If you’re a successful entrepreneur, real estate investor, or business owner in New York City, you don’t have a traditional 401(k). That's not a setback—it's an opportunity to take control and build wealth on your own terms. The main retirement plans for the self-employed—the Solo 401(k), SEP IRA, SIMPLE IRA, and Defined Benefit Plan—are incredibly powerful tools for slashing your tax bill and securing your financial future.

Choosing Your Path to Financial Independence

For entrepreneurs in a high-cost, high-tax environment like NYC, retirement planning isn't just about building a safety net. It's a core part of your overall wealth strategy. Standard IRAs just don't cut it; their contribution limits are too low for high earners. This is where specialized retirement plans for the self-employed come in. They provide a much more powerful way to grow your nest egg and handle a significant tax burden.

These plans are built for the reality of self-employment, where income can fluctuate and savings goals are often aggressive. Unlike a typical employee, you're not stuck with a plan chosen by an HR department. You have the freedom to pick a vehicle that aligns perfectly with your business’s cash flow, your tax picture, and your ultimate financial goals. This level of control is a massive advantage.

Why Proactive Planning Matters

High-net-worth individuals in competitive markets like New York City face a unique set of financial hurdles, from complex federal tax laws to punishing state and local taxes. The right retirement plan does more than just sock money away for later; it actively cuts down your taxable income right now.

Here’s why this is so critical:

- Massive Contribution Limits: The biggest draw is the ability to save far more than you could in a standard IRA. Plans like the Solo 401(k) and SEP IRA allow you to contribute well over $69,000 per year.

- Serious Tax Reduction: Every pre-tax dollar you contribute is a dollar you can deduct from your business's taxable income. The immediate tax savings can be substantial.

- The Right Fit for Your Business: Each plan is designed for a different scenario. A Solo 401(k) is perfect for a one-person shop, while a SIMPLE IRA makes sense for a small business with a handful of employees.

The real goal here is to think beyond simple savings. These plans are active financial instruments. They are specifically designed to reward your hard work by letting you keep more of what you earn, putting that money to work for your future instead of Uncle Sam's.

This guide will lay out a clear, side-by-side comparison to help you choose the right plan for your unique situation. Getting into the details and understanding the subtle differences between these options is the first step toward building the secure, prosperous retirement you deserve. Let's dive in and compare the top choices.

Comparing Your Top Self-Employed Retirement Plan Options

Choosing the right retirement plan is one of the most powerful financial moves a self-employed professional can make. When you're the one in charge, you have access to a unique set of tools designed to help you build wealth and slash your tax bill. But with several self-employed retirement plan options available, the key is to find the one that fits your income, business structure, and long-term goals like a glove.

This isn't about just listing features. We're going to dig into a practical, side-by-side comparison of the four workhorses of self-employed retirement savings: the SEP IRA, the Solo 401(k), the SIMPLE IRA, and the Defined Benefit Plan. Let's break down how they actually work for high-earning entrepreneurs and business owners.

Eligibility and Business Structure

Before you get lost in contribution limits, the first question to answer is: "Do I have employees?" This one factor is a major fork in the road and can immediately narrow your choices.

-

Solo 401(k): This plan is built exclusively for the self-employed with no employees, other than a spouse. The moment you hire a full-time W-2 employee, you're out. It's truly a "one-participant" powerhouse.

-

SEP IRA: Much more flexible. A SEP IRA is a great fit for a solo operator but also works well for a small business with a handful of employees. Its simplicity and high limits make it a very popular starting point.

-

SIMPLE IRA: As the name implies, this is designed for small businesses that want to offer a retirement benefit. If you have up to 100 employees, a SIMPLE IRA is an excellent way to provide a company plan without the complexity of a traditional 401(k).

-

Defined Benefit Plan: While almost any business can open one, these plans are really geared toward established, high-income sole proprietors or partners. They're a way to play catch-up and save an enormous amount of money in a short period, typically later in a career.

