At the heart of every partnership's tax story is a single, powerful concept: pass-through taxation. Unlike a traditional corporation, the partnership itself doesn't pay income tax. Instead, all of its profits, losses, deductions, and credits flow through the business directly to the individual partners.

From there, it's up to each partner to report these items on their personal tax returns and settle up with the IRS at their own individual tax rates.

The Foundation of Partnership Taxation

The best way to picture this is to think of a partnership as a transparent pipeline. The financial results of the business—good or bad—travel straight through the entity to the owners without being taxed along the way. This is a world away from how a standard C corporation operates, where the business is a separate taxable entity that pays its own income taxes first.

This pass-through design is the absolute cornerstone of partnership taxation. Its main superpower? It completely sidesteps the dreaded "double taxation" that plagues many corporations. With a C corp, profits get hit with tax once at the corporate level and then a second time when they're paid out to shareholders as dividends. Partnerships neatly avoid this.

A Tale of Two Tax Models

The difference between these two systems isn't just academic; it has a massive impact on the real, after-tax cash that ends up in an owner's pocket. By cutting out that first layer of tax at the business level, the partnership model ensures profits are only taxed once.

The primary benefit of the pass-through system is its tax efficiency. All financial outcomes, whether positive or negative, are allocated among the partners and handled on their individual returns, simplifying the process and often lowering the overall tax burden.

Let's put the two models side-by-side to really drive home the difference.

Comparing Partnership and Corporation Tax Models

This table illustrates the fundamental differences between how partnerships and C corporations handle income tax.

| Taxation Feature | Partnership (Pass-Through) | C Corporation (Separate Entity) |

|---|---|---|

| Tax at Entity Level | No, the partnership files an informational return but pays no income tax itself. | Yes, the corporation pays tax on its net profits at the corporate tax rate. |

| Tax on Profits | Profits are taxed once on each partner’s personal tax return at their individual rates. | Profits face potential double taxation—first at the corporate level, then again at the shareholder level when distributed as dividends. |

| Handling of Losses | Business losses flow through to partners, who can often use them to offset other personal income, subject to specific rules. | Business losses remain within the corporation and cannot be passed through to shareholders to offset their personal income. |

This foundational concept explains why partnerships, and LLCs that choose to be taxed as partnerships, are such popular structures. They are the go-to choice for countless closely held businesses, real estate ventures, and investment funds. The direct flow of financial results to the partners is the key that unlocks everything else we're about to explore.

The Key Tax Forms Every Partner Should Know

To really get a handle on partnership taxation, you first need to understand the annual rhythm of its tax reporting. It’s not some mysterious black box. Instead, think of it as a structured flow of information, moving from the business itself to the IRS and, finally, landing on your desk. This entire system hinges on two key documents that work in tandem to make sure every dollar of profit or loss is accounted for.

