusts are completely shut out of this activity, which limits their appeal for anyone who wants to embed charitable giving into their estate plan.

A complex trust, however, can be specifically designed to support charitable causes. The trustee can make donations directly from the trust's assets to qualified charities. This not only fulfills the grantor's philanthropic vision but also generates a valuable tax deduction for the trust, lowering its overall income tax bill. This feature allows a complex trust to become the central pillar of a family's charitable legacy, streamlining their giving and maximizing its impact.

Navigating the Tax Implications of Complex Trusts

Understanding the flexibility of a complex trust is one thing, but mastering its tax implications is where real financial strategy comes to life. The IRS views a complex trust not just as a legal arrangement but as its own distinct taxpayer. This means it has to stand on its own two feet and file an annual income tax return using IRS Form 1041, U.S. Income Tax Return for Estates and Trusts.

This separate taxpayer status is the source of its power. Unlike a simple trust that just passes everything through, a complex trust can hold onto income, pay its own taxes on that income, and make strategic distributions. It’s all about optimizing the tax situation for everyone involved—the trust and its beneficiaries.

Understanding Distributable Net Income

At the heart of trust taxation is a concept called Distributable Net Income (DNI). You can think of DNI as a yearly measuring cup for the trust's income. This cup defines the maximum amount of income that can be passed out to beneficiaries and still be considered taxable to them.

When a trustee makes a distribution, the IRS assumes that money comes from the DNI "cup" first. If the total distributions for the year are less than or equal to the DNI, the beneficiaries will pay income tax on what they received. In turn, the trust gets to deduct those distributions, which cleverly prevents the same income from being taxed twice.

But what if the trustee decides to distribute more than the DNI, maybe by dipping into the trust's principal? That extra amount is generally received by the beneficiary completely tax-free. This DNI mechanism is a fundamental tool for making strategic, tax-efficient transfers of wealth.

A complex trust’s ability to control the flow of taxable income is its greatest strength. By managing distributions relative to its DNI, a trustee can effectively decide who pays the tax—the trust or the beneficiary—and at what rate.

The Challenge of Compressed Tax Brackets

While having a trust pay its own taxes sounds great, there's a major catch: its tax brackets are incredibly compressed. An individual doesn't hit the top federal tax rate of 37% until their income soars past $600,000.

A complex trust, on the other hand, hits that same 37% rate after earning just $15,200 in taxable income (for 2024). That's not a typo. This steep climb means that letting income pile up inside the trust without a solid plan can result in a punishing tax bill.

This is precisely why a skilled trustee is so important. They're constantly performing a balancing act—weighing the benefit of keeping money in the trust to grow against the painful tax cost of doing so. The goal is often to distribute just enough income out to beneficiaries (who are hopefully in lower tax brackets) to sidestep the trust’s high rates, while retaining what's needed to meet its long-term goals.

Key Deductions and Exemptions

Thankfully, a complex trust has a few tools to lower its taxable income before those compressed rates kick in. Smartly managing these deductions is key to keeping the tax liability in check.

- Income Distribution Deduction: This is the big one. It allows the trust to deduct any income it passes along to beneficiaries, effectively shifting the tax responsibility from the trust to the person receiving the money.

- Charitable Contribution Deduction: If the trust document allows for it, gifts to charity are deductible. And here’s a unique perk: a trust can deduct contributions from its gross income, which is a much better deal than the adjusted gross income (AGI) limits that individuals face.

- A Modest Personal Exemption: A complex trust gets a small $100 personal exemption. It isn't much, but it reinforces the trust's status as a separate taxpayer, distinguishing it from a simple trust, which gets a $300 exemption.

These tax dynamics are what make complex trusts a go-to strategy for high-net-worth families. According to IRS trust income statistics, data from 2021 shows complex trusts reported over $250 billion in gross income, and 65% of them chose to retain some of those earnings. This allows trustees to pay taxes at the trust level, a move that can be a big win, especially when beneficiaries live in high-tax states like New York.

