A state tax lien is the government's way of putting a legal "dibs" on your property when you owe back taxes. It's a public claim that secures the state's interest in your assets, making sure they get paid first if you sell or transfer your property. This isn't just a minor administrative note; it's a powerful legal tool that can freeze your ability to sell, refinance, or even give away assets until the tax debt is fully settled.

Breaking Down the State Tax Lien

Imagine the state placing a giant, official sticky note on everything you own—your house, your car, your business inventory. That's essentially what a tax lien does. It doesn't mean they’re kicking you out of your home tomorrow, but it does give them a legally recognized claim to your assets to cover what you owe.

The whole point is to secure the debt. By filing a lien, the state government jumps to the front of the line of creditors. If you sell a piece of property, for instance, the state gets its money from the sale proceeds before you see a dime.

Common Triggers for a State Tax Lien

A state tax lien is never a surprise. It's the final step after a series of notices and collection attempts have gone unanswered. The most common reasons one might be filed are:

- Unpaid Income Taxes: This is the big one, affecting both individuals and corporations who haven't settled their state income tax bills.

- Delinquent Sales Taxes: A frequent issue for businesses that collect sales tax from customers but then fail to send those funds to the state.

- Outstanding Property Taxes: Although often a local county matter, unpaid property taxes can also escalate to a state-level lien.

It's critical to know the difference here: A lien is the legal claim against your property to secure a debt. A levy is the actual act of seizing that property to satisfy the debt. The lien is the warning; the levy is the enforcement.

To better understand how a lien works, it helps to know who the key players are. This table breaks down the roles and responsibilities in a typical state tax lien scenario.

State Tax Lien at a Glance

| Component | Description | Primary Role |

|---|---|---|

| Taxpayer | The individual or business entity with the outstanding tax debt. | Responsible for the underlying debt and its ultimate resolution. |

| State Tax Agency | The government body in charge of tax collection, like the NYS Department of Taxation and Finance. | Issues the initial tax bill, files the official lien, and manages collection efforts. |

| County Clerk/Recorder | The local government office where property records are maintained. | Makes the lien a public record, which notifies creditors and clouds the property's title. |

Each party has a distinct and crucial function, from the taxpayer who owes the debt to the county clerk who makes that debt a matter of public record, impacting credit scores and real estate transactions.

How a Tax Lien Attaches to Your Property

A state tax lien doesn't just materialize out of nowhere. It's the end result of a formal, step-by-step legal process that turns an unpaid tax bill into a powerful claim against everything you own. The journey starts long after your tax payment was originally due.

It all begins with an assessment. The state tax agency calculates what you owe and sends you a bill. If that bill goes unpaid and unchallenged, the next step is a formal Notice and Demand for Payment. Think of this as the final warning. Ignoring it is what gives the state the green light to establish a lien against you.

At this stage, the lien technically exists, but it’s still an internal government matter. To give it real teeth and make it enforceable against others—like lenders, creditors, or potential buyers—the state has to take one more crucial step.

Perfecting the State Tax Lien

This is where the lien goes public. To "perfect" it, the state files a document, usually called a Notice of State Tax Lien, with a public office like the county clerk or recorder. This action puts the world on notice that the state has a legal claim to your property.

Once that notice is filed, the lien’s power grows exponentially. It acts like a kind of financial superglue, attaching not just to the property you owned when the tax was due, but to nearly all assets you currently have and any you acquire in the future, for as long as the lien remains active.

A perfected lien creates a "cloud on title"—a legal term for any claim or issue that makes a property’s ownership uncertain. This cloud has to be cleared before the property can be sold or refinanced, effectively locking up your assets.

Specific vs. General Liens

It's vital to understand the scope of the lien you're facing, as they generally come in two flavors.

-

Specific Lien: This type is laser-focused on a single piece of property. The classic example is a property tax lien, which is secured only by the real estate on which the taxes are owed.