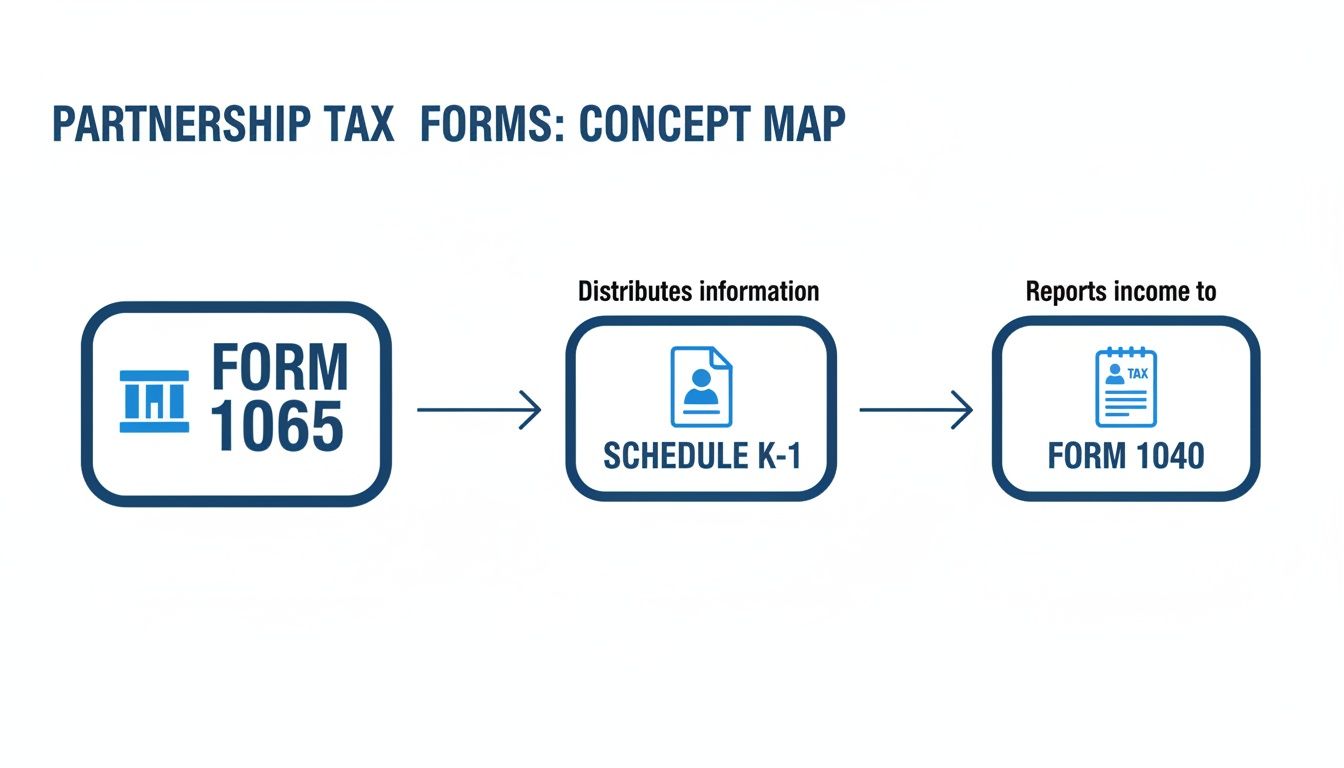

It all starts with the partnership’s own tax filing. Every year, the partnership files Form 1065, U.S. Return of Partnership Income, with the IRS. Crucially, this isn't a tax bill. It's an informational return—a detailed summary of the partnership's financial performance, tallying up all its income, gains, deductions, and losses for the year.

The Master Blueprint: Form 1065

Think of Form 1065 as the master blueprint for the partnership's entire tax year. It’s the official ledger where the business calculates its overall net income or loss. The form tells a detailed financial story, covering everything from gross sales down to specific deductions for salaries, rent, and depreciation. The final numbers here are the official record of the partnership's activities.

This level of reporting is essential for the IRS to keep tabs on the massive world of partnerships. In 2022 alone, partnerships filed over 4.5 million tax returns on behalf of 28.8 million partners. And here’s a telling trend: Limited Liability Companies (LLCs) that chose to be taxed as partnerships accounted for a whopping 72.7% of all those filings—a dominant position they've held for over two decades, which speaks volumes about their flexibility. You can dig into these trends and more in the complete partnership statistics from the IRS.

Once the partnership has Form 1065 locked in, it has everything it needs to slice up the financial pie and distribute the results to its owners. That brings us to the second document—the one that matters most to you as an individual partner.

Your Personal Tax Report Card: Schedule K-1

Using the master Form 1065 as its source, the partnership then prepares a Schedule K-1 (Form 1065) for every single partner. If Form 1065 is the blueprint for the whole building, your Schedule K-1 is the detailed floor plan for your specific unit. It itemizes your exact share of the partnership’s income, deductions, and other financial items.

