When people talk about New York corporate income tax, they're not just talking about one single tax. It's really a franchise tax—a fee C-corporations pay for the privilege of doing business in the state. And it’s often a multi-layered system, especially if you operate anywhere near New York City.

Cracking the Code on New York's Tax System

Figuring out New York's corporate tax can feel like putting together a puzzle without the box top. For most C-corps, the final bill isn't a single number but a stack of different taxes. Getting a handle on this layered approach is the first, most critical step to staying compliant and managing your cash flow.

Think of it like a layered cake. The state tax is the base, but depending on where you are, you might have to add a couple more layers—like the MTA surcharge and the city tax—on top. Miss a layer, and you've got an incomplete (and incorrect) picture of what you really owe.

The Three Tiers of NY Corporate Tax

For a company doing business in New York, the total tax burden can come from three main sources:

- The State Franchise Tax: This is the big one. It's the baseline tax under Article 9-A that applies to almost all general business corporations that operate, own property, have employees, or even just maintain an office in New York.

- The MTA Surcharge: Formally called the Metropolitan Transportation Business Tax Surcharge, this is an extra tax slapped on corporations doing business within the Metropolitan Commuter Transportation District (MCTD). That district covers New York City plus the suburban counties of Dutchess, Nassau, Orange, Putnam, Rockland, Suffolk, and Westchester.

- New York City Business Corporation Tax (BCT): If your business is physically located within the five boroughs, you’re also on the hook for a separate city-level corporate tax. It's a completely different system, though it follows many of the same rules as the state tax.

What this all means is that a company in Manhattan faces a much different tax situation than a similar company up in Buffalo. You have to pinpoint exactly which of these taxes apply to you.

Who Actually Has to File?

As a rule of thumb, any C-corporation with "nexus" in New York must file a corporate tax return. Nexus is just a legal term for having a strong enough connection to the state that it gains the right to tax you. This connection could be obvious, like having an office or employees, but it can also be established through "economic nexus"—which just means you hit a certain threshold of sales into the state.

Here's the key takeaway: You can owe New York corporate income tax even without a single employee or physical office in the state. If you sell enough to New York customers, you've likely triggered a filing requirement.

It's Not Always About Profit

One of the biggest surprises for business owners is that New York can demand a tax payment even when you don't make a dime of profit. Why? Because the state doesn't just tax your income. It actually calculates your tax bill three different ways and makes you pay whichever amount is the highest.

The three tax bases are:

- A tax on your Entire Net Income (what you'd think of as profit).

- A tax on your Business Capital that's tied to New York.

- A Fixed Dollar Minimum tax that’s based on your gross sales in the state.

This "highest-of-three" structure guarantees that nearly every active corporation pays something, creating a reliable revenue floor for the state. Understanding this rule is absolutely fundamental to forecasting your New York tax bill and sets the stage for everything else we'll cover.

How New York Determines Your Tax Bill

If you're used to the federal tax system or how most other states handle corporate taxes, New York is going to feel a little different. Instead of a single, straightforward calculation based on your profits, the state uses a "highest-of-three" method under Article 9-A to figure out your final franchise tax. This system is designed to create a stable revenue stream for the state, but it often catches business owners by surprise.

Here’s the deal: you have to calculate your tax bill using three completely separate formulas. Once you have the three numbers, your official state tax bill is simply the largest of the three. That means a business could owe a hefty tax bill even in a year where it didn't make a dime, all depending on its assets or sales volume.

This multi-pronged approach ensures that pretty much every business contributes something. It's a massive revenue generator for the state, and the number of Article 9-A filers actually grew by 8.7% between 2015 and 2021. Interestingly, while over 78% of these companies had a tax bill under $1,000, it's the big players—fewer than 0.2% of all filers—that paid between 64.9% and 74.0% of the total tax collected. You can dig deeper into these figures in the state's official report on corporate tax statistics.

