When you're figuring out your quarterly tax payments, the goal is to project your total income for the year, calculate the tax you'll likely owe, and then break that total into four payments. It sounds straightforward, but the devil is in the details. You can lean on reliable methods like the 'Safe Harbor' rule, which uses your prior year's tax as a benchmark, or the more dynamic Annualized Income Method, which is better if your income fluctuates.

Why Quarterly Tax Payments Matter in NYC

If you're pulling in significant income that doesn't have taxes withheld—a very common situation for real estate investors, partners in professional firms, or entrepreneurs here in New York City—the IRS wants its cut as you earn it. This "pay-as-you-go" system is handled through quarterly estimated tax payments.

Let's be clear: skipping these payments isn't just about getting a big tax bill in April. It’s about getting hit with underpayment penalties and interest that can eat into your hard-earned profits.

For high-income professionals and business owners in NYC, this is a critical piece of financial management. When you stack federal, state, and city taxes, the total liability gets very large, very quickly. Getting your estimates right is non-negotiable.

Who Needs to Pay Estimated Taxes

First things first, you need to know if this even applies to you. As a rule of thumb, if you expect to owe at least $1,000 in tax for the year after your withholding and credits are accounted for, you're on the hook for estimated payments.

This typically includes people like:

- Business Owners and Entrepreneurs: Income from an S-corp, partnership, or closely held business almost always requires estimated payments.

- Real Estate Investors: That rental income or the profit from a property sale? The IRS wants its share throughout the year.

- Freelancers and Gig Workers: When there's no employer handling withholding, the responsibility is 100% yours.

- Investors with Capital Gains: A big win in the market from selling stock can trigger a hefty tax bill that needs to be paid in the quarter you received the gain.

The core principle is simple: if taxes aren't being taken out of your income automatically, you have to send them in yourself. It’s a common misconception that you're fine as long as you pay in full by April 15th, but you can still face penalties for not paying evenly throughout the year.

Two Core Methods for Estimating Quarterly Taxes

When it's time to actually calculate what to send, you have two primary strategies at your disposal. The right one for you really hinges on how predictable your income is.

Here’s a quick comparison to help you decide which approach best fits your financial situation.

Two Core Methods for Estimating Quarterly Taxes

| Method | Best Suited For | Key Advantage |

|---|---|---|

| Safe Harbor Rule | Individuals with stable or growing year-over-year income. | Simplicity and penalty protection. Paying 100% (or 110% for high-earners) of your prior year's tax liability is a straightforward way to avoid penalties. |

| Annualized Income Method | Individuals with fluctuating or unpredictable income, such as from a large one-time sale or seasonal business. | Accuracy. It lets you adjust payments based on what you actually earn each quarter, so you don't overpay during leaner months. |

Choosing the right method and getting your income forecast right are the cornerstones of smart tax planning. In this guide, we'll walk you through the practical steps for each, so you can stay compliant and keep your finances on track.

Forecasting Your Income and Figuring Out Your Tax Liability

Before you can even think about sending a check to the IRS, you need a solid projection of your total annual income. This isn't a wild guess; it’s an educated forecast that becomes the bedrock of your entire tax plan. For the investors and business owners we work with here in New York City, this usually means juggling multiple, often complex, income streams that go far beyond a simple W-2 salary.

A reliable income forecast starts by looking back before you look forward. Pull out last year's financial statements, partnership K-1s, and brokerage reports. This gives you a baseline, but you have to adjust it for what's happening right now. Are you planning to sell off a large stock position? Did your S-corp have a fantastic first quarter? Those are the kinds of real-world variables that need to be folded into your numbers.

Nailing Down Your Key Income Streams

For most of our NYC clients, income isn’t just one number—it's a mosaic of earnings from different places, and each piece has its own tax rules.

Your projection needs to carefully account for every dollar coming in. This typically includes:

- Business Profits: We're talking about distributions from your S-corp or profits from a partnership, which you'll usually find detailed on a Schedule K-1.

- Rental Income: If you own property, this is your net profit after you back out all the usual expenses—mortgage interest, property taxes, repairs, and so on.

