When you hear about Qualified Opportunity Zones (QOZs), you're really hearing about three powerful tax incentives wrapped into one strategy. It's a way to defer your current capital gains tax, get a reduction on that deferred tax bill, and then, most importantly, completely eliminate any future capital gains tax on the new investment.

This program was created as part of the 2017 Tax Cuts and Jobs Act. It was designed to encourage investors to take their profits from selling stocks, real estate, or a business and put that money to work in designated communities that need it most. It's a win-win: you get a significant tax break, and capital flows into developing areas.

Understanding the QOZ Program and Its Core Value

At its core, the Qualified Opportunity Zone program is a trade. You agree to invest your recent capital gains into a Qualified Opportunity Fund (QOF) that targets these specific zones, and in return, the government gives you a series of compounding tax benefits. For investors in a high-tax environment like New York City, this can be a game-changer for managing the tax bite from a major liquidity event.

Think of it this way: instead of immediately writing a check to the IRS after a big gain, you have a 180-day window to reinvest that gain into a QOF. Doing this hits the pause button on your tax bill and puts that money into an investment designed for long-term, tax-free growth.

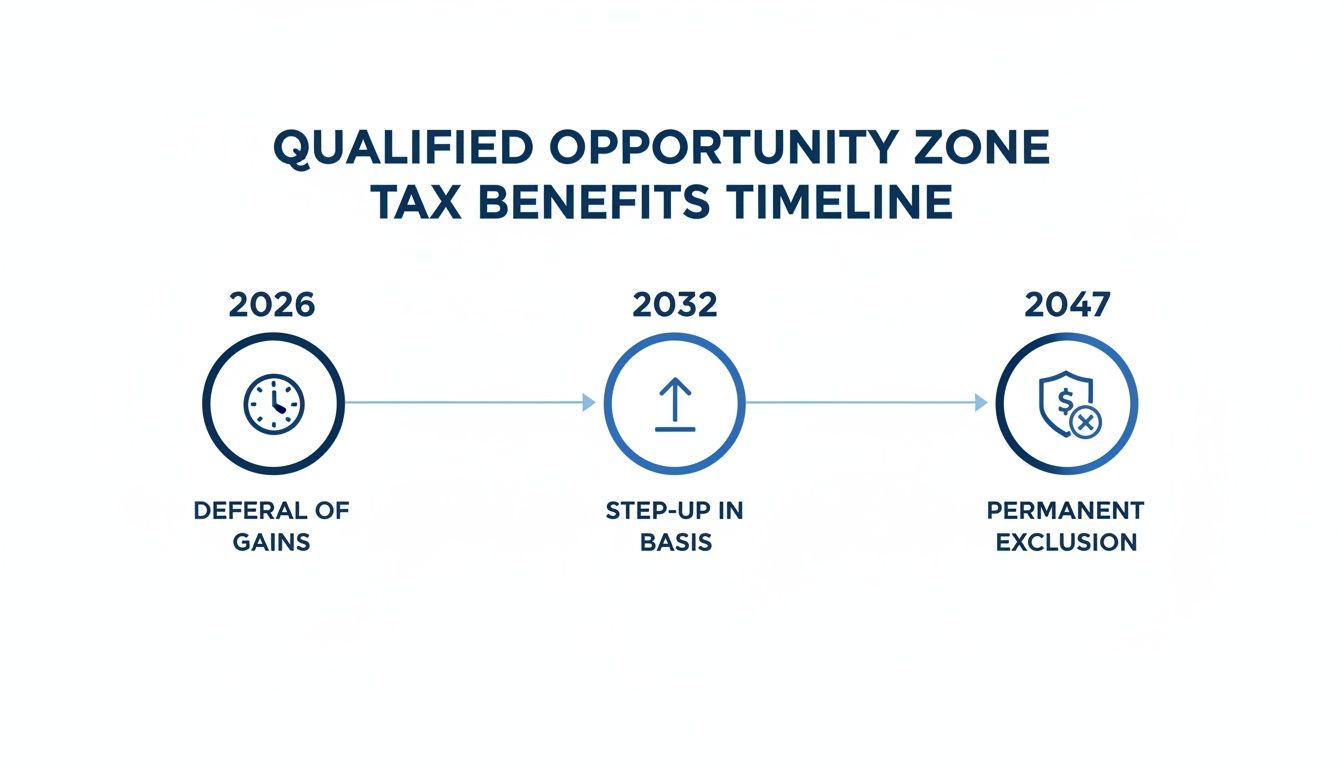

To really see how this works, you need to understand the three main benefits and how they're tied to your holding period. The longer you stay in the investment, the more powerful the tax savings become, with the ultimate prize being a complete tax exemption for those who stick with it for the long haul.