The Three Competing Tax Bases

To get a handle on your potential tax liability, you really have to understand how each of these three calculations works. They look at completely different parts of your business, from your bottom line to your physical and financial footprint in the state.

-

Entire Net Income (ENI) Base: This is the one that feels most like a typical "income tax." You start with your federal taxable income and then make a series of New York-specific adjustments, like adding back any state and local taxes you deducted on your federal return.

-

Business Capital Base: This calculation has nothing to do with your company's profits. Instead, it's based on the value of your business assets—things like real estate, equipment, and investments—that are allocated to New York.

-

Fixed Dollar Minimum Base: This is the simplest of the bunch. It's just a flat fee determined by a tiered schedule based on your total New York gross receipts. The more you sell in New York, the higher the fee.

The most important thing to remember is that you don't get to pick the formula that works best for you. New York law is clear: you must run the numbers for all three and pay whichever amount is highest.

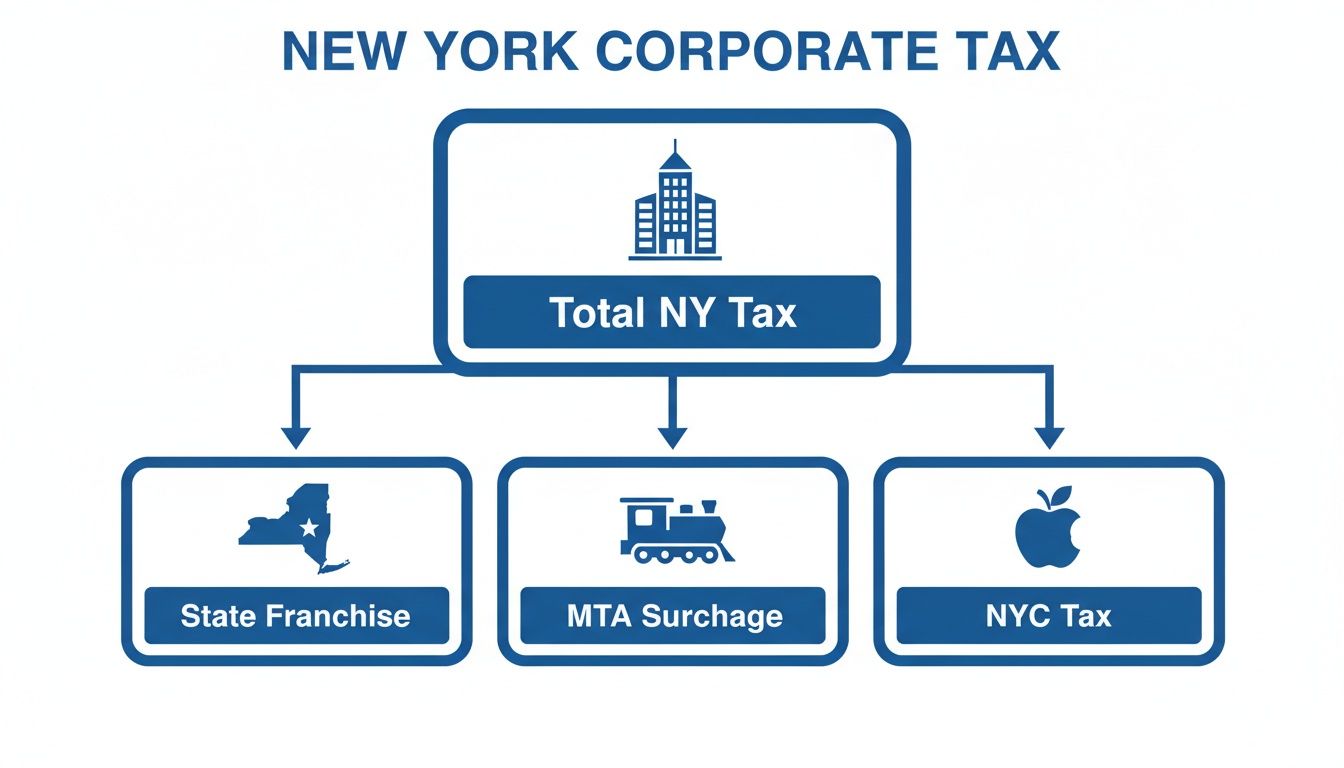

This breakdown shows the main pieces that can make up a company's total tax bill in New York.