- Capital Gains: You have to project both short-term and long-term gains from selling stocks, real estate, or other assets. A single big sale can completely change your tax picture for the year.

- Interest and Dividends: It’s easy to forget, but earnings from investment portfolios, high-yield savings accounts, or bonds all count.

Once you’ve got a handle on your total gross income, the next critical step is calculating your Adjusted Gross Income (AGI). This is a hugely important number; it's what the IRS uses to decide if you qualify for all sorts of deductions and credits.

Think of your AGI as your gross income minus a specific list of "above-the-line" deductions. It’s your taxable income before you get to itemized deductions (like mortgage interest and charitable giving) or the standard deduction. Getting this number right is absolutely essential.

Weaving in the Right Deductions

To get from gross income to AGI, you need to subtract some key deductions. These are powerful because they directly lower your taxable income, which means you owe less tax. For anyone who is self-employed or owns a business, these are your best friends.

Some of the most common deductions to factor in are:

- Self-Employment Tax: You get to deduct one-half of the self-employment taxes (that’s Social Security and Medicare) you pay. For any independent contractor or business owner, this is a major tax saver.

- Retirement Contributions: Money you put into a traditional IRA, SEP IRA, or solo 401(k) can seriously reduce your AGI.

- Health Insurance Premiums: If you're self-employed and don't have access to a spouse's or company's plan, you can almost always deduct the premiums you pay for medical, dental, and even long-term care insurance.

Let’s run a quick, practical scenario. Say a freelance marketing consultant in Manhattan expects to bring in $250,000 in gross income this year. She’s smart, so she plans to max out her solo 401(k) at $23,000. She’ll also pay about $17,660 in self-employment tax, which gives her a deduction for half of that ($8,830), and she spends $12,000 on health insurance premiums.

Her projected AGI would be around $206,170 ($250,000 – $23,000 – $8,830 – $12,000). That AGI is the number she'll now use to start calculating her actual tax liability.

Tackling NYC-Specific Tax Headaches

Trying to estimate taxes in New York City throws in an extra layer of difficulty, mainly because our state and local tax rates are so high. The biggest hurdle for many high-earners we see is the State and Local Tax (SALT) deduction cap.

Right now, the federal government limits the amount you can deduct for state and local taxes—that includes property, income, and sales taxes—to just $10,000 per household. For plenty of New Yorkers with hefty property tax bills and high state/city income taxes, their actual payments blow way past that limit. The result? Their federal taxable income is higher than it would be otherwise.

When you're mapping out your tax liability, you absolutely have to account for this cap. It directly impacts your bottom line and makes accurate forecasting that much more critical to managing your total tax burden.

Using the Safe Harbor Rule to Avoid Penalties

When you're trying to figure out how to estimate your quarterly tax payments, the IRS offers a powerful tool called the safe harbor rule. Think of it as your best defense against the dreaded underpayment penalty. It gives you a clear, predictable benchmark, which takes the guesswork out of the equation and offers real peace of mind, especially if your income is relatively consistent year over year.

The core idea is simple: if you pay enough tax throughout the year based on specific IRS thresholds, you won't be penalized—even if your final tax bill for the current year ends up being higher than you anticipated. It’s a smart way to use a known figure (last year’s tax liability) as your guide.

Understanding the Basic Safe Harbor Thresholds

The safe harbor rule essentially gives you two paths to compliance. You're generally protected from penalties if your total payments for the year, including both withholding and estimated tax payments, meet one of these conditions:

- You pay at least 90% of the tax you owe for the current year.

- You pay at least 100% of the tax you owed for the previous year.

For most people, that second option is much easier and far more reliable. Trying to forecast your current year's income with perfect accuracy is tough, particularly if you have fluctuating capital gains or business profits. In contrast, your prior year's tax liability is a fixed, known number pulled straight from your filed return.

The real value of the safe harbor rule is its simplicity. Instead of building complex income projections, you can simply take your total tax from last year's Form 1040, divide it by four, and use that figure for your quarterly payments. It creates a straightforward, compliant payment plan.