-

General Lien: This one is far more menacing. Liens for unpaid income, sales, or withholding taxes are almost always general liens. They attach to all of your property and rights to property—your house, cars, bank accounts, investments, and even your business assets.

For business owners and high-net-worth individuals with diverse portfolios, a general lien is a nightmare. It can freeze an entire collection of assets over a single tax debt, causing widespread financial paralysis. This is exactly why it’s so critical to handle any state tax issue long before it escalates to a perfected, public lien.

The Real-World Consequences for Owners and Businesses

A state tax lien isn't just a piece of paper filed away in a county clerk's office. It casts a long, dark shadow over your financial life, with tangible consequences that can stop you—and your business—dead in your tracks.

The most immediate and common headache is the "cloud on title" it places on your real estate. In simple terms, this legal claim makes it virtually impossible to sell or refinance the property. No sane buyer will close, and no lender will approve a new mortgage, until that lien is paid off and formally removed from the public record. Your property is effectively shackled.

Frozen Assets and Shattered Credit

But the damage doesn't stop at your front door. A state tax lien is public information, which means credit reporting agencies find it quickly. Once it hits your credit report, your score can plummet. Suddenly, getting any kind of new financing—from a simple car loan to a critical business line of credit—becomes incredibly difficult and far more expensive.

Think about a real estate developer on the verge of breaking ground. An unexpected state tax lien surfaces, attaching to her business assets. Her construction financing is instantly frozen. Just like that, expansion plans evaporate, contractors are idled, and the entire project is thrown into jeopardy over a single tax dispute.

For a business, this kind of operational paralysis can be devastating. With a lien slapped on company assets, you can forget about securing new loans, attracting investors, or even selling the business. That lien is a bright red flag signaling financial instability, scaring off the very partners and lenders you need to survive and grow.

The Looming Threat of Seizure

A lien is a claim, but it's also the legal stepping stone to a levy—the actual seizure of your property. Once a lien is in place, the state has the right to force the sale of your assets through foreclosure to get its money back. What started as a financial problem can escalate into losing your home, your commercial building, or other core assets.

This isn't a rare occurrence. Data reveals that property tax delinquency rates in states that use tax liens average 6.2%, a noticeably higher figure than in states without such systems. You can find more insights about rising property tax delinquencies on Cotality.com.

Here’s a quick rundown of what you’re up against:

- Blocked Real Estate Transactions: You can't sell or refinance until the debt is cleared. Period.

- Devastated Credit Score: A public lien can damage your personal and business credit for years to come.

- Risk of Foreclosure: The state can ultimately seize and sell your property to collect what it's owed.

- Crippled Business Operations: Access to capital is choked off, halting growth and threatening day-to-day survival.

Understanding Lien Priority: State vs. Federal Claims

When more than one creditor has a claim on the same piece of property, things get complicated fast. The big question is: who gets paid first? The answer comes down to lien priority, which is basically a legal pecking order that dictates who gets their money and in what sequence when a property is sold or foreclosed on.

Think of it like a line at the bank. Each creditor, whether it's a mortgage lender, the state tax authority, or the IRS, has a place in that line.

The foundational rule for lien priority is simple: “first in time, first in right.” This principle means that liens are typically prioritized in the order they were officially recorded. If a mortgage was recorded in 2020, a federal tax lien in 2022, and a state income tax lien in 2023, that’s exactly the order they’d get paid out. Simple, right?

Well, not always. There's a major exception that can completely shuffle the deck.