As you can see, the final amount you write on the check is often a combination of the state franchise tax, a possible MTA surcharge, and, for businesses in the five boroughs, a separate NYC tax.

Comparing the Three NY Corporate Tax Bases

Laying the three methods out side-by-side really helps clarify when each one is most likely to kick in and become your primary tax calculation.

| Tax Base | How It's Calculated | When It Typically Applies |

|---|---|---|

| Entire Net Income | (Federal Taxable Income +/- NY Adjustments) x NY Tax Rate | This is the most common base for consistently profitable companies with strong net earnings. |

| Business Capital | (Total Business Capital x Apportionment Factor) x Tax Rate | This often applies to businesses with significant physical assets or investments in NY but low profits. |

| Fixed Dollar Minimum | Based on a tiered schedule of your NY gross receipts | This usually applies to startups, businesses operating at a loss, or companies with high sales but slim margins. |

At the end of the day, a highly profitable company will almost certainly pay based on its net income. On the flip side, a real estate holding company with valuable properties but very little rental income might find its tax is determined by the business capital base. This unique system makes proactive tax planning an absolute must for any corporation doing business in the Empire State.

Cracking the Code on Tax Rates and the MTA Surcharge

Once you’ve figured out what New York is going to tax, the next logical question is, "at what rate?" The New York corporate income tax isn't a simple flat tax. It's a tiered system based on your income, and for a huge number of businesses, there's another significant layer on top that can really move the needle on your final tax bill.

The state's approach is progressive, meaning the rate adjusts based on your profitability. This structure is designed to ask more from larger, more successful corporations while giving smaller businesses a bit of a break.

The State Corporate Tax Rate Structure

New York's main corporate tax is based on your Entire Net Income (ENI). For the vast majority of businesses, this is the calculation that matters most. The rate you'll pay hinges on which income bracket you fall into.

Following the economic strain of the COVID-19 pandemic, New York made a temporary but significant change, increasing its top corporate tax rate. In 2021, the rate for companies earning over $5 million jumped from 6.5% to 7.25%. This was a major policy move to help shore up funding for public services, a change you can read more about in a detailed report from the Fiscal Policy Institute.

Here’s how the rates break down:

- For businesses with an ENI of $5 million or less, the tax rate is 6.5%.

- For businesses with an ENI over $5 million, the tax rate is 7.25%.

It’s crucial to know that this higher rate has been extended, so you need to factor it into your financial planning for the foreseeable future.

The All-Important MTA Surcharge

If you do business in or around New York City, the state tax is just the beginning. There's another critical—and often costly—piece of the puzzle: the Metropolitan Transportation Business Tax Surcharge, better known as the MTA surcharge.

Think of it as a hyper-local tax specifically designed to fund the sprawling public transit system that keeps the region’s economy humming. If your business has a footprint within the Metropolitan Commuter Transportation District (MCTD), this surcharge applies to you.

The MTA surcharge is calculated based on your tax liability before you apply most of your tax credits. This is a key detail, as it can dramatically inflate your effective tax rate and is a must-know for any business forecasting its finances in the region.

The current MTA surcharge is a hefty 30% of the tax you owe on your ENI. It's a substantial number that can easily catch unprepared business owners off guard.

Which Counties Are in the MCTD Zone?

The surcharge isn't just a "New York City" tax; it covers a much wider area. If you conduct business in any of the counties within the district, you're on the hook.