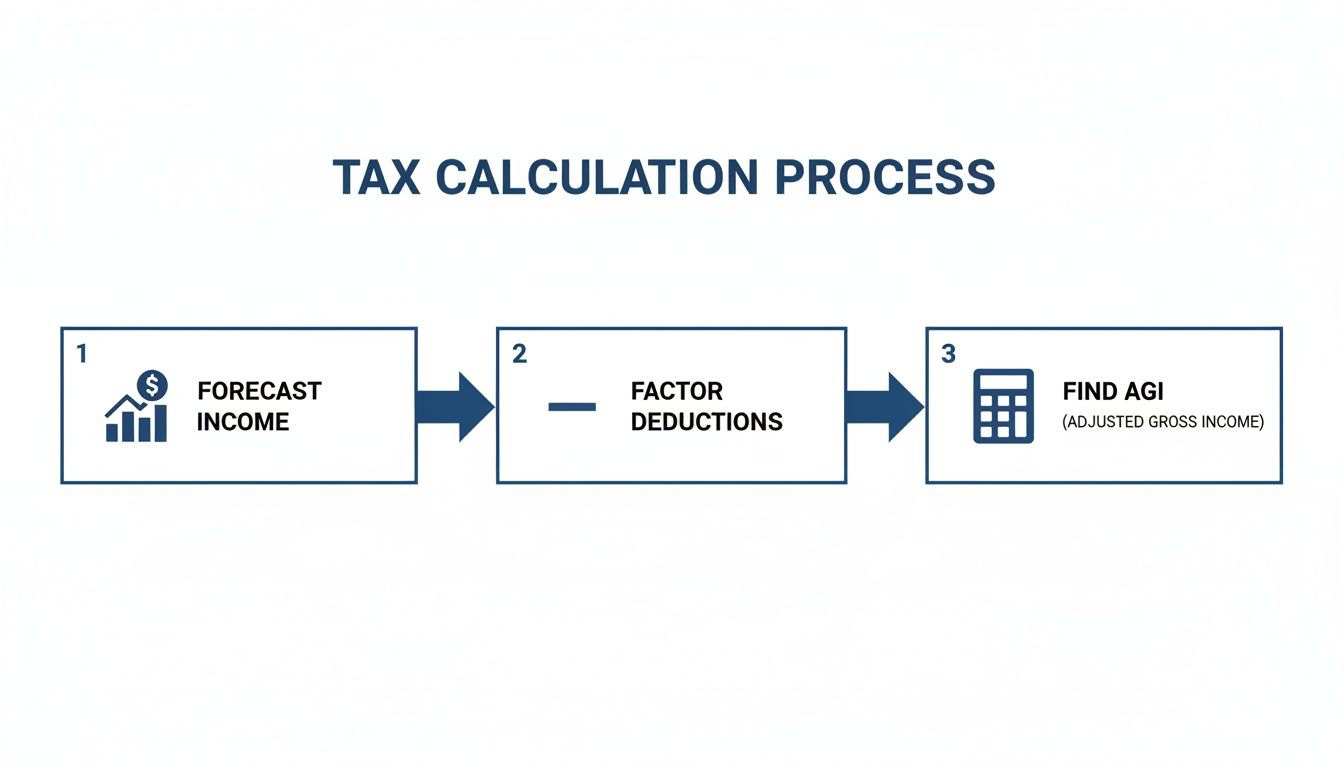

The visual below outlines the foundational steps in any tax estimation process, from forecasting income to pinpointing your AGI—a key figure for applying the safe harbor rules correctly.

This process shows that determining your Adjusted Gross Income (AGI) is a critical step before you can calculate your final tax liability and apply the safe harbor rules.

The Critical 110 Percent Rule for High Earners

Here's where things change for higher-income taxpayers—a common scenario for successful investors and business owners in New York City. This is a detail many people miss, so it’s crucial to get it right.

If your Adjusted Gross Income (AGI) from the previous year was more than $150,000 (or $75,000 if you're married filing separately), the 100% rule no longer applies. To satisfy the safe harbor, you must pay at least 110% of your prior year's tax liability.