Effectively managing these tax intricacies is certainly not a DIY project. It demands careful, forward-looking planning and deep expertise—especially when state and local tax (SALT) laws add another layer of complexity. To truly unlock the potential of a complex trust, partnering with an experienced tax advisor is absolutely crucial.

Real-World Applications for Investors and Families

The theory behind a complex trust is interesting, but its real power comes to life when you see it applied to actual financial situations. This isn't just an abstract legal tool; it's a practical and powerful vehicle used by entrepreneurs, investors, and families to navigate very real challenges.

Let’s walk through a few scenarios. In each one, you’ll see how the unique flexibility of a complex trust helps achieve common goals for high-net-worth clients: growing a business, preserving wealth, minimizing tax exposure, and protecting a legacy for the next generation.

Managing a Real Estate Portfolio

Picture a real estate investor with a growing portfolio of rental properties across New York City. She has two main goals: keep expanding her holdings by acquiring new buildings and provide for her two children—one in college and the other launching a startup.

She establishes a complex trust and transfers the properties into it. Now, all the rental income flows into the trust, not her personal bank account. This simple move unlocks a few significant advantages.

-

Fueling Growth with Accumulated Income: Instead of taking all the rental profits as personal income (and paying high personal tax rates), the trustee can hold onto a portion of the cash inside the trust. This pool of capital becomes the dry powder for the next down payment, allowing the portfolio to grow organically without her needing to constantly inject her own post-tax money.

-

Providing Tax-Smart Support to Heirs: When her kids need capital for tuition or their new business, the trustee can make distributions from the trust's principal—that is, the original property value or accumulated capital. These are not income distributions. As a result, the children generally receive the funds tax-free, giving them a clean capital injection without a new tax headache.

The trust essentially becomes the central operating entity for her real-estate enterprise, cleanly separating her business assets from her personal life while creating an efficient engine for both reinvestment and family support.

The Family Office and Asset Protection

Now, let's consider a multi-generational family office overseeing a diverse portfolio of stocks, private equity, and other investments. Their top priorities are shielding these assets from creditors and streamlining their extensive charitable giving. A complex trust is practically built for this.

The family moves a significant portion of its investment assets into an irrevocable complex trust. This immediately creates a formidable layer of asset protection. Since the family members no longer legally own these assets directly, they are insulated from personal lawsuits, divorces, or creditor claims.

For families with substantial wealth, a complex trust is more than an estate plan; it's a fortress. It secures assets against unforeseen risks while providing the operational flexibility to manage investments and philanthropic missions effectively.

The trust document is also drafted to handle the family's philanthropy. The trustee can make sizable donations directly from the trust's assets to designated charities. This strategy hits two birds with one stone:

- Centralized Philanthropy: It simplifies the family's giving, creating a single, organized channel for all contributions.

- Tax Efficiency: The trust claims a full charitable deduction for these donations, which can dramatically reduce the taxable income generated by the investment portfolio. This means more capital stays within the trust to grow and fund future giving.

Business Succession for the Entrepreneur

Finally, think about an entrepreneur who has poured her life into building a successful manufacturing business. She plans to retire in the next decade and wants to transition ownership to her children, but she knows a sudden handover could be chaotic. She also needs to prepare for a potential sale or liquidity event down the line.

She works with her advisors to create a complex trust, placing her ownership stake in the business into it. An independent professional is appointed as trustee to oversee the long-term succession plan.

Here's how it works in practice: The trust accumulates business profits year after year. This cash can be used to fund buy-sell agreements among the children or provide the necessary liquidity to handle estate taxes when the time comes.

During the transition, the trustee has the discretion to make distributions—some to the founder for her retirement income, and some to her children as they step into larger roles. This structure creates a stable, legally-enforced roadmap for the company's future, ensuring her legacy is protected long after she's left the corner office.