The full list includes:

- New York City: Bronx, Kings (Brooklyn), New York (Manhattan), Queens, and Richmond (Staten Island).

- Suburban Counties: Dutchess, Nassau, Orange, Putnam, Rockland, Suffolk, and Westchester.

If your corporation operates in any of these twelve counties, you’ll need to calculate and pay the MTA surcharge on top of your regular New York corporate income tax.

Let's put it into practice. Imagine a marketing firm in Manhattan has a state tax bill of $100,000. They'd owe an additional $30,000 for the MTA surcharge, making their total state-level bill $130,000. A manufacturing company out in Suffolk County with the exact same state tax liability would face the exact same $30,000 surcharge. This shows how the tax creates a higher burden for businesses across the entire downstate region, not just within the five boroughs.

Untangling Nexus and Apportionment in New York

If your business operates in multiple states, you’ve probably asked the big question: "How much of my income does New York get to tax?" The answer lies in two concepts that every multistate business owner needs to understand: nexus and apportionment.

Think of it this way: nexus is the "on" switch. It's the minimum connection your business must have with New York for the state to have the right to tax you in the first place. Once that switch is flipped, apportionment is the formula New York uses to figure out its fair share of your company's income pie.

Let's break down how this works in the real world.

What Creates a Taxable Connection (Nexus)?

For a long time, the rule was simple: if you had "boots on the ground" in New York—an office, a warehouse, employees—you had nexus. That physical presence test is still very much alive and well.

But the game changed with the rise of e-commerce and remote services. To keep up, New York introduced economic nexus. This means you can trigger a tax obligation without ever setting foot in the state.

-

Physical Nexus: This is the old-school standard. It’s created by having a physical tie to the state, like leasing an office, owning property, or having employees who regularly work there. Pretty straightforward.

-

Economic Nexus: This is the modern, sales-based standard. For New York corporate tax, if your business has $1 million or more in sales sourced to the state in a year, you have economic nexus. This is a huge deal for out-of-state companies that sell a lot to New York customers online.

The bottom line is this: a business in California with zero employees or property in New York can still owe New York corporate tax if it sells over $1 million worth of goods or services to New York customers. This is a game-changer for e-commerce and digital service companies.

How New York Slices the Pie: The Single-Sales Factor

Once you've established nexus, the next step is determining how much of your income is subject to New York tax. Many states use a complicated three-factor formula that looks at your property, payroll, and sales.

New York decided to keep things much simpler. The state uses a single-sales factor apportionment formula.

This is a big deal. It means the only thing that matters when dividing up your income is your sales. The percentage of your company's total sales that comes from New York determines the percentage of your total income that New York gets to tax.

For example, if 20% of your company's total nationwide sales are to customers in New York, then you’ll pay New York corporate tax on 20% of your apportionable business income.

Which Sales Count as "New York Sales"?

Getting this part right is absolutely critical. New York has specific rules for sourcing different kinds of revenue, but the core idea is to follow the money to where the customer gets the benefit.

-

Tangible Personal Property: For physical goods, it’s simple. The sale is sourced to New York if the product is shipped or delivered to a customer in the state.

-

Services: Here, you follow the benefit. If you’re a consultant providing services to a company in Manhattan, that revenue is sourced to New York.

-

Digital Products: Receipts from software, streaming, and other digital products are sourced to New York if the customer uses the product in the state. The customer's billing address is usually the best indicator for this.

Let’s put it all together with an example. Imagine a software company based in Texas. It has $10 million in total sales and a net income of $1 million. Of those sales, $2 million comes from subscriptions sold to customers with New York billing addresses.

Because of the single-sales factor, 20% of the company's sales ($2M / $10M) are sourced to New York. Therefore, 20% of its $1 million net income—or $200,000—is the amount subject to New York corporate income tax.