The real power of the QOZ program isn't just deferring a tax bill; it's about transforming a tax liability into a tax-free growth engine. It allows savvy investors to compound their capital more efficiently while making a tangible impact.

Let's break down these three core incentives in a simple table. This really helps visualize how the benefits stack up over time, moving you from simply delaying your tax payment to completely eliminating taxes on your new profits. This is what makes the QOZ program one of the most compelling tax strategies available today.

The Three Core Qualified Opportunity Zone Tax Benefits

| Investment Holding Period | Tax Benefit Unlocked | Impact on Your Capital Gains |

|---|---|---|

| Initial Investment | Tax Deferral | Postpones the tax payment on your original capital gain until as late as December 31, 2026. |

| 5+ Years | Basis Step-Up | Reduces the taxable amount of your original deferred gain, providing a permanent tax reduction. |

| 10+ Years | Permanent Gain Exclusion | Eliminates 100% of the federal capital gains tax on any new appreciation from your QOF investment. |

As you can see, the program rewards patience. The ten-year hold is where the magic really happens, offering a rare opportunity for truly tax-free appreciation on your new investment.

The Three Pillars of QOZ Tax Savings

The Qualified Opportunity Zone program is built on three powerful tax incentives that stack on top of each other over time. To really get a feel for how impactful this strategy can be, you have to look at how these pillars work together. It’s not just one benefit; it’s a compounding advantage that rewards patient, long-term investors.

At its heart, the program lets you take the gains from a recent sale—whether from stocks, real estate, or your business—and put that capital back to work with some serious tax advantages. This is a game-changer for anyone who’s had a big liquidity event and is looking for a smart, efficient way to preserve and grow that capital.

Let's unpack these three pillars—deferral, basis step-up, and permanent exclusion—and see how they actually play out.

Pillar 1: Deferral — The Power of Postponement

The first and most immediate benefit you get from a QOZ investment is tax deferral. Instead of cutting a check to the IRS for capital gains in the year you make a sale, you can effectively hit the pause button on that tax bill. This isn't just kicking the can down the road; it’s a strategic move that keeps your capital working for you.

Let’s say you sell an asset and have a $1 million capital gain. Normally, that triggers a tax liability, due now. But by reinvesting that $1 million gain into a Qualified Opportunity Fund (QOF) within the 180-day window, you push that tax bill all the way out to December 31, 2026.

This simple act of deferral gives you two huge advantages right out of the gate:

- More Capital at Work: You get to invest the full, pre-tax $1 million. That’s a larger base of capital compounding and growing from day one.

- Time Value of Money: The money you would have paid in taxes stays in your pocket, working for you for years. It’s like getting an interest-free loan from the government.

This first benefit is the gateway to the even bigger incentives that come later. It sets the stage for what’s to come.

The timeline below gives you a great visual of how these benefits build on each other over the life of the investment.

As you can see, the program is deliberately structured to reward investors who are in it for the long haul, helping to fuel real economic growth in these communities.

Pillar 2: Basis Step-Up — A Permanent Tax Reduction

The second benefit was designed to give you a permanent discount on the tax you’d eventually owe on that original, deferred gain. This was done through a step-up in basis. Unfortunately, the deadlines for new investments to qualify for these step-ups have passed.

Still, it’s important to understand how it worked. For early investors who held their QOF investment for at least five years before the 2026 deadline, the program offered a 10% increase in the basis of their original investment, effectively making 10% of that gain tax-free forever.

While new investors can no longer get this basis step-up, understanding its role is key. It shows the program's original intent: to layer on rewards for sustained, long-term commitment to these designated zones.

