As a business owner, you're the master of your craft. You know how to build a team, serve your clients, and grow your revenue. But when it comes to your finances, it's easy to keep your business books and your personal checkbook in two completely separate worlds. This is one of the biggest—and most common—mistakes entrepreneurs make.

True financial planning isn't just about managing company cash flow; it’s about strategically weaving your business's success into the fabric of your personal wealth. It’s the blueprint that ensures your company doesn't just provide an income, but actively builds the life you want.

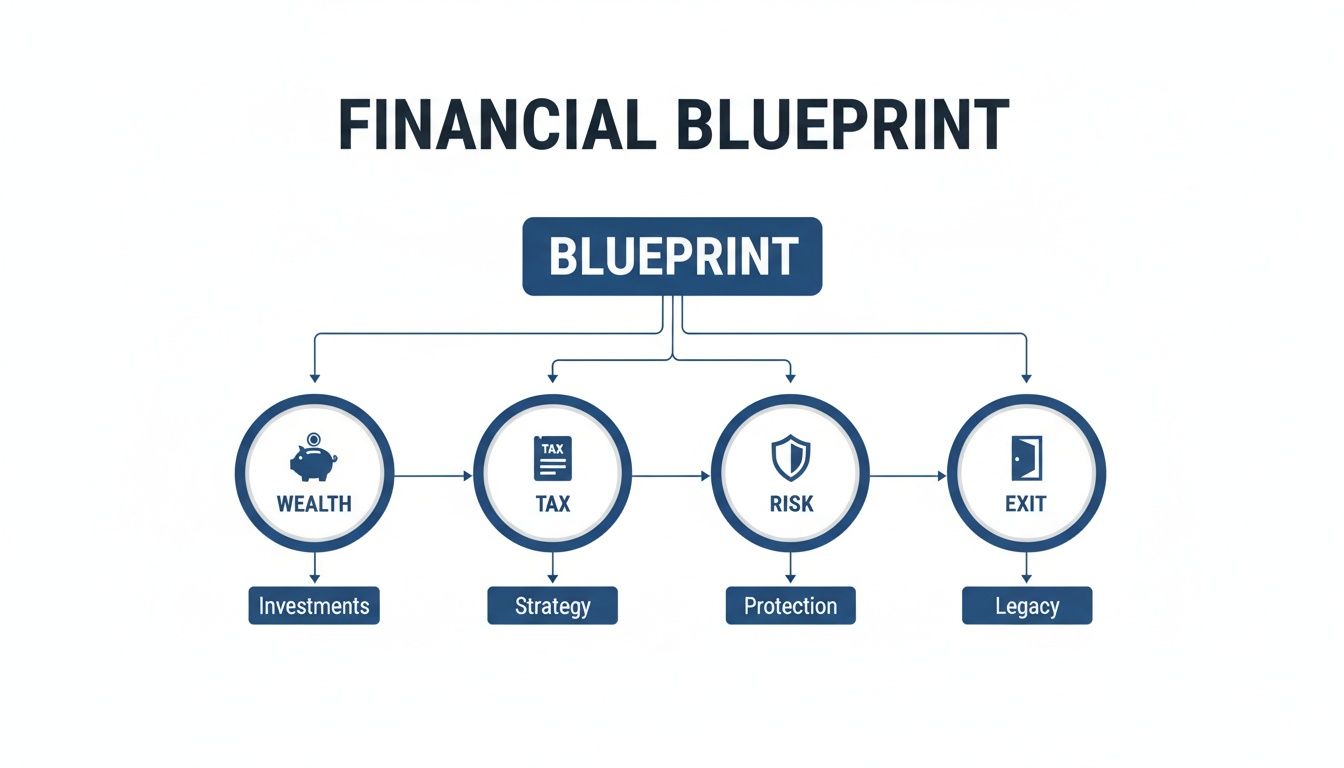

Why Financial Planning Is Your Business Blueprint

Many owners get stuck in a reactive loop. They see accounting as a look in the rearview mirror—a necessary task to track what's already happened. Financial planning, on the other hand, is your forward-looking GPS. It’s the strategic map that plots the best route, anticipates detours, and makes sure you have enough fuel to reach your ultimate destination: financial freedom.

Without this blueprint, your business is just a job, albeit a very demanding one. With it, your business becomes the single most powerful engine for building generational wealth.

