When you're self-employed, figuring out your tax obligations can feel like a puzzle. But when it comes to self-employment tax, the formula is surprisingly direct. At its core, you'll be multiplying 92.35% of your net self-employment income by a 15.3% tax rate.

This process covers your contributions to Social Security and Medicare—the same funds W-2 employees pay into, but with a twist.

Your Quick Answer to Calculating Self Employment Tax

If this is your first time dealing with self-employment tax, it can seem a little daunting. The main thing to remember is that you're covering both the employee and employer portions of Social Security and Medicare taxes (often called FICA taxes). As a business owner, you're essentially wearing both hats.

The starting point is always your net earnings—that's your total business income after you've subtracted all your legitimate business expenses. But here's the good news: you don't pay tax on the whole amount. The IRS only taxes 92.35% of your net earnings. This little adjustment is the government's way of giving you a break, similar to the deduction employers get for paying their share of FICA.

The Core Numbers You Need

Before you can run the numbers, you need to know the key rates. These components come together to form the total self-employment tax.

Here's a quick reference table with the figures you'll be working with.

Core Components of Self Employment Tax

| Component | Rate / Amount | What It Means for You |

|---|---|---|

| Net Earnings Multiplier | 92.35% | You only pay SE tax on this portion of your net business profit. |

| Social Security Tax Rate | 12.4% | This applies to your earnings up to an annual wage base limit. |

| Medicare Tax Rate | 2.9% | This applies to all of your net self-employment earnings, with no limit. |

| Total SE Tax Rate | 15.3% | This is the combined Social Security (12.4%) and Medicare (2.9%) rate. |

Having these figures handy makes the calculation much more straightforward.

Let's walk through a quick example. Imagine you netted $50,000 from your business this year.

- First, you find your taxable base: $50,000 x 0.9235 = $46,175.

- Next, apply the 15.3% tax rate: $46,175 x 0.153 = $7,064.78.

And there's one more benefit. You get to deduct one-half of your self-employment tax ($3,532.39 in this case) from your income when calculating your adjusted gross income (AGI). It's a valuable deduction that lowers your overall income tax bill.

If you want to dig deeper into the nuances, you can find more insights in this 2025 self-employment tax guide on taxfyle.com.

Key Takeaway: The self-employment tax is simply your way of contributing to Social Security and Medicare. While you pay both the "employee" and "employer" share, the tax code gives you important deductions to help even the playing field.

First Things First: Nailing Down Your Net Earnings

Before we even touch the 15.3% self-employment tax rate, we need a solid starting point. Everything hinges on one number: your net earnings from self-employment. This isn't your total sales or the sum of all your invoices. It's your profit—what's left after you subtract every single legitimate business expense.

Honestly, getting this number right is the most important part of the whole exercise. Why? Because every dollar in deductions you miss is a dollar you'll pay tax on, plain and simple. It all starts with accurately filling out your Schedule C (Form 1040), Profit or Loss from Business.

What Can You Actually Deduct?

So, what counts as a business expense? The IRS has a straightforward rule: it has to be both "ordinary and necessary" for your line of work. An "ordinary" expense is something common in your field, and a "necessary" one is anything that's helpful and appropriate for your business.

This definition is your best friend because it covers a ton of costs that can seriously reduce your taxable profit.

For freelancers and small business owners, some of the most common write-offs include:

- Home Office Costs: Got a dedicated workspace at home? You can deduct a portion of your rent or mortgage interest, utilities, and insurance.

- Software and Subscriptions: This is a big one. Think about your accounting software like QuickBooks, project management tools like Asana, or any professional subscriptions you pay for.

- Marketing and Advertising: Costs for social media ads, new business cards, your website hosting—it all counts.

- Business Travel: The price of flights, hotels, and 50% of your meals while on business trips are deductible.

Good record-keeping is non-negotiable here. Whether you use a simple spreadsheet or dedicated accounting software, track every single expense and keep a digital copy of the receipt. It's your best defense against overpaying.