This powerful deferral mechanism, created by the 2017 Tax Cuts and Jobs Act, has been a go-to strategy for high-net-worth individuals and developers. Remember, once you realize a capital gain, you have 180 days to roll it into a QOF, pushing the tax bill to the end of 2026 and giving your money a strategic window to grow. For more details on the mechanics, you can explore further analysis on the topic.

Pillar 3: Permanent Exclusion — The Grand Prize

This is the big one. The third and, by far, the most compelling benefit of the QOZ program is the permanent exclusion of capital gains on the new QOF investment itself. For investors with a long-term horizon, this is the ultimate prize.

Here’s the deal: if you hold your investment in the QOF for at least 10 years, every single dollar of appreciation your investment earns is 100% free from federal capital gains tax. Let me say that again—completely tax-free. It’s one of the most powerful wealth-building tools baked into the U.S. tax code.

Let's go back to our example one last time:

- You invest your $1 million deferred gain into a QOF.

- You hold it for 10 years.

- Over that decade, your investment grows to $2.5 million.

When you sell that QOF investment after the 10-year mark, the $1.5 million of new growth ($2.5M sale price – $1M initial investment) is yours to keep, completely free from federal capital gains tax. This transforms the QOF from a simple deferral strategy into an incredible engine for tax-free wealth creation.

How to Invest in a Qualified Opportunity Fund

Knowing the powerful tax benefits of the Qualified Opportunity Zone program is one thing, but putting that knowledge into action is what truly matters. The investment process itself is methodical, demanding close attention to timing and detail. It all starts with a capital gain.

Just about any gain from selling an asset to an unrelated party can be your ticket into the QOZ program. This could be from selling stocks, a piece of real estate, your family business, or even a valuable piece of art. The moment you realize that gain, a critical countdown begins.

Navigating the 180-Day Investment Window

From the date you receive the proceeds from your sale, you have a 180-day window to reinvest the gain portion into a Qualified Opportunity Fund (QOF). This deadline is non-negotiable. Missing it means you lose the chance to defer the tax and tap into any of the program's powerful benefits.

Thankfully, the rules provide some welcome flexibility for gains flowing from a partnership or an S-corporation. In these cases, the 180-day clock can start on the date of the entity's sale, the last day of its tax year, or even the due date of its tax return. This gives partners and shareholders much more breathing room to plan their QOF investment.

The engine of this entire process is the Qualified Opportunity Fund, the specific investment vehicle that directs capital into designated zones. A QOF is simply a corporation or partnership set up for the express purpose of investing in QOZ property.

A QOF must hold at least 90% of its assets in qualified opportunity zone property. This is the rule that ensures the capital is actually put to work fueling development and economic activity in the target communities—the entire point of the legislation.

Choosing Your QOF Investment Path

Investors typically have two main avenues for getting involved, each offering a different degree of control and responsibility.

- Investing in an Existing QOF: This is the most common route. You invest in a fund managed by a third-party sponsor, much like a traditional private equity or real estate fund. These managers often specialize in certain sectors, like multifamily real estate or early-stage tech companies, and handle all the operational heavy lifting.

- Creating a Self-Directed QOF: For entrepreneurs or family offices who already have a specific project in mind, forming your own QOF delivers total control. This path means you establish a new partnership or corporation and take on the responsibility of ensuring it meets all IRS compliance standards, including the crucial 90% asset test.

Which path is right depends entirely on your specific goals, your hands-on expertise, and how involved you want to be.

Performing Diligence on QOFs

If you decide to invest in an existing fund, think of it like hiring a key business partner—thorough due diligence is non-negotiable. Not all QOFs are built the same, and the ultimate success of your investment hinges on both the manager’s skill and the fund’s strict adherence to the program rules.

When you're kicking the tires on a QOF, focus on these critical areas:

- Manager Experience: Does the fund sponsor have a legitimate, proven track record in the specific assets they're targeting? A manager with deep experience in NYC commercial real estate, for example, is a very different beast than one focused on tech startups.

- Fund Strategy: Get crystal clear on the investment thesis. Does it align with your personal risk tolerance and financial objectives? You need to understand the specific projects or businesses the fund intends to back.

- Compliance and Reporting: A top-tier QOF will have a rock-solid framework for navigating the complex QOZ regulations. Don't be shy about asking about their legal and accounting teams.