The Four Pillars of a Solid Financial Blueprint

A truly effective financial plan stands on four core pillars. Each one is critical, and if one is weak, the entire structure is at risk.

-

Wealth Integration: This is all about connecting the dots. It’s how you strategically pay yourself, manage cash flow, and ensure the profits from your business are fueling your personal investment and retirement goals, not just sitting idle.

-

Tax Strategy: Let's move beyond just filing on time. This is about playing offense, not defense. It means proactively using smart strategies—like R&D credits or multi-state tax planning—to legally and ethically minimize what you send to the government.

-

Risk Management: You've worked too hard to see it all disappear. This pillar is your fortress. It uses essential tools like key person insurance and well-drafted buy-sell agreements to protect your business, your family, and your partners from the unexpected.

-

Exit & Legacy: Every owner leaves their business one day. The only question is whether it's on your terms. This is about planning your departure from day one to maximize your company's value and secure your financial future, whether you plan to sell to a third party or pass it to the next generation.

Here’s a look at how these four pillars come together to create a complete financial strategy.

As you can see, these elements aren't isolated; they're deeply interconnected. A decision in one area has a ripple effect across all the others. Without a plan that integrates wealth, tax, risk, and exit planning, you're just juggling numbers. With one, you're building a lasting legacy.

In this guide, we'll walk through the frameworks you need to master each pillar and turn your business into a finely tuned machine for achieving your biggest goals.

Integrating Business Goals with Personal Wealth

For most entrepreneurs, there’s a thick, imaginary wall between the company’s finances and their personal wealth. I see it all the time. But thinking this way is a huge missed opportunity. The most effective financial planning for business owners means tearing down that wall and creating one, unified financial ecosystem.

Start thinking of your business as more than just a source of income. It's the primary engine for your personal financial freedom. When your business goals are specifically designed to fuel your personal wealth, every dollar of profit starts working double-time for you. This approach transforms your company from a demanding job into a powerful asset-building machine.

This shift in perspective starts with a simple change: view every major business decision through a dual lens. Ask yourself, "How does this benefit the company?" and immediately follow it with, "How does this move my personal financial goals forward?" Without this integrated strategy, you run the very real risk of building a valuable business that never quite translates into personal prosperity.

The Art of Structuring Owner Compensation

How you pay yourself is one of the most powerful levers you can pull to merge your business and personal finances. This isn't just about taking a paycheck; it's a strategic game of tax efficiency and wealth acceleration. The sweet spot is finding the perfect balance between what you need to live on, what the business can comfortably afford, and what makes the most sense from a tax perspective.

Your compensation strategy typically has three main components:

- A Reasonable Salary: Taking a W-2 salary isn't just a good idea; it's often a legal requirement, especially if you're an S-Corp. The key is to set a salary that's defensible for your role and industry while strategically managing your payroll tax burden.

- Distributions or Dividends: This is how you take profits out of the business. These payments are often taxed at a lower rate than your regular salary, making them an incredibly efficient way to move wealth from the company's books to your personal accounts.

- Strategic Reinvestment: Don't forget the power of leaving money in the business. Reinvesting profits to fund growth, buy assets, or build up cash reserves directly fuels the company's value, which in turn, increases your own net worth.

It’s a sobering statistic, but for the average business owner, up to 80% of their net worth is tied up in their company. This really drives home why failing to effectively transfer that business value into personal wealth can be devastating when it comes time to think about retirement or leaving a legacy.

Aligning Business Growth with Personal Milestones

A classic trap for entrepreneurs is chasing business growth for its own sake. A much smarter approach is to align your company’s growth targets with your family’s long-term financial milestones. This means you actually start by mapping out your personal financial needs and then reverse-engineer a business plan to meet them.

Here’s a simple framework to follow:

- Define Your Personal Goals: Get specific. When do you want to be financially independent? What major life events are on the horizon, like sending kids to college or buying a vacation home, that will need funding?

- Calculate the Numbers: Sit down with an advisor and figure out the exact net worth and cash flow you'll need to make those goals a reality.

- Reverse-Engineer Your Business Targets: Now, you can set meaningful revenue, profitability, and valuation goals for your business—goals that are designed to produce the exact capital you need on your personal timeline.

Following this process gives all the hard work you pour into your business a clear and powerful purpose. Every new client you land, every operational efficiency you find, and every strategic investment you make becomes a deliberate step toward building the life you truly want for yourself and your family. This is what real financial planning for business owners is all about: closing the gap between professional success and personal fulfillment.