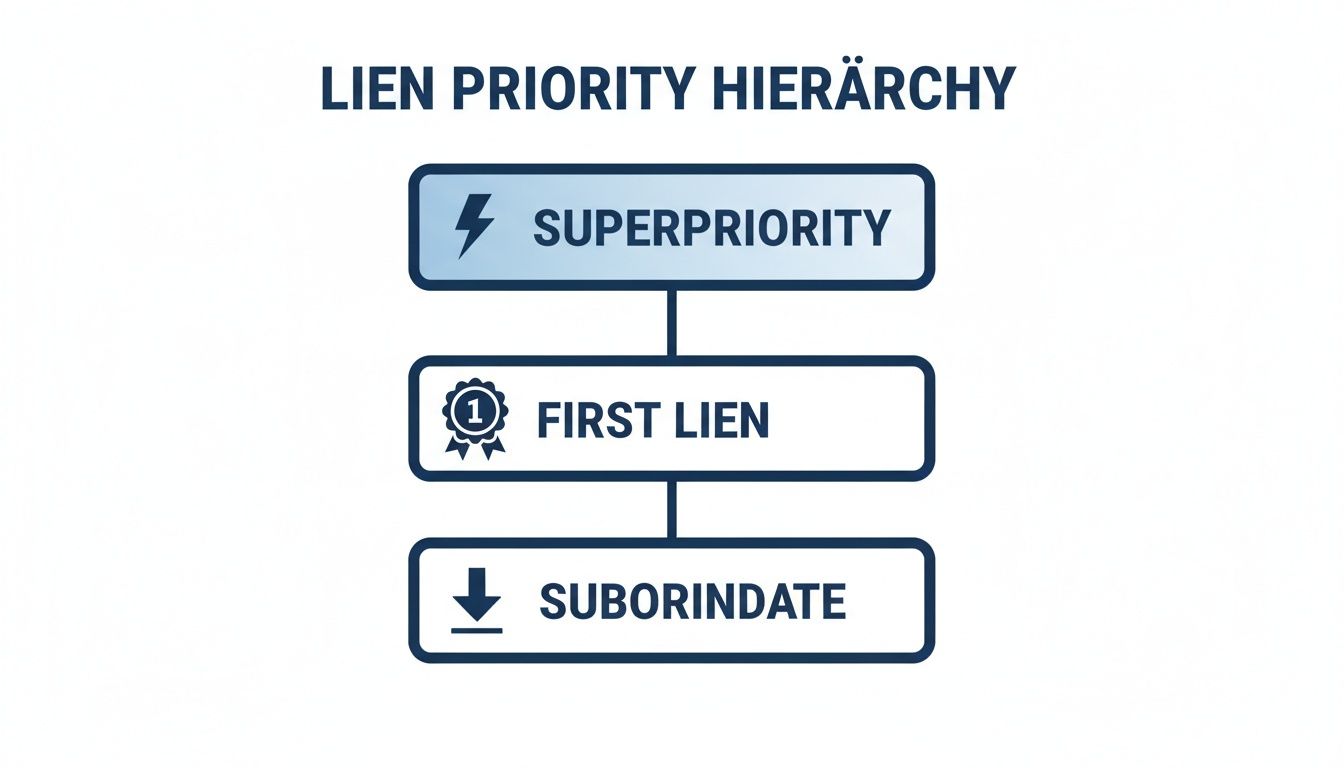

The Superpriority Exception

Certain state and local property tax liens get a special hall pass called superpriority. This lets them jump to the very front of the line, no matter when they were filed. They can even leapfrog a mortgage that’s been on the books for decades.

A superpriority lien bulldozes the "first in time" rule. It's designed to ensure that local governments get paid for essential services funded by property taxes before anyone else—including the IRS and private mortgage lenders.

If you're a real estate investor with a leveraged portfolio, this isn't just an interesting legal quirk; it's a critical risk factor. A small, overlooked property tax bill could suddenly take precedence over the primary lender, completely upending the financial security of the asset.

Federal vs. State: The Ultimate Authority

When federal and state tax liens are competing for the same asset, the hierarchy can be a bit tricky. While the "first in time" rule generally applies between them, federal law gives the IRS some serious muscle. Under Section 6321 of the Internal Revenue Code, the federal government’s lien is incredibly powerful and can sometimes steamroll state-level creditor protections.