- Fee Structure: Dig into the fine print. You need to analyze the management fees, carried interest (the manager's share of profits), and any other expenses. Remember, high fees can eat away at your long-term, tax-free returns.

For investors focused on the New York City market, finding a fund with deep local knowledge is a game-changer. A manager who truly understands the city’s unique zoning codes, development hurdles, and economic microclimates brings a massive advantage to the table. This vetting process is the final, crucial step in turning a capital gain into a powerful, tax-advantaged growth engine.

QOZ Investment Scenarios for NYC Investors

Tax benefits are one thing on paper, but seeing them work in the real world is what really matters. To get a feel for the true power of a Qualified Opportunity Zone investment, let's walk through three scenarios that are common for investors here in New York City. Each example will put real numbers and timelines to the concepts of deferral and permanent gain exclusion.

These stories show how different types of capital gains—from selling a building, exiting a business, or rebalancing a stock portfolio—can be strategically rolled into a QOF to build significant, long-term tax-free wealth.

Scenario 1: The Brooklyn Real Estate Investor

Meet Sarah. She bought a multi-family building in Park Slope years ago and, after watching its value climb, decides to sell in May 2024. The sale leaves her with a $2 million capital gain and a looming federal tax bill. Instead of just writing a check to the IRS, she starts looking into the QOZ program.

She finds a promising Qualified Opportunity Fund that’s backing a new mixed-use project in a designated Opportunity Zone in Long Island City. Well within her 180-day window, she reinvests the entire $2 million gain into this QOF.

Here’s how the benefits play out for her:

Immediate Tax Deferral: Right away, Sarah gets to defer the tax on her $2 million gain. She won’t owe federal capital gains tax on it for the 2024 tax year; that liability is kicked down the road to December 31, 2026. This is huge—it means her entire $2 million is working for her in the new project from day one.

The 10-Year Horizon: The Long Island City project turns out to be a great bet. The neighborhood booms, and after holding her investment for a little over a decade, Sarah sells her QOF stake in June 2034 for $5 million.

The Tax-Free Exit: This is the game-changer. Because she held the investment for more than 10 years, her new gain is completely tax-free. The $3 million in appreciation ($5 million sale price minus her $2 million initial investment) is entirely exempt from federal capital gains tax.

The math here is incredibly compelling. By rolling a $2 million gain into a QOF, Sarah first deferred the tax. Then, by letting that investment grow to $5 million over 10 years, the entire $3 million of new profit escapes federal tax altogether. At current long-term capital gains rates, that could easily save her over $714,000. You can find more details on how these calculations work by exploring government resources for investors.

Scenario 2: The Startup Founder’s Exit

Now, let's look at David, an entrepreneur who launched his tech startup from a Manhattan co-working space. In August 2024, the company gets acquired, and David walks away with a $5 million long-term capital gain.

Rather than putting it all into a traditional portfolio, David wants to reinvest in the local ecosystem. He decides to roll $3 million of his gain into a venture-focused QOF that seeds early-stage businesses operating in designated Opportunity Zones in the Bronx.

Let's track his journey:

- Gain Deferral: David defers the federal tax owed on the $3 million he reinvested. This immediately allows a much larger capital base to be put to work in the fund's portfolio of startups.

- Long-Term Growth: Over the next 11 years, the QOF’s portfolio companies grow. A few fail, as startups do, but a couple become breakout successes, driving the value of David's initial stake all the way up to $9 million.

- Permanent Gain Exclusion: When David liquidates his position in 2035, the $6 million of appreciation is completely free from federal capital gains tax. This strategy didn't just let him delay a big tax bill—it allowed him to generate millions in tax-free profit while helping fuel economic growth right in his own city.

Scenario 3: The Family Office Diversification Play

Finally, consider a family office managing a portfolio built over generations. After a strategic rebalancing in early 2024, the office realizes a $10 million capital gain from selling a highly concentrated stock position.

The family’s investment committee sees the QOZ program as a perfect tool for both diversification and impact. They decide to allocate $5 million of that gain into a diversified, multi-asset QOF that holds a mix of real estate and operating businesses across several NYC Opportunity Zones.