Mastering Advanced Tax and Cash Flow Strategies

Most business owners see cash flow as the company’s pulse and taxes as a painful but necessary cost. That’s true, but it’s also a limited view. Truly expert financial planning for business owners flips the script, turning these two items from reactive chores into powerful, proactive tools for building real wealth.

Think about it this way: basic budgeting is like driving your car while only looking at the few feet of road right in front of you. Dynamic cash flow forecasting, on the other hand, is like having a GPS with a satellite view—it shows you the entire route, warns you about traffic jams, and alerts you to bad weather ahead. This foresight lets you sidestep challenges and strategically time your investments to accelerate when others are hitting the brakes.

In the same way, advanced tax strategy isn't just about hunting for a few extra deductions in April. It's a year-round discipline that can function as one of your biggest profit centers. When you stop treating tax planning as a compliance headache and start seeing it as a strategic initiative, you can unlock capital, fuel growth, and seriously boost your bottom line.

Unlocking Profits Through Proactive Tax Planning

Your choice of business entity—whether you're an S-Corp, C-Corp, or LLC—is the bedrock of your tax strategy, but it’s only the beginning. The real magic happens when you layer on specialized strategies that fit your specific industry and operations. This is where a sharp advisor goes beyond simple tax prep to deliver a massive return on their fee.

These strategies can shave significant points off your effective tax rate, freeing up cash for reinvestment or building your personal net worth. For instance, sophisticated firms regularly use detailed R&D credit studies to slash effective tax rates by up to 30% for qualifying clients. In the real estate world, developers using 1031 exchanges deferred an estimated $2.7 billion in capital gains taxes in a single year. These aren't just accounting tricks; they are powerful asset shields, as you can see from these insights on financial services trends that show how strategic moves shape the market.

The biggest mistake owners make is waiting until the end of the year to think about taxes. Proactive tax planning is a 12-month process of making smart, informed decisions that compound over time.

Key Tax Strategies for Ambitious Owners

The tax code gets complicated fast, especially as your business expands. Operating across state lines or internationally opens up exciting new markets, but it also creates a minefield of tax complexity if you don't manage it properly.

Here are a few powerful strategies every owner should be discussing with their advisor:

-

R&D Tax Credits: So many founders think these credits are just for tech giants or scientists in lab coats. That's a myth. If your business is developing new products, improving internal processes, or building custom software (even for your own use), you could qualify. This is a dollar-for-dollar reduction of your tax bill—it’s pure gold.

-

Multi-State Tax (SALT): Have employees, customers, or even a single warehouse in more than one state? If so, you're tangled in a complex web of State and Local Tax (SALT) laws. A proactive SALT strategy makes sure you're compliant everywhere while optimizing your tax position to avoid overpayments and nasty penalties.

-

International Tax Structuring: For any business with global customers, suppliers, or operations, this is non-negotiable. Proper structuring helps you manage foreign tax credits, lower your global tax burden, and navigate the constantly shifting international regulations without getting tripped up.

This table gives a quick overview of these strategies and who they're best suited for.

Key Tax Strategies for Business Owners

| Strategy | Primary Benefit | Ideal Business Profile |

|---|---|---|

| R&D Tax Credits | Directly reduces federal and state income tax liability. | Businesses in tech, manufacturing, software, engineering, and architecture that invest in innovation. |

| SALT Planning | Minimizes tax burden across multiple jurisdictions and ensures compliance. | E-commerce companies, service businesses with remote employees, or any company with a physical presence in more than one state. |

| International Tax | Optimizes global effective tax rate and manages foreign compliance risks. | Companies with foreign subsidiaries, international sales channels, or overseas suppliers and contractors. |

These advanced approaches are crucial for protecting the wealth you work so hard to create.

From Reactive Budgeting to Dynamic Forecasting

If tax planning is about preserving capital, dynamic cash flow forecasting is about protecting it. A static annual budget is often obsolete by February. One late payment from a major client or one unexpected equipment failure can throw the whole thing off. A dynamic forecast, however, is a living model that flexes and adapts with your business in real time.

Getting this right involves a few key disciplines:

- Model Best-Case, Worst-Case, and Likely Scenarios: Don't just plan for the year you hope for. What happens if revenue suddenly drops 20%? What if you land that game-changing contract? Modeling these extremes prepares you to act decisively, not emotionally, when reality hits.