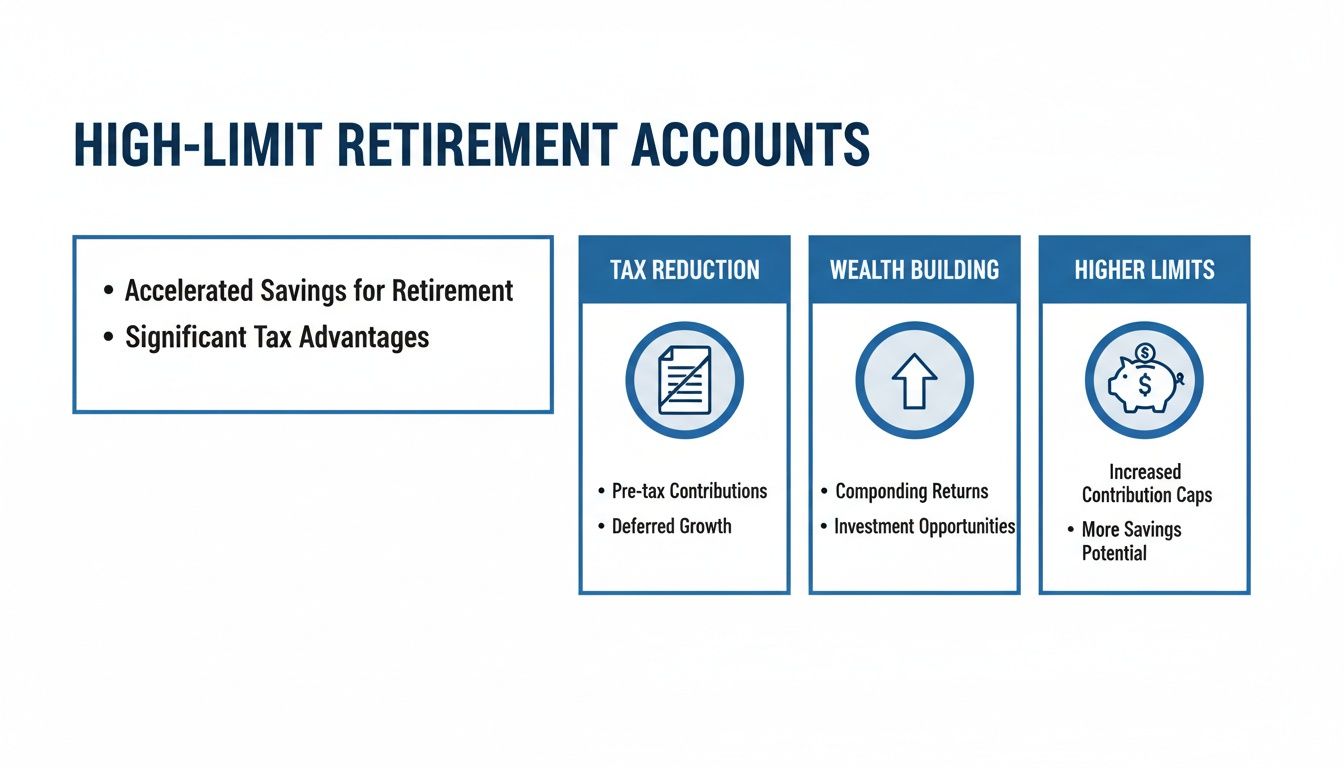

This infographic captures the core benefits you unlock with these powerful retirement accounts.

As you can see, the strategy boils down to immediate tax relief, disciplined wealth accumulation, and the ability to save far more than you could with a standard IRA.

Contribution Limits and Formulas

The real magic of these plans is how much you can sock away each year. The "how," however, differs quite a bit, and understanding the mechanics is crucial to maximizing your savings. The Solo 401(k), in particular, has a unique structure that lets you contribute from two different angles.

Think of yourself as wearing two hats with a Solo 401(k): you're both the "employee" and the "employer." This dual role means you can make two distinct contributions to the same plan, effectively supercharging what you can save.

Here’s a breakdown of how the contributions work for each plan:

-

SEP IRA: All contributions are made by the employer (that's you). You can put in up to 25% of your net adjusted self-employment income, with a cap of $69,000 for 2024. It's a simple, straightforward formula.

-

Solo 401(k): This is where you get to wear both hats. As the "employee," you can contribute 100% of your compensation up to $23,000 in 2024. Then, as the "employer," you can add an additional 25% of your net adjusted self-employment income. The grand total from both sources can't exceed $69,000 for 2024.