The Critical Role and Responsibilities of a Trustee

A complex trust is an incredibly powerful tool, but it's only as good as the person or institution steering the ship—the trustee. This isn't just an administrative gig; it's a position built on immense trust and serious legal responsibility. The role demands a sharp mind for finance, solid judgment, and an unwavering commitment to the person who created the trust (the grantor).

Every decision a trustee makes directly affects the financial health of the beneficiaries and the future of the trust itself. They are held to a very high legal standard, bound by what are known as fiduciary duties. This simply means they must always put the interests of the trust and its beneficiaries first, without exception. Understanding these duties is key to grasping what a complex trust is and, more importantly, who you can trust to manage it.

Core Fiduciary Duties Explained

While the legal nitty-gritty can get complicated, a trustee's responsibilities really boil down to three core principles. These are the guideposts for every action they take, from investing assets to distributing funds to a beneficiary.

- Duty of Loyalty: The trustee’s loyalty must be absolute. They must act solely for the benefit of the trust and its beneficiaries, period. This means no self-dealing, no conflicts of interest, and no actions that could personally benefit the trustee at the trust's expense.

- Duty of Prudence: Think of this as the "common sense" rule on steroids. A trustee has to manage the trust's assets with care, skill, and caution. This involves making smart investment decisions, diversifying to manage risk, and staying away from overly speculative ventures that could put the principal at risk.

- Duty of Impartiality: When a trust has multiple beneficiaries with different needs—like a child who gets income now and a grandchild who will inherit the principal later—the trustee can't play favorites. They must balance these competing interests fairly and objectively.

These duties aren't just suggestions; they are legally binding. A trustee who messes up can be held personally liable and face serious legal trouble.

The Practical Challenges of Discretion

Here’s where the job gets really tough. Unlike a simple trust that often has fixed payout rules, a complex trust gives the trustee discretion. This means they have to make tough judgment calls with real financial and personal consequences.

For instance, the trustee has to decide whether to pay out income to a beneficiary or keep it inside the trust to grow. This isn't a simple guess. It requires a careful look at the trust's punishingly compressed tax brackets versus the beneficiary's own tax situation to figure out the most tax-efficient move for the entire family.

A trustee of a complex trust is not just a manager of assets, but a steward of the grantor's intent. Their ability to navigate intricate family dynamics, tax laws, and market conditions is what transforms a legal document into a living, effective legacy.

And it’s a constant tightrope walk. They have to balance the needs of a current beneficiary who might need more income today against the needs of future beneficiaries who are counting on that principal to grow over the long haul.

Meticulous Record-Keeping and Tax Compliance

On top of the big strategic decisions, the trustee is also on the hook for all the administrative and tax compliance work. This is a non-negotiable part of the job that requires painstaking attention to detail.

Key administrative tasks include:

- Keeping detailed, accurate financial records for every single transaction.

- Filing the trust's annual Form 1041 tax return with the IRS.

- Issuing Schedule K-1s to each beneficiary, which tells them their share of the trust's income, deductions, and credits to report on their personal tax returns.

Given how much is at stake, choosing the right trustee is one of the most important decisions a grantor will ever make. Working with professional advisors isn't just a good idea—it's essential for making smart choices, ensuring the grantor's vision is carried out, and minimizing both financial and legal risks down the road.

It Takes a Team: Partnering with an Expert for Your Trust Strategy

We've covered a lot of ground, from what a complex trust is to its incredible power for flexible wealth management, tax planning, and even charitable giving. The ability to accumulate income and make discretionary distributions of principal makes it an essential tool for anyone managing significant assets.

But as we've seen, all that power and flexibility comes with a matching level of complexity. Navigating the nuances of Form 1041 and those notoriously compressed tax brackets isn't something to take lightly.

Trying to go it alone with a complex trust is, frankly, a huge risk. The margin for error is razor-thin. A misstep in compliance, a poorly timed distribution, or a mistake in multi-state tax planning can unravel your strategy and lead to serious financial consequences. This is precisely why having a dedicated professional partner isn't a luxury—it's essential.