- Identify Key Drivers: You don't need to track a hundred metrics. Pinpoint the 2-3 variables that have the biggest impact on your cash flow. This could be your sales cycle length, customer acquisition cost, or inventory turnover. Focusing here simplifies everything and makes your model far more actionable.

- Set Trigger Points: Establish clear thresholds that automatically trigger a pre-planned response. For example: "If cash reserves dip below three months of operating expenses, we activate our line of credit and freeze all non-essential spending." This removes panic from the equation.

By mastering these advanced tax and cash flow strategies, you stop being a passenger in your own business and become the pilot. You gain the control and foresight needed to navigate any economic weather and steer your company toward its ultimate destination: sustained profitability and personal freedom.

5. Building Your Financial Fortress with Risk Management

You've worked hard to generate wealth. That's only half the battle. Now you have to protect it.

Too many business owners think a standard liability policy is enough, but that’s like building a castle and only guarding the front gate. A real financial fortress needs a multi-layered defense system. It has to protect your business, your personal assets, and your family from every threat you can—and can't—see coming.

We're talking about much more than just slip-and-fall accidents. Smart risk management is a core part of financial planning for business owners. It's about ensuring one bad day doesn't unravel years of hard work and making your business resilient enough to weather any storm.

Insuring Your Most Critical Assets

You insure your building and your equipment, but what about the people who make it all run? Losing a founder, a star salesperson, or that one technical genius who knows how everything really works can be absolutely catastrophic. This is where specialized insurance policies stop being an expense and become a non-negotiable part of your financial plan.

Think of these not as costs, but as investments in continuity. They provide the capital you need to get through a crisis without derailing the entire company.

-

Key Person Insurance: This is simply a life or disability policy that the company takes out on its most vital employees. If that person unexpectedly passes away or is disabled, the business gets a tax-free payout. That money can be used to recruit and train a replacement, cover the revenue gap, or just keep the lights on and reassure lenders that you’re stable.

-

Buy-Sell Agreements: I like to call this the "business pre-nup" for partners. Funded by life insurance, it spells out a clear, legally binding plan for what happens if a co-owner dies, becomes disabled, or just wants out. It ensures ownership transitions smoothly and prevents the kinds of devastating disputes or forced sales that can tear a business—and families—apart.

-

Directors & Officers (D&O) Coverage: This is a must-have if your company has a board of directors or corporate officers. D&O insurance shields their personal assets from lawsuits claiming wrongful acts or mismanagement. It's the backstop that allows your leadership team to make bold decisions without fear.

A well-structured buy-sell agreement is one of the single most important documents a multi-owner business can have. It takes emotion and uncertainty out of a crisis, providing a clear and fair path forward for everyone involved, including the owner's family.

Preparing for the Threats You Can't Insure

Let's be honest: you can't buy a policy for everything. An economic downturn, a disruptive new competitor, or a massive cybersecurity breach can pose a very real threat to your business. Preparing for these kinds of risks requires a different strategy—one built on financial foresight and strategic cash reserves.

This is where the dynamic cash flow modeling we talked about earlier becomes your best defense. By stress-testing your finances against worst-case scenarios ("What if sales drop 50% for six months?"), you can spot your biggest vulnerabilities before they become a five-alarm fire.

Here’s how you build that resilience against the uninsurable:

-

Build a "War Chest": This isn't your regular operating cash. It's a dedicated contingency fund. Your goal should be to set aside enough capital to cover 3-6 months of essential, bare-bones expenses with zero revenue coming in. This fund buys you time to think and make smart decisions during a crisis, not panicked ones.

-

Secure Lines of Credit (Before You Need Them): The worst time to ask for a loan is when you're desperate. Establish relationships and secure lines of credit with your bank when the business is healthy and your financials are strong. This gives you a lifeline you can tap into immediately when you need it most.

-

Fortify Your Cybersecurity: In today's world, a data breach is no longer a question of "if" but "when." Investing in robust security, continuous employee training, and having a clear incident response plan is every bit as critical as locking your office doors at night.

When you combine the right insurance with smart financial planning for the unexpected, you build a fortress that truly protects your life's work.

Planning Your Profitable Exit and Legacy

Every entrepreneur leaves their business eventually. That day is coming. The real question is, will you exit on your terms—as a planned, profitable finish line to your life's work—or will it be a rushed, reactive scramble that leaves money on the table? Engineering a great succession plan isn't something you tack on at the end; it's a long-term strategy you should weave into your financial planning for business owners right from the early days.