-

SIMPLE IRA: This plan requires participation from both sides. As the employee, you can contribute up to $16,000 in 2024. The employer side is then required to either match employee contributions up to 3% of their compensation or make a flat 2% contribution for all eligible employees.

-

Defined Benefit Plan: This is a completely different animal. Instead of a contribution limit, it has a benefit limit. An actuary calculates the annual funding needed to provide a predetermined, pension-like payout at retirement. Contributions can easily top $100,000 or even $200,000 a year, depending on your age and income.

Tax Advantages and Roth Options

All four of these plans let you make tax-deductible contributions, which is the main draw for many business owners looking to lower their current tax bill. But a key dividing line is whether you can make Roth (after-tax) contributions.

With a Roth contribution, you give up the immediate tax break. In exchange, your qualified withdrawals in retirement are 100% tax-free. If you believe you'll be in a higher tax bracket down the road, this is an incredibly valuable feature.

- The Solo 401(k) is the only one of these mainstream plans that routinely includes a Roth component. This lets you make your "employee" contributions with after-tax dollars.

- The standard SEP IRA and SIMPLE IRA do not have a built-in Roth option. While some recent legislation has opened the door for Roth versions, they are not yet common or widely supported by financial institutions.

The ability to choose Roth contributions inside a Solo 401(k) gives you tremendous tax diversification and control over your financial future.

Comparing Self-Employed Retirement Plans at a Glance

To bring it all together, let’s look at a high-level comparison. This table puts the key features of the most common self-employed retirement plan options side-by-side, helping you see the trade-offs at a glance.

| Feature | SEP IRA | Solo 401(k) | SIMPLE IRA | Defined Benefit Plan |

|---|---|---|---|---|

| Ideal For | High-income solo operators or businesses with few employees seeking simplicity. | Sole proprietors (and spouses) looking to maximize contributions and access Roth/loan options. | Small businesses (up to 100 employees) wanting an easy-to-manage retirement benefit. | High-income owners, often 50+, looking to make massive, tax-deductible contributions. |

| Who Contributes | Employer only. | Both employee and employer. | Both employee and employer (employer part is mandatory). | Employer only. |

| Max Contribution (2024) | $69,000 (up to 25% of compensation). | $69,000 (combined employee/employer). | $16,000 (employee) + employer match. | Varies by age/income; can exceed $100,000. |

| Roth Option? | No | Yes (for employee part) | No | No |

| Plan Loans? | No | Yes (up to $50,000) | No | No |

| Admin Burden | Very Low | Moderate (Form 5500-EZ if assets >$250k) | Moderate (requires notices to employees) | High (requires an actuary) |

This table makes the strategic differences clear. The SEP IRA is your go-to for high limits and pure simplicity. The Solo 401(k) offers the most features and flexibility for an individual, including the coveted Roth option and plan loans. The SIMPLE IRA serves a different audience—the small business owner looking to care for a team.

And in its own league, the Defined Benefit Plan is the ultimate tool for those who need to save aggressively later in their careers, though it comes with far more complexity and cost.

A Deep Dive on the Solo 401(k) for High Earners

When I talk to high-income sole proprietors, independent contractors, or consultants without employees, the Solo 401(k) is almost always at the top of the list. It’s hands-down one of the most powerful tools in the retirement savings arsenal for the self-employed. Sometimes called a one-participant 401(k), this plan offers a unique mix of high contribution limits, flexible options, and features you just won’t find in other common self employed retirement plan options. It’s built for business owners who want to save aggressively and keep a firm grip on their financial strategy.

What really makes the Solo 401(k) a standout is its dual-contribution structure. Since you're self-employed, the IRS sees you as both the "employee" and the "employer" of your business. This clever distinction allows you to make two separate contributions to your plan each year, which can dramatically boost your savings potential far beyond a standard IRA.

Unpacking the Dual-Contribution Advantage

The ability to contribute in two capacities is the engine behind the Solo 401(k)'s power. Getting a handle on how this works is the key to getting the most out of it.

-

As the 'Employee': You can contribute up to 100% of your compensation through salary deferrals, with a cap of $23,000 for 2024. If you're age 50 or over, you can tack on an extra catch-up contribution.

-

As the 'Employer': On top of your employee contribution, your business can kick in a profit-sharing contribution of up to 25% of your net adjusted self-employment income.