For a family office, a QOF investment serves a dual purpose. It's a powerful tool for tax-efficiently recycling capital gains while also fulfilling philanthropic or impact-investing mandates by directing funds toward community revitalization.

Here’s how this strategy delivers a compelling outcome:

- Tax Management: The tax on the $5 million gain is deferred, immediately improving the portfolio's overall tax efficiency for the next few years.

- A Decade of Growth: The family holds the QOF investment for the required 10 years. By 2034, steady appreciation across the fund’s diverse assets has grown their stake to $11 million.

- Tax-Free Appreciation: Upon exiting the fund, the entire $6 million of growth is shielded from federal capital gains taxes. This outcome dramatically enhances the family’s after-tax returns, delivering a result far beyond what a traditional, taxable investment could have achieved with the same pre-tax performance.

Navigating New York State and City Tax Rules

While the federal benefits of the Qualified Opportunity Zone program are compelling, investors in New York have a major local hurdle to clear. The powerful federal tax advantages simply don't carry over to your state and city tax returns. This is a critical point that, if overlooked, can lead to a significant and immediate tax bill you weren't expecting.

The reason? New York State and New York City have officially "decoupled" from the federal QOZ program. Put simply, this means they don’t recognize the tax deferral. So, even when you roll a capital gain into a Qualified Opportunity Fund and successfully pause your federal tax clock, NYS and NYC treat that gain as taxable income right away.

This creates a serious cash-flow problem you have to plan for. While your pre-tax federal dollars are hard at work in a QOF, you still need to have cash on hand to pay the state and city taxes on that exact same gain.

Understanding the Decoupling Effect

The impact of this decoupling is pretty direct. Let's go back to our earlier example: you generate a $2 million capital gain from selling a property in Brooklyn and reinvest it into a QOF.

- Federal Treatment: You've successfully deferred the federal capital gains tax, pushing it out to December 31, 2026.

- New York Treatment: You owe New York State and City income tax on that $2 million gain for the current tax year. It’s due now.

This immediate tax liability often catches investors by surprise. The last thing you want is to be blindsided by a hefty state and local tax bill right after you’ve locked up your capital in a long-term QOF investment.

The core takeaway for NYC investors is this: a QOZ investment splits your tax obligation. You defer the federal portion, but you must pay the state and city portion now. Factoring this immediate cash outflow into your investment analysis is non-negotiable.

Strategic SALT Planning Is Essential

This is precisely where sophisticated State and Local Tax (SALT) planning becomes absolutely critical. A solid strategy isn't just about cutting a check; it's about optimizing your entire financial position given this unique tax divergence. A seasoned advisor can help you model the exact cash impact and find the best ways to manage that liability.

For any NYC-based investor, the planning process must include these steps:

- Calculate the Immediate Liability: Before you even think about signing QOF documents, figure out the exact New York State and City tax you will owe on the gain. Treat this number as a key part of your investment's upfront cost.

- Secure Necessary Liquidity: Make sure you earmark enough cash from the sale proceeds to cover this tax payment. Never reinvest 100% of the gain without first setting aside funds for this tax bill.

- Analyze True After-Tax Returns: That state and city tax hit directly reduces the amount of capital you have left to invest. It's crucial to rerun your QOF projections to reflect your true, after-tax return so you can accurately compare it against other investment options.

For New York investors, a successful QOZ strategy requires a dual focus. You have to capture the powerful long-term federal benefits while carefully managing the immediate state and local tax consequences. Proper SALT planning is the bridge between these two realities, making sure your investment is both compliant and financially sound from day one.

IRS Compliance and Reporting Requirements

All the strategic planning in the world won't secure your QOZ tax benefits without meticulous IRS compliance. Think of this as the final, and frankly, non-negotiable step. Get it right, and your tax deferral and exclusion are locked in. Get it wrong, and you risk unraveling the whole strategy.

This isn't just about filling out a form or two. It's about creating a clear paper trail for the IRS that documents your initial deferral and tracks your investment year after year. This process starts the moment you make your QOF investment and continues for as long as you hold it.

Making the Initial Deferral Election

To officially hit the pause button on your original capital gain, you have to make a formal election on your tax return for the year the gain occurred. This is where Form 8949, Sales and Other Dispositions of Capital Assets, comes into play.