Your K-1 will spell out your portion of:

- Ordinary business income or loss

- Real estate rental income or loss

- Interest, dividends, and capital gains

- Guaranteed payments

- Tax deductions and credits

This K-1 is the critical bridge connecting the partnership's return to your personal Form 1040, U.S. Individual Income Tax Return.

Your Schedule K-1 isn't just a suggestion; it's the official record of your allocated income and deductions from the partnership. You are required to report the figures from this form on your personal tax return, usually on Schedule E (Supplemental Income and Loss).

Getting your K-1 and knowing what it means is a fundamental responsibility of being a partner. It dictates exactly how much of the partnership’s success—or struggles—you have to report to the IRS. If you ignore it or report the numbers incorrectly, you're inviting audits, penalties, and a world of headaches. This little form is the key that makes the whole pass-through system work, translating the business's financial results directly onto your personal tax return.

Understanding Your Investment Through Partner Basis

Beyond the yearly tax forms, perhaps the most critical concept to grasp in partnership taxation is your partner basis. The best way to think of it is as the official, running tally of your total financial investment in the partnership. It's a dynamic number, not a static one, and it directly affects your tax bill and reflects your true economic stake in the venture. Getting a handle on how it works isn’t just an accounting chore—it's a fundamental part of managing your investment.

Your journey with basis starts the moment you become a partner. It kicks off with the value of whatever you put in, whether that's cash or property. This is your starting line, but it almost never stays the same for long.

How Your Partner Basis Changes

Your basis is constantly adjusted to reflect the partnership's financial life and your relationship with it. It’s a living number that ebbs and flows based on specific events during the tax year.

Here are the key adjustments that increase your basis:

- Your share of partnership income: When the business turns a profit, your share of that income gets added to your basis. This is true even if you don't actually see a penny of it in cash.

- Additional contributions: If you decide to invest more money or property into the business, your basis goes up by that amount.

- Your share of partnership debt: In most situations, when the partnership takes on more debt, your basis increases because you're considered to share in that new liability.

On the flip side, other events will decrease your basis:

- Your share of partnership losses: Just like profits boost your basis, your slice of any business losses will bring it down.

- Distributions to you: When the partnership pays out cash or property to you, your basis is reduced by the value of that distribution.

- A decrease in partnership debt: As the partnership pays down its loans, your share of that liability shrinks, which in turn reduces your basis.

This constant push and pull is exactly why keeping a close eye on your basis is so important for anyone trying to understand how partnerships are taxed.

Why Basis Is So Important

So, why all the fuss about this one number? Your basis plays two crucial roles that can have a massive impact on your personal tax return. First, it dictates how distributions are taxed. Second, it puts a cap on the partnership losses you can deduct.

A partner’s basis is the ultimate gatekeeper for tax-free distributions and deductible losses. If you have a positive basis, distributions up to that amount are typically a tax-free return of your investment. Once your basis hits zero, any further cash distributions are generally taxed as a capital gain.

This chart illustrates how the tax information flows from the partnership's books all the way to your personal return.

As you can see, the partnership's Form 1065 creates the Schedule K-1, which then feeds directly into your Form 1040. The basis calculation is all the behind-the-scenes work that gives these numbers their real meaning for you.

The second critical job of your basis is to limit your loss deductions. You can only deduct your share of partnership losses up to the amount of your basis. For example, if your share of losses for the year is $50,000 but your basis is only $30,000, you can only deduct $30,000 this year. The remaining $20,000 isn't lost forever—it’s simply suspended and carried forward until you have enough basis in a future year to use it.

Failing to track your basis is one of the most common—and costly—mistakes a partner can make. Without an accurate number, you could easily misreport gains, take deductions you aren't entitled to, or pay far more tax than you need to when you eventually sell your interest. It’s the foundational figure that underpins the entire tax structure of your investment.