Why Expert Guidance Is Not Optional

For high-net-worth families, entrepreneurs, and family offices, a complex trust is a living, breathing financial vehicle, not a static document you file away. It demands active management and ongoing strategic input to work as intended. A true advisor does far more than just keep you compliant; they partner with you to unlock the trust’s full potential.

This partnership involves:

- Proactive Tax Planning: Actively strategizing distributions to keep assets out of the trust’s punishingly high tax rates and in the hands of beneficiaries.

- Navigating Multi-State Rules: Untangling the web of state-specific tax laws, especially in high-tax jurisdictions like New York.

- Supporting the Trustee: Arming the trustee with the clear financial data they need to make sound, defensible fiduciary decisions.

A complex trust is the architectural plan for your financial legacy. But a plan is just a piece of paper without a master builder. An expert advisory partnership is what turns that blueprint into a strong, tax-efficient structure that stands for generations.

At Blue Sage Tax & Accounting, we live in the details of trust administration and tax strategy, serving clients across New York City and beyond. We know that cookie-cutter solutions don't work when you're building a legacy.

Your life's work deserves more than just a plan; it deserves meticulous execution and expert oversight. If you're ready to see how a well-managed complex trust can secure your family's future, let's talk.

Schedule a consultation with Blue Sage Tax & Accounting today, and let's start building a strategy that preserves and grows your wealth for the years ahead.

Frequently Asked Questions About Complex Trusts

Even after you get the hang of what a complex trust is, a lot of practical questions still come up. Let’s tackle some of the most common ones I hear from clients to clear up how these powerful tools actually work in the real world.

Can a Trust Change from Simple to Complex?

Absolutely. This is a critical point that many people miss. A trust's status as "simple" or "complex" isn't set in stone; we actually determine it year by year for tax purposes.

Think of it this way: if a trust pays out all its income in one year, it files its tax return as a simple trust. The very next year, if that same trust holds onto even a little bit of income or makes a distribution from its principal, it operates and files as a complex trust. This annual flexibility is a powerful tool, but it also means the trustee has to keep meticulous records to justify the trust's classification each tax year.

The ability to toggle between simple and complex status year after year is a key strategic lever. A savvy trustee can use this to optimize the tax outcome for both the trust and its beneficiaries, reacting to new financial realities as they happen.

Are All Distributions from a Complex Trust Taxable?

No, and this is where complex trusts really shine for transferring wealth. A beneficiary is only taxed on distributions up to the amount of the trust's Distributable Net Income (DNI) for that year. Anything beyond that can be a tax-free transfer of principal.

Here’s a practical example: say a trust has a DNI of $50,000. The trustee decides to distribute $80,000 to a beneficiary to help with a down payment on a house. The tax situation breaks down like this:

- The first $50,000 is treated as income and is taxable to the beneficiary.

- The extra $30,000 is a distribution of the trust's principal (or corpus) and is generally received by the beneficiary completely tax-free.

This distinction allows trustees to make significant capital transfers for major life events without saddling the beneficiary with a massive, unexpected tax bill.

What Are the Main Downsides of a Complex Trust?

For all their benefits, complex trusts aren't a walk in the park. The main drawbacks are the increased administrative complexity and the higher costs to run them properly. The trustee has a lot on their plate—they need to be skilled at juggling investment decisions, the beneficiaries' needs, and some pretty thorny tax rules.

This means more sophisticated accounting, rigorous record-keeping, and a more involved tax preparation process for Form 1041. And as we've covered, the compressed tax brackets are no joke. Any income left in the trust can hit that top federal rate of 37% with startling speed. Without a proactive strategy to manage that retained income, the tax drag can be significant, which is why professional oversight is so crucial.

Navigating these nuances demands a deep understanding of both trust administration and tax law. At Blue Sage Tax & Accounting, we specialize in providing the expert guidance needed to make sure your complex trust is an asset, not a burden. Schedule a consultation with Blue Sage Tax & Accounting to protect your wealth and secure your financial legacy.