Pro Tip: Don't overlook the small stuff. Bank fees for your business account, an online course to sharpen your skills, or the mileage you drive to meet a client might seem minor, but they add up. These little deductions can easily save you hundreds or even thousands of dollars over a year.

A Real-World Example: From Gross to Net

Let's see how this works in practice. Imagine you're a freelance graphic designer based in Queens, and you billed clients a total of $80,000 last year. That's your gross income.

You were diligent about tracking your expenses:

- Software subscriptions (Adobe Creative Cloud, etc.): $1,200

- New computer for work: $2,500

- Home office deduction: $3,000

- Client travel and meals: $800

- Business insurance: $500

Adding these up, your total deductible expenses come out to $8,000. To get your net earnings, just subtract your expenses from your gross income:

$80,000 (Gross Income) – $8,000 (Expenses) = $72,000 (Net Earnings)

This $72,000 is the number. It's the profit your business truly made, and it's the figure you’ll plug into Schedule SE to kick off the self-employment tax calculation.

A Practical Walkthrough of the Tax Calculation

Okay, you’ve nailed down your net earnings. Now for the fun part: figuring out the actual self-employment tax. This can feel a little intimidating at first glance, but it's really just a two-part math problem to cover your Social Security and Medicare obligations.

Let's walk through it together using the $72,000 net profit we figured out for our freelance graphic designer.

First things first, there's a crucial adjustment you have to make. You don't actually pay self-employment tax on 100% of your net profit. The IRS only taxes 92.35% of it. Think of this as a small break, designed to level the playing field since W-2 employees don't pay FICA taxes on the half their employer covers.