How Active Partners Are Compensated and Taxed

When you're actively running the business, your compensation isn't always just a simple slice of the annual profits. It's critical to understand how active partners get paid—and how that pay gets taxed—to manage your own tax bill and make sure the partnership agreement actually works in practice. The two main ways this happens are through profit distributions and guaranteed payments, and they have very different tax treatments.

A regular profit distribution is just what it sounds like: your share of the business's net income. As we've covered, this income flows through to your personal return, and you pay tax on it whether you actually took any cash out or not. But what if a partner needs to be compensated for their day-to-day work, much like a salary?

Guaranteed Payments Explained

That’s where guaranteed payments enter the picture. A guaranteed payment is a fixed amount paid to a partner for their services or for the use of their capital. The key is that this payment is made without regard to the partnership’s income for the year. Think of it as a salary-like payment that a partner gets even if the business just breaks even or posts a loss.

For the partnership, these payments are typically treated as a business expense. This deduction lowers the total profit that then gets allocated among all the partners. For the partner on the receiving end, guaranteed payments are treated as ordinary income.

Guaranteed payments give active partners a predictable income stream, much like a salary. From a tax standpoint, the partnership deducts them, and the receiving partner pays ordinary income tax on them, ensuring they're compensated for their direct contributions to the business.

This tool is especially useful in partnerships where some partners are doing the heavy lifting while others are mostly providing capital. It’s a fair way to pay the working partners for their labor before the remaining profits are split according to ownership stakes.

The Impact of Self-Employment Tax

Here's something active partners can't afford to overlook: self-employment tax. This is the partner’s version of Social Security and Medicare taxes, and it's a huge piece of the puzzle. The tax applies to a general partner’s share of the partnership’s ordinary business income and to any guaranteed payments received for services.

Let's break down what's usually on the hook for this tax:

- Share of Business Income: If you're a general partner who is actively involved in the business, your cut of the net earnings from its trade or business activities is considered self-employment income.

- Guaranteed Payments: Any payments you receive for your services are also subject to self-employment tax.

This is a massive difference compared to limited partners, who are generally passive investors. A limited partner's share of income is typically not subject to self-employment tax. This distinction has become a major battleground in tax law, especially for professional service firms, investment funds, and LLCs where the line between an "active" and "passive" role can get pretty fuzzy.

Getting this wrong can lead to some nasty underpayment penalties. If you're an active partner, you have to plan for this liability all year. That usually means making quarterly estimated tax payments to the IRS to cover both your income tax and your self-employment tax obligations.

Making the Most of the Qualified Business Income Deduction

For many partners, one of the single most valuable tax breaks available today is the Section 199A Qualified Business Income (QBI) deduction. This isn't just a minor tweak to your tax return; it's a powerful provision that lets eligible partners deduct up to 20% of their share of the partnership’s income, right off the top.

The impact can be massive. Think of it as a direct discount on your business profits. If your share of qualified partnership income is $100,000, the QBI deduction could slash your taxable income by $20,000 before your regular tax rates even come into play. For anyone involved in a pass-through business, understanding how this works is fundamental to smart tax planning.

Who Actually Qualifies for the QBI Deduction?

It's not a free-for-all, though. Not every dollar of partnership income is eligible for this 20% haircut. The rules are designed to benefit most trades or businesses, but the IRS has put some important guardrails in place.

The biggest hurdle is determining whether your partnership is a regular trade or business or what the tax code calls a Specified Service Trade or Business (SSTB). Essentially, an SSTB is a business where the main "product" is the reputation or skill of its owners or employees.

This bucket includes professions like:

- Health and medicine

- Law and accounting

- Consulting and financial services

- Performing arts and athletics

If your partnership falls into the SSTB category, your ability to take the QBI deduction starts to phase out once your personal taxable income hits certain thresholds. For everyone else, the deduction is more widely available, but other limitations can still kick in.

The whole point of the QBI deduction is to give pass-through businesses a fighting chance against corporations with their lower flat tax rate. It’s not just about compliance—it's a core strategy for keeping more of what you earn from your partnership investments.