This higher threshold is designed to ensure high earners pay a more appropriate amount of tax throughout the year, especially if their income is likely to increase. Forgetting this 110% requirement is one of the most frequent reasons high-net-worth individuals get hit with unexpected underpayment penalties. With interest on underpayments reaching 7% in recent years, sticking to the safe harbor is more important than ever. You can learn more about these strategies for estimated tax payments from Fidelity.

Safe Harbor in Action: A Real-World NYC Example

Let’s put this into a practical context. Imagine a real estate investor based in NYC who files as a single individual.

Scenario:

- 2023 AGI: $400,000

- 2023 Total Tax Liability (Federal, State, and NYC): $150,000

To figure out her 2024 quarterly payments, she needs to calculate her safe harbor amount. Since her 2023 AGI of $400,000 is well above the $150,000 threshold, she must use the 110% rule.

Here’s the simple math:

-

Calculate the Required Annual Payment: She takes her 2023 total tax of $150,000 and multiplies it by 110%.

- $150,000 x 1.10 = $165,000

-

Determine the Quarterly Payment Amount: She then divides this total by four to get her equal quarterly installments.

- $165,000 / 4 = $41,250

To stay in the safe harbor and avoid any penalties, she must pay $41,250 by each of the four quarterly deadlines. By doing so, she's fully protected, even if her income in 2024 ends up being significantly higher than it was in 2023. This strategy gives her a clear, actionable plan that simplifies her finances and protects her from unnecessary IRS fees.

Navigating Quarterly Tax Deadlines and Payment Schedules

Knowing how much to pay is only half the battle. The other half is getting those payments to the IRS on time, every single time. Miss a deadline, and you can get hit with penalties—even if you've paid the right total amount for the year.

The IRS runs on a strict "pay-as-you-go" system. This means they expect to collect taxes as you earn the income, not all at once next April. For busy investors and business owners, this requires a disciplined approach to managing your calendar and a crystal-clear understanding of the payment cycle.

Don't Let the "Quarterly" Deadlines Fool You

Here’s where a lot of people get tripped up: the term "quarterly" is a bit of a misnomer. The payment periods aren't neat, equal three-month blocks. You absolutely have to get these specific dates on your calendar and know which income period each payment covers.

The due dates are fixed mid-month landmarks that demand your attention. Here's how the income periods and deadlines actually break down:

- Q1 (Jan 1 – Mar 31): Payment due April 15

- Q2 (Apr 1 – May 31): Payment due June 15

- Q3 (Jun 1 – Aug 31): Payment due September 15

- Q4 (Sep 1 – Dec 31): Payment due January 15 of the next year

Notice that Q2 is only two months long, and Q3 is three. It’s an odd cadence, designed to align with fiscal calendars, but it’s a classic trap for the unwary. With the IRS processing over 101 million returns by early April in a typical year, this structured schedule is how they manage the flow. You can dig into more IRS filing season statistics if you're curious about the numbers.

One of the most common mistakes I see is the assumption that the fourth-quarter payment is due at the end of December. It's actually due January 15 of the following year. This detail is crucial for proper year-end financial planning.

If a due date happens to fall on a weekend or a holiday, the deadline mercifully shifts to the next business day. But a word of advice: never rely on this. It's far better to plan your payments well in advance and treat the original date as your hard deadline.

Best Practices for Staying on Schedule

For anyone juggling multiple income streams, investments, or business interests, trying to remember these dates manually is just asking for trouble. You need a proactive system to stay compliant and avoid the stress of last-minute scrambles.

Here are a few practical strategies we recommend to clients:

- Automate Your Calendar: Set up recurring digital calendar alerts for at least two weeks before each deadline. This gives you a comfortable cushion to review your numbers, finalize your calculation, and make the payment without rushing.

- Schedule Payments in Advance: The government's own payment systems, like IRS Direct Pay and EFTPS, allow you to schedule payments ahead of time. You can literally set up all four payments at the start of the year and forget about them.