Combined Reporting and the NYC Tax Labyrinth

If you think you've got New York's corporate tax system figured out, don't get too comfortable. There are two major curveballs that often trip up even seasoned business owners: mandatory combined reporting and the completely separate New York City tax regime. Getting these right is absolutely critical for staying compliant and making smart financial decisions.

Think of combined reporting this way: it’s like New York is taking a family photo. If a parent company and its kids (the subsidiaries) are all part of the same family business, New York wants them all in one picture for tax purposes. They file a single, unified return. Why? To stop companies from playing shell games—shuffling profits around to subsidiaries in lower-tax jurisdictions to shrink their tax bill.

When Do You Have to File a Combined Return?

You can't just choose to file a combined return; New York tells you when you have to. It's mandatory for related corporations that meet two specific tests, ensuring only truly integrated businesses are lumped together.

First up is the ownership test. This one's straightforward: a parent company has to own or control more than 50% of the voting stock of its subsidiaries. This solidifies the financial tie between them.

The second, and often trickier, condition is the unitary business test. This isn't about numbers; it's about how the businesses actually operate together. Are they sharing resources? Is management intertwined? Does one company's success depend on the other's?

Imagine a clothing brand that owns a separate company just for its e-commerce sales. If that e-commerce site only sells the parent company’s clothes, they're almost certainly a unitary business. They'll have to file a combined return.

The bottom line is, if the companies are so deeply connected that they really function as one economic unit, New York expects them to file their taxes as one.

Don't Forget About New York City

Doing business in the five boroughs? Welcome to another layer of tax complexity. On top of the state franchise tax and the MTA surcharge, you're also on the hook for the New York City Business Corporation Tax (BCT). This isn't a state tax; it's a completely separate system run by the NYC Department of Finance.

The good news is that the BCT is structured a lot like the state's system. It uses a similar "highest-of-three" approach to figure out your tax bill, based on:

- Your net income allocated to NYC

- Your business capital allocated to NYC

- A fixed-dollar minimum tax

While the structure is familiar, the rates and rules are different. For most C-corporations, the standard NYC BCT rate is a hefty 8.85% on net income.

This city-level tax can be a real gut punch to a company's finances. The BCT, which started in 2015, dramatically changed the game for city-based businesses. In fact, after the federal Tax Cuts and Jobs Act of 2017, city tax collections shot up by a staggering 46.2% in 2018 as corporate profits soared. You can dig into the numbers yourself in a fascinating report from the NYC Comptroller.

Managing your New York State and New York City tax filings requires two distinct, careful analyses. You have to correctly apportion your business activity to both the state and the city. Forgetting that these are two separate obligations is one of the most common—and expensive—mistakes a business can make in NYC.

Key Tax Credits and Filing Essentials

Getting a handle on the New York corporate income tax rules is one thing, but filing correctly and finding every possible saving is how you actually come out ahead. Let's get into the practical details you'll need to manage your tax filings and hopefully shrink your final bill.

First things first: know your deadlines. For C-corporations, the New York State corporate tax return, known as Form CT-3, is due on the 15th day of the fourth month after your fiscal year ends.

For the vast majority of businesses that run on a standard calendar year, that date is April 15th. If you know you're going to need more time, you can get an automatic six-month extension by filing Form CT-5. That pushes your filing deadline to October 15th, but don't get tripped up—it's an extension to file, not an extension to pay. You still have to estimate what you owe and pay it by the original April deadline to steer clear of penalties and interest.

Unlocking Savings with Major Business Tax Credits

Beyond just filing on time, smart businesses can make a serious dent in their tax liability by using New York’s business tax credits. The state created these programs to encourage specific activities, from hiring more people to investing in new technology. While New York offers a whole menu of credits, a few really stand out for their potential impact.

A tax credit is a dollar-for-dollar reduction of the tax you owe. This makes them way more powerful than a deduction, which just lowers your taxable income. A $10,000 credit saves you a full $10,000 in taxes. It's that simple.