This deduction was a centerpiece of the 2017 Tax Cuts and Jobs Act (TCJA). For a partner in the top 37% tax bracket, it can effectively drop their rate on business income down to 29.6%. That's a huge deal when C-corporations are paying a flat 21%. But there's a catch: many TCJA provisions are set to expire after 2025, putting this deduction on the chopping block and creating real uncertainty for real estate partnerships and other businesses. You can get more details on this critical partnership tax debate from NAIOP.

Navigating the Key Limitations

Even if your business isn't an SSTB, the QBI deduction isn't always a straight 20%. For higher-income partners, the calculation gets more complex. Once your taxable income crosses a certain threshold, your deduction can be limited by one of two major factors:

- W-2 Wages: The first test limits your deduction to 50% of your share of the W-2 wages the partnership paid. This is meant to reward businesses that are creating jobs and paying salaries.

- Property Basis: The second test is a bit different. It limits the deduction to 25% of your share of W-2 wages plus 2.5% of your share of the unadjusted basis immediately after acquisition (UBIA) of the partnership's qualified property. This calculation is a lifesaver for capital-intensive businesses, especially real estate partnerships, which might have huge property assets but very few direct employees.

Let’s run a quick example to see this in action. Imagine a real estate partner with $500,000 in qualified business income. The partnership itself pays no W-2 wages. Under the first test, their deduction would be a big fat zero.

But, if that partner's share of the property’s basis is $4 million, the second test comes to the rescue. They could claim a deduction of up to $100,000 (2.5% of $4 million), which is much better than nothing.

This is why tracking property basis and wages is so critical for any partner with significant income. To get the most out of this deduction, you have to plan ahead and structure the partnership's activities to align with these rules. Frankly, if you want to understand how partnerships are taxed today, you absolutely have to master the QBI deduction.

Navigating State and Multi-Jurisdictional Tax Rules

While the federal rules are the foundation of partnership tax, the complexity skyrockets the moment a business operates across state lines. State and local tax (SALT) considerations add a tricky layer of compliance that can catch even seasoned investors and business owners off guard.

Once your partnership’s footprint crosses a state border, you enter a whole new world of varied tax laws, filing requirements, and income allocation methods. This isn't just a federal issue anymore. It's a multi-front compliance effort where every state plays by its own rulebook.

Establishing a Tax Footprint with Nexus

The first concept you have to get your head around is nexus. In simple terms, nexus is the minimum connection or business activity a partnership must have with a state before that state can legally force it to file a tax return and pay taxes.

And nexus isn't just about having a physical office. It can be triggered by a whole host of activities, creating a filing obligation right where you might not expect one.

Common activities that create nexus include:

- Having a physical presence, like an office, warehouse, or storefront.

- Employing remote workers who live and work in the state.

- Owning or leasing property (a huge one for real estate partnerships).

- Regularly sending salespeople into a state to solicit business.

- Hitting a certain dollar amount of sales or number of transactions in a state (this is called economic nexus).

Once you've established nexus in a new state, the partnership has to start filing returns there. This brings us to the next big challenge: figuring out how much of your income actually belongs to each state.

Slicing the Pie with Income Apportionment

A multi-state partnership can’t just pay tax on its total income in every single state where it has nexus. That would be double (or triple, or quadruple) taxation. Instead, it must apportion its income. Think of it as slicing up the total profit pie and giving each state a fair share based on how much business was actually done there.

Historically, this was often done using a three-factor formula that looked at property, payroll, and sales. But the game has changed. A growing number of states now use a single sales factor, putting all the emphasis on where the partnership's customers are located.

Apportionment is all about making sure states only tax the slice of a partnership's income that was generated within their borders. Get this wrong, and you could end up overpaying taxes in some states while facing audits for underpayment in others. It's a critical compliance task.