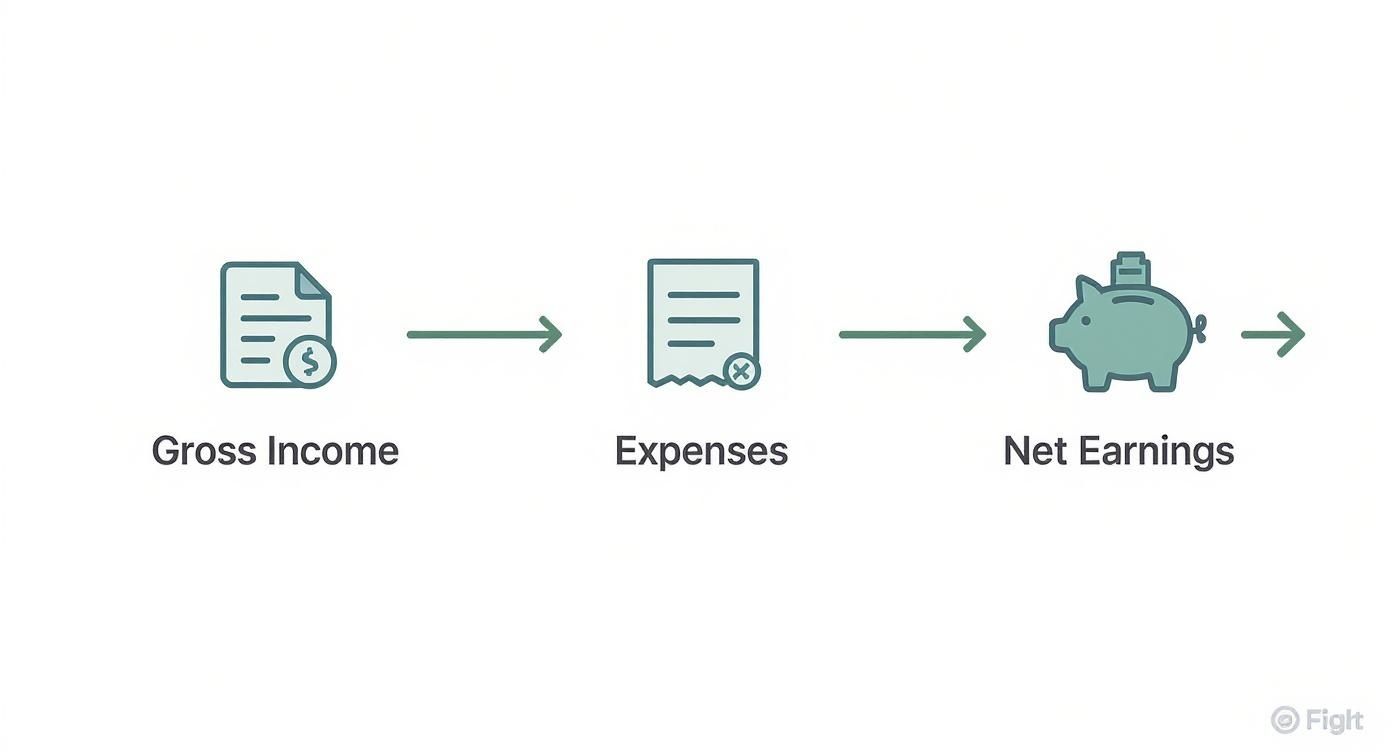

This quick flowchart shows how your gross income gets whittled down by expenses to arrive at the net earnings that matter for this calculation.

The takeaway here is simple: only your final profit—after you’ve subtracted every legitimate business expense—is what you’ll use to figure out your tax.

Applying the SE Tax Rate

With that in mind, let's find our designer's taxable base:

$72,000 (Net Earnings) x 0.9235 = $66,492

This $66,492 is the magic number, the amount that's actually subject to self-employment tax. The next move is to apply the combined 15.3% tax rate. This rate is a mix of two different components:

- 12.4% for Social Security

- 2.9% for Medicare

So, the math looks like this:

$66,492 x 0.153 = $10,173.28

And there you have it. Our designer’s self-employment tax for the year comes out to $10,173.28. This is the standard playbook: find your net profit, multiply by 92.35%, and then by 15.3%. That gets you your SE tax liability. If you'd like to see more examples, this guide from Northwestern Mutual breaks down the process nicely.

A Quick Note on High Earners: That 12.4% Social Security tax isn't unlimited. It only applies up to a certain income cap, which the government adjusts for inflation each year. For 2024, that limit is $168,600. Any self-employment earnings you have above that threshold are off the hook for Social Security tax. The 2.9% Medicare tax, however, applies to every single dollar you earn—no cap.

An Example with the Social Security Limit

Let's switch gears and look at a high-earner. Imagine a successful consultant in Manhattan who pulled in net self-employment earnings of $200,000.

-

Find the Taxable Base:

$200,000 x 0.9235 = $184,700 -

Calculate the Social Security Portion:

Here's where the cap kicks in. The Social Security tax only applies to the first $168,600 of her earnings.

$168,600 x 0.124 = $20,906.40 -

Calculate the Medicare Portion:

Remember, Medicare has no limit. It applies to the full taxable base.

$184,700 x 0.029 = $5,356.30 -

Find the Total SE Tax:

Now we just add the two parts together.

$20,906.40 (Social Security) + $5,356.30 (Medicare) = $26,262.70

As you can see, understanding how that wage cap works is absolutely essential for anyone with high earnings to get their tax calculation right. This is the final number you'd report on your Schedule SE.

Tying It All Together on Your Tax Return

You’ve done the heavy lifting of calculating your self-employment tax, but you’re not quite at the finish line. The final step is connecting that number back to your main tax return, the Form 1040. This is where a fantastic tax-saving opportunity comes into play—one that many new business owners completely miss.

The IRS gives self-employed folks a pretty significant break: you get to deduct one-half of what you pay in self-employment tax. This isn't just another business expense you'd list on your Schedule C. It's a special deduction that directly cuts down your overall income tax bill.