Think of it like planning a cross-country road trip. You wouldn't just jump in the car and start driving. You'd map your route and plan your stops. Your business exit is the ultimate destination, and without a clear roadmap, you'll almost certainly miss key opportunities or end up somewhere you never wanted to be.

Why Your Exit Strategy Needs a Head Start

Most owners I've worked with dramatically underestimate how long it takes to get a business ready for a smooth transition. The truth is, you need to start this process 5 to 10 years before you actually want to leave. This runway gives you enough time to methodically increase your company’s value, get your financials in perfect order, and structure the business to attract the best possible buyers or successors.

Waiting until you're burned out and ready to retire is a recipe for disaster. It almost always leads to a lower valuation, a much bigger tax bill, and a chaotic, stressful handover. The Exit Planning Institute has some sobering data: while 75% of owners plan to exit in the next decade, a staggering 70% to 80% of businesses listed for sale will never actually find a buyer. Proactive planning is what keeps you out of that statistic.

Choosing Your Path to the Finish Line

Your exit strategy has to line up with your personal, financial, and business goals. While every situation is unique, most exits fall into one of three buckets. Each one has its own financial implications and needs a very different kind of planning.

-

Third-Party Sale: This is often the route to the highest valuation. Selling to an outsider, like a strategic competitor or a private equity firm, demands pristine books, proof of growth, and a strong management team that can run the show without you.

-

Management or Employee Buyout (MBO/EBO): This is a fantastic option if you want to preserve the company’s culture and legacy. You're selling the business to your existing leadership team or employees. These deals can get complicated and often require creative financing, like seller financing, to make them work.

-

Family Succession: Passing the business to the next generation is the dream for many founders. But the stats show this is the hardest transition to pull off. It requires years of careful planning around estate taxes, figuring out a fair distribution of assets among heirs, and formally training the next leaders.

A common mistake is getting fixated on just one exit option. The best financial planning prepares the business so that multiple paths are on the table. This flexibility gives you leverage and control, allowing you to pivot if the market shifts or your personal circumstances change.

Structuring the Deal for Maximum Return

Once you have a potential path in mind, the focus shifts to structuring the deal to be as tax-efficient as possible. This is where a sharp financial advisor and tax pro earn their keep. How a deal is structured—as an asset sale versus a stock sale, for example—can have a massive impact on what you actually walk away with.

Proactive modeling is essential here. As asset and wealth management deals continue to rise, investors and family offices need to see clear financial forecasts to understand the value they're acquiring. Without it, a huge percentage of deals fail after the close because of poor integration, costing businesses billions every year. An advisor with multi-state and international tax experience can help you structure a deal that minimizes the tax bite, ensuring you keep more of your hard-earned money. You can explore a deeper analysis of these global banking and financial trends to see where the market is headed.

Ultimately, your exit is the final, critical chapter of your entrepreneurial story. By planning for it with the same intention and strategic foresight you used to build your company, you ensure your life's work pays off with a rewarding and financially secure future, cementing a legacy for yourself and your family.

Assembling Your Team of Financial Advisors

As a business owner, you’re the captain of the ship. Your expertise is in your industry, your people, and your customers. But the smartest captains know they can't also be the chief engineer, the navigator, and the lookout all at once. The same is true for your finances.

Truly effective financial planning for business owners means assembling a “personal board of directors”—a hand-picked team of advisors dedicated to protecting your interests and guiding you toward your long-term goals.

This isn’t just about hiring people to file paperwork. It's about surrounding yourself with strategic partners who offer proactive, forward-thinking advice. Trying to navigate the labyrinth of tax law, legal structures, and investment strategy on your own is a recipe for disaster. A coordinated team creates a powerful synergy, making sure every financial move is examined from all the right angles.

Your Core Financial Leadership Team

To build a truly resilient financial strategy, there are three roles you absolutely need to fill. Each professional brings a unique and critical perspective to the table. When they work together, they create a financial foundation that’s built to last.

-

The Certified Public Accountant (CPA): Think of your CPA as the historian and compliance officer. They look backward, ensuring your books are spotless, your tax returns are accurate, and you're playing by the rules. A top-tier CPA, like the professionals at a firm such as Blue Sage Tax & Accounting Inc., doesn't just record history—they use it to find patterns and inform smarter tax strategies for the future.