For example, a tech partnership based in New York City with developers in California and a major client in Texas has to carefully apply each state's unique apportionment formula. That NYC firm has to figure out how much of its share of the $2.6 trillion in reported 2022 pass-through income is attributable to each jurisdiction. The challenge is magnified on a global scale, where Pillar 2's 15% global minimum tax—agreed to by over 135 countries—creates entirely new hurdles for international partnerships. You can explore the OECD's latest findings to see how these global stats impact large-scale operations.

The PTET Workaround for the SALT Cap

One of the biggest game-changers in state partnership tax recently is the rise of the Pass-Through Entity Tax (PTET). This is a brilliant and strategic workaround to a major federal headache.

The 2017 Tax Cuts and Jobs Act (TCJA) slapped a $10,000 cap on the state and local tax (SALT) deduction for individuals. This was a massive blow to partners in high-tax states like New York and California.

In response, most states have rolled out PTET laws. Here’s how this clever maneuver works:

- The Partnership Pays: The partnership elects to pay the state income tax directly at the entity level.

- A Federal Deduction is Created: This state tax payment is a normal business expense, so the partnership deducts it in full on its federal Form 1065. Crucially, this deduction is not limited by the individual $10,000 SALT cap.

- Partners Get a Credit: The individual partners then get a credit on their personal state tax returns for their share of the tax the partnership already paid for them.

The end result? The partners effectively get a full federal deduction for their state income taxes, sidestepping the SALT cap. For high-earning partners in states like New York, making a PTET election can translate into very real federal tax savings. But be warned: the rules are complex and vary by state, so it requires careful analysis to make sure it's the right move for your specific partnership.

Common Questions on Partnership Taxation

When you get down to the brass tacks of partnership taxes, a few questions pop up time and time again. The pass-through concept makes sense on paper, but what happens when you actually take cash out of the business? Or when the business has a tough year and posts a loss? Let’s walk through some of the most common scenarios partners run into.

Are Distributions from a Partnership Taxable?

This is easily the biggest point of confusion for new partners, but the answer is surprisingly simple: usually, no.

Think of a cash distribution as a return of your own investment—it’s not new income. Instead, it simply lowers your basis in the partnership. You've already been taxed on your share of the partnership's profits for the year, whether that cash stayed in the business account or landed in your pocket.

The one major exception is when a distribution exceeds your basis. If you get more cash out than you have invested (your basis), that excess amount is treated as a taxable capital gain.

Can I Deduct My Share of Partnership Losses?

You absolutely can, but not without limits. The tax code has a few guardrails in place to make sure partners can't deduct more than they genuinely have on the line.

Your deductible loss is capped by three key rules, applied in this order:

- Your Tax Basis: First and foremost, you can’t deduct losses beyond your basis.

- Your At-Risk Amount: This rule limits your deductible losses to the amount you could actually lose in a worst-case scenario.

- Passive Activity Rules: If you’re a passive investor, you can generally only use these losses to offset income from other passive ventures.

Don't worry, any losses you can't deduct because of these limits aren't gone for good. They are suspended and carried forward, waiting to be used in a future year when you have enough basis or passive income to absorb them.

What Is the Tax Difference Between a General and Limited Partner?

The main distinction boils down to a single, crucial issue: self-employment tax. How you're classified has a direct impact on your tax bill.

A general partner is hands-on, actively running the business. Because of that active role, their share of the partnership's ordinary business income (and any guaranteed payments) is subject to self-employment taxes for Social Security and Medicare.

On the other hand, a limited partner is typically a passive investor. They have limited liability and aren't involved in management. For that reason, their share of the partnership's income is generally exempt from self-employment tax. This has become a hot-button issue with the IRS, especially as modern structures like LLPs and LLCs blur the lines between active and passive participation.

At Blue Sage Tax & Accounting Inc., our job is to bring clarity to these complex rules for investors, real estate pros, and closely held businesses. We believe in proactive planning to help you navigate the world of partnership tax and hit your financial targets. If you're ready to build a tax strategy with confidence, get in touch with us at https://bluesage.tax.