The combined total from both sources can't go over the annual limit, which is a hefty $69,000 for 2024. This structure lets you stash away a huge chunk of your income in a tax-advantaged account, leaving traditional and Roth IRAs in the dust.

The Strategic Value of the Roth Solo 401(k)

One of the most compelling features—and a critical differentiator from SEP and SIMPLE IRAs—is the option to designate your employee contributions as Roth. This is a game-changer.

When you make Roth contributions, you give up the immediate tax deduction. The payoff? All qualified withdrawals of your contributions and their earnings are 100% tax-free in retirement.

Why is this so important for a high earner? If you expect to be in the same or even a higher tax bracket when you retire—a very real possibility for successful entrepreneurs—the Roth Solo 401(k) can save you an absolute fortune in future taxes. It provides critical tax diversification for your entire retirement portfolio.

This flexibility lets you pick your tax advantage:

- Traditional Contributions: Get your tax break now by lowering your current taxable income.

- Roth Contributions: Pay the taxes now to enjoy tax-free income later.

Many savvy business owners I work with split the difference. They make Roth employee contributions for future tax-free growth and still get the immediate tax deduction on their employer's profit-sharing contribution. It's a fantastic way to create a balanced tax strategy.

Accessing Liquidity Through Plan Loans

Here's another exclusive feature that puts the Solo 401(k) in a class of its own: the ability to borrow from your account. You can't do this with a SEP IRA or a SIMPLE IRA. This provision can be a financial lifeline, giving you access to capital without getting hit with taxes or early withdrawal penalties.

The rules are pretty straightforward. You can borrow up to 50% of your account balance, capped at a maximum of $50,000. The loan has to be paid back with interest, usually over five years. Whether you need emergency funds or a bridge loan for a business opportunity, this feature adds a layer of financial flexibility that other plans just don't offer. For business owners with unpredictable cash flow, this access to liquidity is a huge practical advantage.

When a SEP IRA or SIMPLE IRA Makes More Sense

The Solo 401(k) gets a lot of attention, and for good reason—it’s a powerhouse for many self-employed individuals. But it’s not a one-size-fits-all solution. Depending on your business structure, income level, and whether you have employees, one of the other self employed retirement plan options might be a much better fit.

Let’s look at the SEP IRA and the SIMPLE IRA. These aren’t just "alternatives"; they are strategic tools designed for specific situations. Knowing when to opt for one of these plans over a Solo 401(k) is crucial for optimizing your retirement savings and managing your business effectively.

The Case for the SEP IRA

Think of the Simplified Employee Pension (SEP) IRA as the go-to for high-income solo operators who value simplicity above all else. It strips away administrative busywork while still letting you sock away a significant amount of money, all tax-deductible.

A SEP IRA really hits its stride in a few key scenarios:

- You demand maximum simplicity. Setting up and managing a SEP IRA is about as easy as it gets, often just a single form to start. Unlike a Solo 401(k), which can trigger a Form 5500-EZ filing once assets top $250,000, the SEP IRA has no annual filing requirements for you as the business owner.

- Your income is high and relatively predictable. Contributions are made solely by the "employer" (that's you), calculated as a straight percentage of your compensation up to 25%. This makes it perfect for professionals with consistent, high earnings who prefer to make one large contribution annually.

- You've missed the Solo 401(k) setup deadline. This is a big one. A Solo 401(k) has to be established by December 31st of the tax year. A SEP IRA, on the other hand, can be opened and funded right up until your business's tax filing deadline, extensions included. It’s a fantastic last-minute tool for slashing your tax bill.

The SEP IRA's superpower is its straightforward, high-impact design. It lets you contribute just as much as a Solo 401(k)—up to $69,000 for 2024—without juggling employee/employer contribution rules or worrying about annual IRS reporting. For a busy consultant or freelancer focused purely on maximizing tax-deferred savings, it's often the most efficient route.

For instance, a consultant with $300,000 in net business income can put away the full $69,000 into their SEP IRA. The calculation is clean, the paperwork is minimal, and the tax deduction is massive. The catch? If this consultant hires an employee, they're on the hook for contributing the exact same percentage of compensation for that employee, which can get expensive quickly.