You'll report the gain just like you normally would, but with a critical difference: you'll use a special code to signal to the IRS that you’ve rolled that gain into a Qualified Opportunity Fund. This is you telling them, "I'm not paying tax on this gain yet because I’ve reinvested it under the QOZ program rules." This form is also where you'll list the Employer Identification Number (EIN) of the specific QOF you invested in.

At the same time, you'll file Form 8997, Initial and Annual Statement of Qualified Opportunity Fund Investments, for the very first time. This form officially registers your QOF investment with the IRS and becomes the cornerstone of your annual reporting obligations.

Annual Reporting Requirements

Your paperwork isn't a one-and-done deal. Every single year that you hold your QOF investment, you must continue to file Form 8997 with your tax return. There are no exceptions.

Think of Form 8997 as your annual compliance scorecard. It updates the IRS on your investment's status, flags any potential issues, and proves you're still on track to meet the 10-year holding period for permanent gain exclusion.

Missing this annual filing is a serious misstep. It can trigger penalties and send a red flag to the IRS that you might have fallen out of compliance, jeopardizing your tax benefits. It’s a simple requirement, but an absolutely critical one.

Your best defense is a strong offense, which means keeping impeccable records.

- Transaction Records: Save all documents from the sale that generated your original capital gain.

- QOF Investment Proof: Keep every subscription agreement, K-1, and statement from the fund.

- Tax Forms: Maintain organized copies of all submitted Forms 8949 and 8997.

When the day comes to sell your QOF interest after holding it for more than ten years, this consistent filing history will be the proof you need to claim that tax-free appreciation. Working with a tax professional who lives and breathes these rules, like the team at Blue Sage Tax & Accounting Inc., is the surest way to know every 'i' is dotted and every 't' is crossed correctly from day one.

Answering Your Top QOZ Questions

Once you get the basics down, the real questions start to pop up. It's one thing to understand the three main tax benefits, but it's another to apply them to your specific situation. Let's walk through some of the most common "what if" scenarios we hear from clients.

Think of this as the practical side of QOZ investing—the stuff you need to know before you write the check.

What If I Have to Sell Before the 10-Year Mark?

This is a big one. Life happens, and you might need to access your capital sooner than planned. Selling your Qualified Opportunity Fund (QOF) investment early won't erase the initial deferral, but it does change the tax math significantly.

Selling Before 5 Years: If you cash out this early, you face a double whammy. The sale immediately triggers your original, deferred capital gain, and you'll have to pay that tax bill. On top of that, any profit you made on the QOF investment itself is taxed as a normal capital gain.

Selling Between 5 and 10 Years: The outcome is pretty much the same here. You still have to pay tax on your original deferred gain, and the new appreciation on your QOF investment is also fully taxable. You miss out on the most powerful benefit of the entire program.

Simply put, the 10-year hold is the magic number. That's the only way to unlock the tax-free growth on your QOF investment. Selling early forfeits that incredible advantage.

Think of it like this: The 10-year hold is the key to the treasure chest. If you leave early, you get your original investment back (plus any gains, which are now taxable), but the real treasure—tax-free appreciation—stays locked away forever.

How Does Depreciation Work with QOF Assets?

For anyone investing in QOFs that hold real estate, this question is crucial. The good news is that depreciation works just like you'd expect. The QOF can take depreciation deductions on its properties, and those tax losses can often be passed through to you, the investor.

This can be a fantastic way to shelter other income while your QOF investment grows. However, keep in mind that depreciation reduces your property's tax basis. When the QOF eventually sells that property, there will be a larger taxable gain to account for, including depreciation recapture. It’s a trade-off that requires careful tracking.

On a related note, we often get asked about gains from partnerships. If you get a K-1 showing a capital gain, your 180-day clock to invest in a QOF typically starts at the end of the partnership's tax year, not the date of the underlying sale. This can give you a lot more breathing room to get your QOZ strategy in order.

At Blue Sage Tax & Accounting Inc., we specialize in helping NYC investors navigate the complexities of advanced tax strategies like the QOZ program. Schedule a consultation with our experts today to ensure your investment is structured for maximum benefit and full compliance.