For instance, a federal tax lien can attach to a taxpayer’s interest in a multi-member LLC and potentially force the sale of the entire business to satisfy the debt. That's a move most other creditors would be blocked from making under state law. It’s a stark reminder of the federal government’s sweeping power to collect.

Grasping this hierarchy isn't just for lawyers. It's essential for:

- Property Owners: It tells you which debts are the most immediate threat to your assets.

- Investors: It's a non-negotiable part of due diligence when evaluating a potential acquisition.

- Lenders: It directly impacts the security of their collateral against unexpected government claims.

At the end of the day, lien priority isn't just an abstract legal concept. It's the practical framework that determines who wins and who loses in any property-related financial dispute.

Navigating the Maze of State-Specific Lien Rules, with a Spotlight on New York

Grasping the general concept of a state tax lien is one thing; navigating the reality is another entirely. There’s no federal playbook here. The rules for how liens are filed, prioritized, and enforced can change dramatically the moment you cross a state line.

What trips most people up are the local differences in things like redemption periods, interest rates, and foreclosure processes. A redemption period—the time a property owner gets to settle their tax debt after a lien is sold—can be a generous window in one state and a brutally short deadline in another, pushing a property toward foreclosure much faster. The same goes for interest and penalties, which can either be a manageable cost or a crushing financial burden.

A Closer Look at New York’s Tough Terrain

New York is a perfect example of how complex and aggressive these systems can be. It operates on a hybrid model, which means municipalities can either sell the tax lien certificates to private investors or jump straight to foreclosing on the property themselves. This creates a patchwork of different procedures from one county to the next.

What really sets New York apart are its notoriously high statutory interest rates. These can make it incredibly expensive for a property owner to get back on solid ground. For an investor, it looks like a high-yield opportunity, but it’s a landscape littered with procedural landmines. One wrong step, and your ability to enforce that lien is gone.

This diagram shows how different claims on a property stack up, and how a lien with superpriority can completely change the game.

As you can see, those superpriority liens don't wait their turn. They cut right to the front of the line, demanding payment before anyone else—even the primary mortgage holder.

State tax liens are a powerful collection tool for governments. They also create a unique market where investors can purchase tax lien certificates, often at auction, and earn significant interest if the owner redeems. Some states offer incredible returns—Illinois can hit an effective 36% annually, while Florida’s rate is capped at 18%. These are government-backed returns that are hard to find anywhere else. You can find more critical facts for real estate investors on Amerisave.com.

Comparing Key States

To see just how different the rules can be, let’s put three major states side-by-side. The table below gives you a quick snapshot of the unique risks and rewards tied to each state’s regulations.

| Feature | New York | Florida | New Jersey |

|---|---|---|---|

| Lien Type | Tax Lien State (Hybrid) | Tax Lien State | Tax Lien State |

| Max Interest Rate | Varies by municipality (often high) | 18% (bid-down auction) | 18% + penalties |

| Redemption Period | 1 to 2 years typically | 2 years | 2 years (can be reduced) |

These variations make it crystal clear: a one-size-fits-all approach is a recipe for disaster. Whether you’re an investor scouting opportunities across the country or a business owner managing complex state and local tax (SALT) obligations, you absolutely must understand the local ground rules to protect your interests.

Proven Strategies for Resolving a State Tax Lien

Discovering a state tax lien has been filed against you can be a shock, but it’s not a financial life sentence. While simply writing a check for the full amount is the quickest way to make it go away, that’s not a realistic option for most people.

Fortunately, you have other powerful tools at your disposal. States have established clear pathways to manage, reduce, or completely remove a lien, each designed for different financial realities. Let's walk through them.

Negotiating a Payment Solution

For many taxpayers, the problem isn't an unwillingness to pay—it's an inability to pay it all at once. Tax agencies get this, which is why they offer structured plans to help you get back on track.