The Role of the SIMPLE IRA

The SIMPLE (Savings Incentive Match Plan for Employees) IRA is built for an entirely different stage of business. This is the plan you turn to when your one-person show grows into a small team and you want to offer a retirement benefit. It's an accessible first step into the world of employer-sponsored plans.

A SIMPLE IRA is the clear choice when:

- You have employees. The moment you hire full-time W-2 staff, the "Solo" 401(k) is off the table. The SIMPLE IRA is specifically designed for businesses with up to 100 employees.

- You need to attract and keep good people. In today's market, a retirement plan is a powerful tool for retention. A SIMPLE IRA lets you offer this competitive perk without the cost and complexity of a traditional 401(k).

- You want to save right alongside your team. The plan requires you to make contributions for your employees. You have two options: either a dollar-for-dollar match of up to 3% of their salary or a flat 2% contribution for everyone, regardless of whether they contribute themselves.

This structure makes the SIMPLE IRA incredibly practical for a growing small business. You're investing in your team’s financial future, which builds loyalty, all while continuing to fund your own retirement. The contribution limits are lower ($16,000 in 2024 for the employee part, plus the employer match), but it strikes the right balance between your personal savings goals and your responsibilities as a business owner.

A Deeper Dive: The Power of Defined Benefit Plans

For well-established business owners with years of high, stable income, the usual self employed retirement plan options can start to feel restrictive. If you're looking to put away a serious amount of money in a relatively short period, the Defined Benefit Plan is in a class by itself. Think of it as the heavyweight champion of aggressive, tax-deductible retirement saving.

Most retirement plans focus on how much you can contribute today. A Defined Benefit Plan flips that script entirely. It starts by defining a specific, pension-like income stream you want in retirement. From there, an actuary works backward to calculate the enormous annual contributions required to make that future promise a reality.

The result? Contribution levels that can easily blow past $100,000 a year, and for some, even approach or exceed $200,000. For a high-earning business owner, this is an incredible way to slash your current tax bill while supercharging your nest egg.

Pinpointing the Right Fit

A Defined Benefit Plan is a finely tuned instrument, not a one-size-fits-all solution. It’s built for a very specific type of business owner who checks a few key boxes.

This plan is typically a perfect match for someone who is:

- Over 50 years old: With a shorter runway to retirement, the required annual funding amounts are larger, which in turn creates a much larger tax deduction.

- Running a consistently profitable business: These plans aren't a casual commitment. They demand significant, predictable funding year in and year out, so strong and stable cash flow is a must.

- A high-income earner: The real magic happens when you're in a top tax bracket, where a six-figure deduction can lead to massive tax savings.

- Operating with few or no employees: While you can include employees, the funding obligations can quickly become prohibitively expensive. These plans work best for sole proprietors, consultants, or partnerships with just the owners.

Think of a Defined Benefit Plan as your own personal pension. You shift the question from "How much can I put in?" to "How much do I want to take out later?"—and then make the massive, tax-deductible contributions to guarantee that outcome.

The Critical Role of an Actuary

Given their complexity, you can’t just set up a Defined Benefit Plan on your own. This is where an actuary—a certified professional who deals in financial risk and projections—becomes an essential part of your team.

Your actuary handles several critical tasks:

- Calculating Annual Contributions: They run the numbers based on your age, income, and retirement goals to determine the exact amount you must contribute each year.

- Managing IRS Filings: These plans come with serious reporting requirements, like the annual Form 5500, which the actuary prepares on your behalf.

- Ensuring Ongoing Compliance: The actuary keeps the plan in line with all the intricate government rules, adjusting calculations as investment performance and regulations change.

Yes, the administrative and actuarial fees are considerably higher than those for a SEP IRA or Solo 401(k). But for the right person, the math works out beautifully. If you're able to put away $150,000 a year, the resulting tax savings will likely far outweigh the costs, making it a brilliant investment in your future. No other retirement plan for the self-employed comes close to this level of savings potential.

Making the Right Choice: A Practical Framework

Alright, you've seen the options. Now comes the hard part: picking the right one. How do you move from comparing features on a screen to making a decision that feels right for your business and your future? The key is to look inward at your specific situation.

There’s no single “best” plan—only the best plan for you. The right choice hinges on a handful of critical questions about your income, your team, and your long-term goals. Let's walk through them.