Why This "Above-the-Line" Deduction is So Powerful

What makes this deduction so great is that it's considered "above-the-line." This is tax-speak for a deduction you can take to lower your Adjusted Gross Income (AGI), and you report it right on Schedule 1 of your Form 1040.

The best part? You don't have to itemize your deductions on Schedule A to get this benefit. Everyone who pays self-employment tax qualifies.

Lowering your AGI is a huge win. AGI is the master number the IRS uses to decide if you qualify for all sorts of other credits and deductions. So, this one simple adjustment can create a positive ripple effect, potentially shrinking your income tax liability in several ways.

Let’s circle back to our freelance graphic designer. We figured out she owed $10,173.28 in self-employment tax. Now, let's see how the deduction works for her:

- Total SE Tax Owed: $10,173.28

- Deductible Portion (50%): $5,086.64

She gets to subtract that $5,086.64 directly from her income. It's a straightforward way to reduce the amount of money she'll actually pay income tax on.

Why Does the IRS Give This Deduction?

It's all about fairness. Think about it: a traditional employer pays half of an employee's FICA taxes (7.65%) and gets to write that off as a business expense. The one-half SE tax deduction is the IRS's way of giving you, the business owner, a similar tax break since you're paying both the employer and employee portions.

Putting the Numbers in the Right Places

Once you have your final SE tax figure and the deductible half, you need to plug them into the correct spots on your tax return. It's a simple flow from one form to another:

- Your total SE tax (our designer's $10,173.28) goes onto Schedule 2, which is for "Additional Taxes." That total then gets carried over to your main Form 1040.

- The deductible half of your SE tax (the $5,086.64) is entered on Schedule 1, under "Additional Income and Adjustments to Income."

Taking this final step is crucial. It ensures you’ve not only paid what you owe for Social Security and Medicare but have also claimed the valuable tax break you’ve earned. Forgetting this deduction is literally leaving money on the table for the IRS to keep. It's a simple, but absolutely critical, part of doing your taxes right and keeping your bill as low as possible.

Handling Tricky Tax Scenarios for Freelancers

Freelance life rarely fits into a neat box, and your tax situation often reflects that. Once you get the hang of the basic self-employment tax calculation, you'll inevitably run into circumstances that add a new layer of complexity. These edge cases are more common than you'd think, but they demand careful attention to make sure you're getting things right.

A classic example is juggling a traditional W-2 job alongside your freelance work. If this is you, it's absolutely critical to understand how your day job wages affect your freelance tax obligations. Here’s the key: your W-2 earnings are counted first toward the annual Social Security wage base limit.

What this means in practice is that if your W-2 salary already exceeds the limit (for 2024, that's $168,600), you won't owe the 12.4% Social Security portion of the SE tax on your freelance income at all. You’re not completely off the hook, though. You will still owe the 2.9% Medicare tax on every single dollar of your self-employment profit.

Juggling Multiple Ventures and Partnerships

What if you're an entrepreneur with more than one hustle? Maybe you're a web developer by day and run an e-commerce shop by night. The IRS doesn't care that they're separate businesses; they want you to combine the net profits and losses from all your sole proprietorships. You’ll calculate your total self-employment tax based on this single, combined figure.

Partners in a partnership face a slightly different setup. Your share of the partnership’s income is generally subject to self-employment tax. This almost always includes guaranteed payments you receive for your services, which are treated just like self-employment earnings. Your K-1 form from the partnership will break down the exact amounts you need to report on Schedule SE.

For high earners, there’s another layer to watch out for: the Additional Medicare Tax. This is an extra 0.9% tax that kicks in on earnings over certain thresholds (for example, $250,000 for those married filing jointly). This tax applies to your combined income from both W-2 wages and your self-employment earnings.

Is an S Corporation Right for You?

As your business grows and profits climb, you might start wondering if there's a more tax-efficient way to structure things. This is where forming an S corporation can be a powerful strategy to lower your self-employment tax bill.