-

The Financial Advisor or Planner: While the CPA focuses on the past, your financial advisor is focused on the horizon. Their job is to map out the journey from where you are now to where you want to be. This involves everything from managing investments and planning for retirement to analyzing risk and weaving your eventual business exit into your personal wealth plan.

-

The Strategic Attorney: Your attorney is your chief risk officer on the legal front. They're the ones who protect your flank, handling everything from setting up the right business entity and reviewing contracts to protecting your intellectual property. Crucially, they also build the legal guardrails for your estate plan and draft the buy-sell agreements that protect you and your partners.

The magic happens when these three experts stop working in silos. Imagine your CPA spots a major tax-saving opportunity. Your financial advisor then structures an investment to fund it, and your attorney drafts the legal framework to make it all happen, seamlessly. That’s a winning strategy in action.

Finding True Strategic Partners

There's a world of difference between a service provider who just completes tasks and a true strategic partner who anticipates your needs. A provider is reactive; a partner is proactive.

When you're interviewing potential advisors, don't just ask about their fees. Ask them how they collaborate with other professionals. Ask for real-world examples of proactive strategies they've developed for business owners like you.

Your ideal team members should challenge your thinking and bring fresh ideas to the table—they should be educators, not just order-takers. Building this team is one of the single most important investments you will make in your business and your family's future. It gives you the collective wisdom you need to make the smartest possible decision, every single time.

Answering Your Key Questions

As we've walked through the roadmap, a few common questions always come up. Let's tackle them head-on, because the answers are crucial to putting these strategies into action.

How Often Should I Really Look at My Financial Plan?

Your formal, deep-dive review should happen at least once a year. Think of it as your business's annual physical—a chance to check all the vital signs and plan for the year ahead.

But that’s just the baseline. You should pull the plan out for a quick check-in whenever something significant happens. A major shift in revenue, a big equipment purchase on the horizon, hiring a new C-suite executive, or even a change in your personal goals—these are all triggers. For businesses growing quickly, I recommend a quarterly pulse-check to keep your forecasts sharp and your decisions grounded in reality.

What’s the Real Difference Between an Accountant and a Financial Advisor?

This is a fantastic question, and the distinction is critical. Your accountant is your financial historian. They look backward, expertly organizing your financial past to ensure your books are clean and your taxes are filed correctly and on time. They are essential for compliance.

A strategic financial advisor, on the other hand, is your financial architect. We look forward. We take the historical data from your accountant and use it to build a blueprint for the future. Our focus is on proactive strategies: How can we minimize your tax liability? How do we optimize cash flow to fuel growth? How do we structure everything to hit your long-term personal and business goals? We're in the business of shaping what's next, not just documenting what's already happened.

I'm Not Ready to Retire. When Should I Start Succession Planning?

The best time to start thinking about succession is 5 to 10 years before you even think you want to step away. I know it sounds early, but trust me, it's not.

Starting the succession process early is the single biggest factor that separates a lucrative, smooth exit from a fire sale. It gives you control over your legacy and ensures you’re not forced into a bad deal when you’re finally ready to move on.

That long runway gives you the time needed to properly groom a successor, get the business valuation as high as possible, and structure everything in the most tax-advantaged way. It allows you to align the sale with your personal retirement goals, avoiding the costly mistakes that come from rushing the process.

How Do I Decide Between Reinvesting in the Business and Paying Myself More?

Ah, the classic entrepreneur's dilemma. The answer lies in moving from gut-feel decisions to a clear, documented policy. This is precisely what a formal financial plan helps you create.

Here’s a simple framework we use to bring clarity to this balancing act:

- Map Out Business Needs: First, we identify exactly what capital the business needs to hit its growth targets, fund new projects, and maintain a solid cash cushion for unexpected bumps in the road.

- Define Your Personal Goals: Next, we get crystal clear on what you need to support your family, your lifestyle, and your own wealth-building outside of the business.

- Model the Scenarios: With those two pieces, we can model different compensation structures—like salary versus distributions—to find the sweet spot. The goal is to find the most tax-efficient way to fund the company's growth while consistently building your personal net worth.

This structured approach takes the emotion out of the equation, ensuring both your business and your personal finances are on a solid path forward.

At Blue Sage Tax & Accounting Inc., we help you answer these questions and build a proactive financial plan that integrates your business success with your personal wealth goals. Schedule a consultation with our team today to start building your blueprint for a secure future.