Key Questions to Guide Your Decision

Think of these questions as a filter. Your answers will quickly narrow down the possibilities and point you toward the most logical fit.

- What’s your income situation? If you have high, stable earnings, you'll want to look at plans that let you sock away the most money. That puts the SEP IRA, Solo 401(k), and even a Defined Benefit Plan at the top of the list.

- Are you planning to hire employees? This is a deal-breaker for one popular option. The moment you bring on staff (other than your spouse), the Solo 401(k) is out. A SIMPLE IRA is built for small teams, while a SEP IRA can work but might get expensive fast.

- How much do you actually want to save? Be realistic. If you're aiming to save the absolute maximum allowed by law, the dual-contribution nature of a Solo 401(k) or the high ceiling of a SEP IRA is what you need. If your savings goals are more moderate, a SIMPLE IRA is often more than enough.

- Do you want a Roth option or the ability to take a loan? For some business owners, having a loan feature for emergencies or the option for tax-free growth with a Roth is non-negotiable. If that’s you, the Solo 401(k) is the only plan that offers both.

A lot of self-employed people skip this part—they save, but they don't strategize. Simply writing down your goals and the reasoning behind your choice can make a world of difference.

Research on workforce retirement trends reveals a fascinating gap. While an impressive 60% of self-employed individuals are saving for retirement (starting at a median age of 29), and 75% of them use tax-advantaged accounts, only 22% have a formal, written financial plan. That's a huge disconnect between action and strategy.

Putting the Framework into Practice: Real-World Scenarios

Let's see how this plays out for a couple of typical NYC professionals.

- The Tech Consultant (High Income, No Employees): She’s pulling in $250,000 a year and wants to save aggressively, but also wants the flexibility of Roth contributions for tax diversification down the road. For her, the Solo 401(k) is the slam-dunk choice. It lets her max out her savings and gives her that Roth option.

- The Real Estate Developer (Growing Team): He’s got three employees and wants to offer a retirement plan to keep them around. A SIMPLE IRA is the perfect solution here. It’s straightforward to set up and allows both him and his team to contribute, making it a great retention tool.

This framework isn't about giving you a definitive answer, but about empowering you to have a much more productive conversation with your financial advisor. You’ll be able to walk in, explain your situation clearly, and work together to lock in the best possible strategy.

Common Questions Answered

When you're sorting through retirement plans for your business, a few key questions always seem to pop up. Let's tackle some of the most frequent ones I hear from entrepreneurs.

Can I Have More Than One Retirement Plan?

Absolutely. It's actually quite common. For example, if you have a day job with a 401(k) and also run a side business, you can set up a SEP IRA or a Solo 401(k) for your self-employment income.

The main thing to watch out for is how the contribution limits interact. The rules can get tricky, and sometimes your contributions to one plan can affect how much you can put into another, so it's not a free-for-all.

What Are the Deadlines for Setting Up and Funding a Plan?

This is where timing can make or break your tax strategy for the year.

For a SEP IRA, you have a lot of flexibility. You can open and fund the plan right up until your business tax filing deadline, including any extensions you might file for.

A Solo 401(k) is a different story. You must have the plan officially established by December 31st of the tax year. The good news is you still have until your tax deadline (plus extensions) to actually make the employer contributions.

A classic mistake is waiting until January or February to think about setting up a Solo 401(k) for the prior year. If you miss that December 31st setup deadline, you've missed your chance. This is when the SEP IRA becomes an excellent plan B.

What Happens to My Solo 401(k) if I Hire Someone?

The "Solo" in Solo 401(k) is there for a reason—it’s strictly for the business owner and their spouse. The moment you bring on a full-time W-2 employee (who isn’t your spouse), your plan is no longer compliant.

At that point, you'll need to freeze the Solo 401(k), meaning you can't make any new contributions. Your next step would be to either roll the existing assets into an IRA or establish a new plan that can cover employees, like a SIMPLE IRA.

Getting these details right is crucial for building wealth and minimizing your tax burden. At Blue Sage Tax & Accounting Inc., we specialize in proactive tax and retirement strategies for successful business owners and high-net-worth individuals in NYC. Let us help you build a plan that truly fits your financial picture. Learn more about our approach at https://bluesage.tax.