- Create a Central Tax Hub: Keep a dedicated digital folder for everything related to your estimated taxes. This includes income statements, expense tracking spreadsheets, and prior-year returns. Having everything in one place makes the calculation process immeasurably smoother each quarter.

How to Actually Make the Payment

The IRS gives you several convenient ways to submit your estimated tax payments. The key is to pick the one that fits your workflow and stick with it.

- IRS Direct Pay: This is our go-to recommendation for most people. It's a free, secure way to pay directly from your checking or savings account. It’s incredibly straightforward and doesn't require any lengthy registration process.

- EFTPS: The Electronic Federal Tax Payment System is another excellent, free online service from the Treasury Department. It requires a one-time enrollment, but it offers more robust features, like the ability to view your payment history for up to 16 months.

- Debit/Credit Card or Digital Wallet: While convenient, paying via a third-party processor comes with fees. This option can make sense in a pinch, but it's the most expensive route.

- Check or Money Order: This is old-school, and honestly, it's the slowest and least secure method. If you absolutely must mail a payment, always send it via certified mail to get a dated receipt proving you sent it on time.

The Real Cost of Underpayment Penalties

Nothing gets a client's attention quite like seeing the real-world cost of a tax miscalculation. The IRS has a simple expectation: you pay your tax as you earn your income, not all at once on April 15th. If you come up short on your quarterly payments, you'll face an underpayment penalty. It's not just a slap on the wrist; it's a direct and entirely avoidable financial drain.

These penalties aren't pulled out of thin air. The IRS has a specific formula based on three things: how much you underpaid, how long that amount was overdue, and the interest rate at the time. Essentially, you're paying the government interest for the money you held onto for too long.

How Penalties Compound Over Time

You can think of an underpayment penalty as an involuntary loan from the government, and the interest rate is set by the federal short-term rate plus three percentage points. As interest rates in the broader economy go up, so does the price of underpaying your taxes. It's a real cost that can eat into your investment returns or chip away at your business's bottom line.

For business owners and active investors, this can be particularly painful. IRS interest rates for underpayments recently climbed to 7%, a significant jump from what we've seen in past years. To put that in perspective, a family office underpaying by just $10,000 would owe over $700 in interest, and that’s before any other potential failure-to-pay penalties kick in. You can track these figures yourself by checking the IRS’s own data on quarterly interest rates. This is exactly why strategies like the safe harbor rule are so crucial.

Here's the key thing to remember: the penalty clock starts running after each quarterly deadline. An underpayment in April accrues interest for far longer than one in September, which makes getting those early-year estimates right especially important.

A Real-World Penalty Scenario

Let's walk through a common example I see in my practice. Picture a real estate developer in NYC who has a fantastic year, but their income projections were a little too optimistic.

- Actual 2024 Tax Liability: $200,000

- Total Estimated Payments Made: $150,000

- Total Underpayment: $50,000

In this case, the developer didn't meet the safe harbor rule (paying at least 90% of the current year's tax or 110% of the prior year's). The IRS will now assess a penalty on that $50,000 shortfall, calculated across the four quarters it was supposed to be paid.

Assuming a 7% annual interest rate, the penalty isn't a simple 7% of $50,000. It’s a much more complex calculation based on the exact number of days each quarterly payment was late. The final penalty could easily be several thousand dollars—money that could have been reinvested into a new project but is instead lost forever.

This is why proactive tax planning isn't just about staying compliant. It's about protecting your capital. Nailing your quarterly estimates is a fundamental part of smart financial management.

When to Work with a Tax Professional

Figuring out quarterly tax payments on your own can work for a while, especially if you stick to the safe harbor rules and your income is fairly predictable. But at some point, the DIY approach becomes a real gamble.

As your financial world gets more complicated, the cost of a single mistake can easily eclipse the cost of professional advice. Knowing when to raise your hand and ask for help is just smart financial management.

When the Math Gets Messy

Certain events are red flags, signaling it's time to bring in a tax pro. These aren't just minor speed bumps; they're situations where specialized knowledge can unlock savings and prevent headaches that tax software often misses.