-

Installment Agreement: Think of this as a payment plan for your tax debt. You agree to pay a set amount each month over a specific period until the balance is cleared. As long as you make your payments on time, the state will halt more aggressive collection actions, like seizing your bank account. It’s a great option for those with steady income who just need more time.

-

Offer in Compromise (OIC): An OIC is a more drastic solution where you ask the state to accept less than the full amount you owe. This isn't a simple negotiation; it’s a formal process reserved for those facing true financial hardship. You essentially have to prove that the state will get more money by settling with you now than they ever could by trying to collect the full debt over time.

A successful Offer in Compromise can be a game-changer, but be prepared to open up your finances completely. The state will want to see everything—bank statements, expenses, asset valuations—to be convinced that your offer is fair and reflects your true ability to pay.

Managing the Lien on Specific Property

Sometimes the lien itself isn't the main issue, but its impact on a specific piece of property is. If you're trying to sell your home or refinance your mortgage, the lien can be a major roadblock. Here’s how to navigate it.

Lien Discharge

A lien discharge is a surgical tool. It removes the state’s claim from one specific asset (like your house) without erasing the underlying tax debt. This is incredibly useful if you need to sell the property. The state will typically agree to a discharge if you promise to use the proceeds from the sale to pay down a significant portion of what you owe.

Lien Subordination

Lien subordination is all about changing the pecking order. It doesn't remove the lien, but it lets another creditor—usually a mortgage lender—jump ahead of the state in line to get paid. Why does this matter? Because no bank will give you a new loan or let you refinance unless their loan is in first position. Subordination makes that possible, clearing the path to better financing terms.

Once your debt is finally paid off, whether through a lump sum, payment plan, or OIC, the final step is to secure a Lien Release. This is the official document, filed in public records, that confirms the state's claim is gone. It’s the key to clearing your title, repairing your credit, and finally putting the issue behind you for good.

Your Questions About State Tax Liens, Answered

When you're dealing with a potential state tax lien, you need clear, straightforward answers. Let's tackle some of the most common questions we hear from property owners, business leaders, and investors.

How Can I Find Out if a Property Has a Tax Lien?

You can start by checking public records yourself. This usually means digging through the website of the County Clerk or Recorder's office where the property is located. Some states have also created a central, searchable database which can make things a bit easier.

But if you want a definitive answer, nothing beats a professional title search. A title company does this for a living; they're experts at uncovering any recorded liens, judgments, or other claims that could cause serious headaches down the road. It's an essential step in any real estate transaction.

How Long Will a State Tax Lien Stick Around?

This really comes down to state law, but a common timeframe is 10 to 20 years. That's the statute of limitations for the state to collect the debt. The key thing to remember, though, is that states can often refile or extend the lien, effectively resetting the clock and keeping the pressure on.

Paying off the debt is only half the battle. A lien doesn't just vanish once the check clears. You have to make sure the state files a formal "lien release" and that it's properly recorded. If that step is missed, the lien can still show up on your property title and credit report, so always follow up to confirm it’s gone for good.

Can a Tax Lien Actually Hurt My Business?

Without a doubt. A state tax lien doesn't just attach to real estate; it can encumber all your business assets. We're talking about everything from your primary bank accounts and accounts receivable to your mission-critical equipment.

This can make it incredibly difficult to get a business loan, bring on new investors, or even sell the company. In more aggressive cases, the state can levy your bank accounts—meaning they can legally seize the funds right out of them—or even padlock your doors and sell off your assets. The best strategy is always proactive compliance to prevent things from ever getting to that point.

Dealing with state tax liens demands both specific knowledge and a clear plan of action. If you need expert guidance on resolving complex tax issues and protecting your hard-earned assets, contact Blue Sage Tax & Accounting Inc. We specialize in bringing clarity to challenging financial situations. Find out more about how we can help at https://bluesage.tax.