Navigating these different scenarios can be a lot to handle. Here’s a quick breakdown of how these common situations compare and what you need to focus on for each.

How Different Scenarios Impact Your Taxes

| Scenario | Key Tax Consideration | What You Need to Do |

|---|---|---|

| W-2 Job + Freelancing | Your W-2 wages count first toward the Social Security limit. | Keep a close eye on your W-2 earnings. Once you hit the wage base cap, you only owe the Medicare portion on freelance profits. |

| Multiple Businesses | Combine net profits and losses from all Schedule C activities. | Consolidate the final numbers from all your ventures onto a single Schedule SE. |

| Partnership Income | Your share of partnership income and guaranteed payments are subject to SE tax. | Use the figures provided on your Schedule K-1 to complete your Schedule SE accurately. |

| S Corporation | You pay yourself a "reasonable salary" (subject to FICA), but profit distributions are not subject to SE tax. | Work with a tax pro to set a defensible "reasonable salary" and manage your payroll obligations correctly. |

The S corp structure is a game-changer for many because it allows you to take profits out of the business as distributions, which escape self-employment taxes. You still have to pay yourself a reasonable salary—which is subject to standard FICA payroll taxes—but the savings on the distributions can be massive. This is a strategic move, though, and it’s one that really requires careful planning with an experienced tax advisor.

Common Questions About Self-Employment Tax

Once you get the hang of the basic calculation, you start running into real-world "what if" scenarios. Let's walk through some of the most common questions I hear from freelancers and business owners.

A classic one is juggling a full-time W-2 job with a side hustle. If that's you, remember this: the IRS looks at your W-2 wages first when applying the annual Social Security wage base limit. So, if your day job salary already puts you over that threshold, you're off the hook for the 12.4% Social Security part of your SE tax. You still have to pay the 2.9% Medicare tax on your freelance profits, though. That part never goes away.

What If My Business Didn't Make Money?

This question comes up a lot, especially for new businesses. The answer is a simple and welcome one: no, you don't.

Self-employment tax is a tax on net profit. If your business expenses topped your gross income, you have a net loss. With no profit, there’s nothing for the IRS to tax. This is why tracking every single business expense on your Schedule C is so crucial—it ensures you're only taxed on what you actually earned.

Key Takeaway: Think of self-employment tax as a profit tax. No profit, no tax. It’s a huge relief for entrepreneurs during a tough year or in the startup phase and highlights why claiming every legitimate deduction is non-negotiable.

Do I Pay All This Tax at Once?

Please don't. Waiting until tax day to pay a year's worth of self-employment tax is a recipe for a painful surprise and potential underpayment penalties.

Instead, the IRS expects you to pay as you go through estimated taxes. This means making quarterly payments that cover both your income tax and your self-employment tax. You'll use Form 1040-ES, Estimated Tax for Individuals, to figure out what you owe. The deadlines are predictable:

- April 15

- June 15

- September 15

- January 15 (of the next year)

Getting into this rhythm keeps you compliant and prevents a massive cash-flow crunch in April. It’s a financial habit every successful business owner masters.

Can Expenses Lower My SE Tax Bill?

Absolutely. This is probably the most powerful tool you have. Every dollar you spend on a legitimate business expense—what the IRS calls "ordinary and necessary"—directly cuts your net profit.

Since your self-employment tax is calculated on that net profit figure, a lower profit means a lower SE tax bill. It's that direct. So when you track expenses for things like software, your home office, or marketing, you're not just reducing your income tax. You're actively shrinking your self-employment tax liability, too.

Handling these details, especially for high-net-worth individuals in a place like New York City, demands a smart, proactive strategy. At Blue Sage Tax & Accounting Inc., we focus on providing clear guidance to help you manage your tax obligations and plan for what's ahead. Learn how our firm can bring clarity to your financial matters.