Figuring out which credits your business can claim is one of the single most effective tax planning moves you can make. It's always a good idea to chat with your tax advisor at Blue Sage Tax & Accounting Inc. to see what opportunities are on the table for you.

Spotlight on Impactful NY Tax Credits

Here are three of the most significant credits that help a wide range of New York businesses:

-

Excelsior Jobs Program: This is New York's big one for job creation. If you're in a key industry—think tech, manufacturing, or life sciences—you can earn refundable tax credits for creating and keeping new jobs in the state. The program isn't just one credit; it has components for jobs, investments, and even R&D.

-

Investment Tax Credit (ITC): This credit rewards businesses for investing in themselves. You can claim a credit for buying new tangible personal property, like machinery and equipment, that's primarily used for production or manufacturing right here in New York. The credit can be as high as 5% of what you invested.

-

Research and Development (R&D) Tax Credit: Built to spark innovation, this credit is for any business with qualified research expenses in New York. It’s designed to work alongside the federal R&D credit, so it’s a fantastic way for companies in software, engineering, and science to get a double benefit for their innovation efforts.

Each of these credits comes with its own set of rules and calculations. For instance, the ITC is mostly for property used in production, while the Excelsior Program demands a detailed application and a firm commitment to hitting job growth targets. Nailing down the right fit for your business and keeping meticulous records are the keys to successfully claiming these benefits and lowering your overall New York corporate income tax.

Answering Your Top NY Corporate Tax Questions

When you start digging into New York’s corporate tax rules, a few questions almost always pop up. Let's clear up some of the most common points of confusion so you can steer clear of expensive mistakes.

Franchise Tax vs. Income Tax: What's the Deal?

So, what's the actual difference between a "franchise tax" and a regular "income tax"? The easiest way to think about it is that a franchise tax is the price of admission—it’s a fee you pay for the privilege of doing business in New York.

While it's mostly calculated on your profits, the key difference is the alternative calculations. New York also looks at a capital base and a fixed minimum tax. This means your company could owe franchise tax even if you didn't turn a profit for the year. A pure income tax, on the other hand, only ever kicks in when you have net income.

How Does New York Handle S-Corporations?

S-corps are what we call "pass-through" entities, meaning they typically don't pay corporate income tax themselves. Instead, the profits (or losses) flow through to the individual shareholders, who then report that income on their personal tax returns.

But this is New York, so there's a small catch. S-corporations are still on the hook for a fixed dollar minimum tax at the entity level. The exact amount depends on the company's gross receipts that are sourced to the state.

I Run an E-Commerce Site. Do I Owe NY Tax?

My e-commerce business has no physical office or employees in New York, so am I in the clear? Not so fast. You very well could be on the hook if you have what’s called economic nexus.

New York established a sales threshold of $1 million in receipts from New York customers. If your out-of-state business crosses that sales figure within a single year, you've created nexus. That means you're required to register, file a New York corporate tax return, and pay tax on the income you've apportioned to the state.

This is a huge deal for digital businesses. It applies even if you have zero physical presence—no office, no warehouse, no employees. The economic nexus rule is something every online seller with a New York customer base needs to understand.

What Are the Most Common Filing Mistakes?

Where do businesses usually trip up? Here are the most frequent errors we see:

- Forgetting to calculate the tax on all three bases—income, capital, and the fixed minimum—and then failing to pay the highest of the three.

- Incorrectly sourcing receipts when figuring out their apportionment factor. This is an easy place to make a costly error.

- Overlooking the mandatory combined reporting rules for affiliated companies.

- Forgetting to add back state and local taxes to their income. These are not deductible for New York tax purposes.

Navigating these rules demands more than just filling out forms; it requires a real strategy. The team at Blue Sage Tax & Accounting Inc. specializes in state and local tax planning, helping businesses in New York City and beyond stay compliant while keeping their tax burden as low as legally possible. You can learn more about our approach at https://bluesage.tax.