Think of these as clear triggers to pick up the phone:

-

You had a big financial win: Did you sell a chunk of stock, unload a rental property, or sell your business? A significant capital gain throws your typical tax liability out the window for that quarter and the rest of the year. It needs careful planning to manage the fallout.

-

You're earning money in multiple states: For business owners or real estate investors, multi-state income is a compliance minefield. Every state has its own playbook for sourcing income and offering tax credits. Trying to navigate this alone is a recipe for trouble.

-

Your business isn't a simple sole proprietorship: If you're running an S-corp, partnership, or a web of LLCs, you're dealing with a different level of complexity. A tax advisor helps you sort through reasonable compensation, basis limitations, and distributions to keep things both compliant and efficient.

From Simple Math to Smart Strategy

Working with a firm like Blue Sage Tax & Accounting is about more than just getting the numbers right for your next 1040-ES payment. It's about crafting a forward-thinking strategy that serves your bigger goals.

A tax professional doesn’t just focus on compliance. The real value comes from proactive, forward-looking advice—helping you structure a transaction to soften the tax blow, finding credits you didn't know you qualified for, and adjusting your entire plan when tax laws shift.

For example, we can run the numbers on a few different scenarios for a planned asset sale to see what makes the most sense. Or we can help you structure your business entity correctly from the get-go, saving you from costly mistakes down the line.

When we see your whole financial picture, we can build a tax plan that actually supports your growth instead of just being a reactive chore.

Answering Your Top Questions About Quarterly Taxes

Even the most buttoned-up financial plan can leave you with questions when it's time to actually cut a check to the IRS. The whole pay-as-you-go system can feel a bit backward at first, especially if you're new to it. Let's tackle some of the most common questions we get from clients to clear up the confusion.

One of the first things people ask is, "What happens if my income is all over the place?" This is the daily reality for freelancers, consultants, and business owners whose revenue can swing wildly from one month to the next.

For this exact scenario, the annualized income method is your best friend. Forget trying to base your payments on last year’s smooth, predictable income. This method lets you pay tax on what you actually earn in each quarter, preventing you from overpaying during a slow period or getting hit with a huge bill after a surprise windfall.

Can I Just Skip a Payment If My Business Lost Money?

This is a classic question from entrepreneurs after a tough quarter. If you didn't make a profit, you shouldn't have to pay tax, right?

Generally, yes. If you're using the annualized method and can show you had zero or negative taxable income for that specific period, you can likely skip that quarter's payment.

But there's a catch: you have to be ready to prove it. Your bookkeeping needs to be crystal clear. Keep in mind that a huge profit in the following quarter will mean you need to make a larger "catch-up" payment to avoid falling behind for the year and triggering penalties.

What If I Realize I've Paid Too Much?

First off, this is a much better problem to have than underpaying. If your total estimated payments end up being more than your final tax bill, you have a couple of straightforward choices when you file your annual return.

- Get a Refund: The simplest option. The IRS will send you a check for the amount you overpaid.

- Apply it to Next Year: You can roll the overpayment forward and apply it as a credit toward your first quarterly payment for the next tax year.

We often see savvy clients choose to apply the overpayment to the next year. It’s a smart way to get a head start on the following year's tax obligations and ease future cash flow demands.

Do I Owe Quarterly Payments to the State and City, Too?

Yes, and this is non-negotiable, especially for anyone living in New York City. Your estimated tax duty doesn't stop with the federal government. You are also required to make separate quarterly payments for both New York State and New York City income taxes.

The logic and deadlines are very similar to the federal system. You'll calculate your projected state and city tax liability and send those payments directly to the correct agencies. Forgetting this step is a costly mistake, as you can face underpayment penalties at the state and local levels on top of any federal ones.

Getting your federal, state, and NYC estimated taxes right requires a detailed strategy, not just a guess. For a plan built around your unique financial picture, contact Blue Sage Tax & Accounting Inc. Let's build a proactive tax strategy together. Find out how we can help at https://bluesage.tax.