Depreciation recapture is one of those tax concepts that trips up a lot of real estate investors, but the idea behind it is actually pretty straightforward. Think of it as the IRS’s way of settling up with you at the time of sale.

Over the years you owned your property, you took depreciation deductions. These write-offs are a fantastic benefit, lowering your taxable income each year. But when you sell the property for a profit, the government essentially says, "Okay, time to pay tax on those benefits you've been enjoying." The gain you made that's equal to the depreciation you took gets "recaptured" and taxed. It’s not a penalty; it’s just paying back a tax deferral.

Understanding Depreciation Recapture in Simple Terms

Here’s a helpful way to think about it: Imagine the IRS gives you a small, interest-free loan every year you own an investment property. That "loan" is your annual depreciation deduction. It reduces your tax bill and puts more cash in your pocket. It’s a huge incentive that makes real estate investing so attractive.

But, as we all know, there's no such thing as a free lunch.

When you eventually sell that property for more than its depreciated value (its adjusted cost basis), the IRS wants that "loan" paid back. That repayment is depreciation recapture. It's the mechanism that makes sure the economic gain you realized over the life of the investment is taxed properly.

Why Recapture Is Not a Penalty

It's easy to get frustrated and see recapture as a last-minute tax hit, but it's really about fairness from the IRS's perspective. Those depreciation deductions you took were based on the idea that your property was slowly losing value due to wear and tear.

But if you turn around and sell it for a big profit, it proves the property didn't actually lose all the value you wrote off on paper. The recapture tax simply squares things up.

The core idea is simple: You can't get a tax break for an asset losing value and then also get a lower capital gains tax rate on the profit that resulted from those very same write-downs. Recapture closes this loop.

To break it down even further, here's a quick cheat sheet.

Depreciation Recapture At a Glance

This table simplifies the key components so you can see how they fit together.

| Concept | What It Means for You | The Tax Impact |

|---|---|---|

| Depreciation Deduction | An annual tax write-off for wear and tear, reducing your taxable income. | Lowers your ordinary income tax liability each year you own the property. |

| Adjusted Cost Basis | Your property's original cost basis, lowered by every depreciation deduction you take. | The lower your basis, the higher your potential gain when you sell. |

| Total Gain on Sale | The difference between your sale price and your lowered adjusted cost basis. | This is the total profit the IRS looks at for tax purposes. |

| Recaptured Gain | The portion of your total gain that's equal to the total depreciation you claimed. | This part is taxed at a special rate, capped at a maximum of 25% federally. |

| Capital Gain | The rest of the profit after accounting for the recaptured portion. | This amount is taxed at the more favorable long-term capital gains rates. |

Understanding these moving parts is the key to accurately projecting your tax liability when you decide to sell.

The Tax Impact and Key Numbers

For any investor selling a rental, the numbers matter. The IRS lets you depreciate residential rentals over 27.5 years and commercial properties over 39 years. Every single one of these annual deductions chips away at your property's adjusted basis.

When you sell, the portion of your gain that comes from all those deductions is taxed as ordinary income, but it gets a special federal cap—it won't be taxed higher than 25%. For more on the specifics, you can dig into the rental property tax rules published by BrightTax.

Calculating depreciation recapture in real estate boils down to a few core figures:

- Cost Basis: What you originally paid for the property, plus certain closing costs.

- Accumulated Depreciation: The grand total of all the depreciation you've claimed over the years.

- Adjusted Basis: Simply your cost basis minus the accumulated depreciation.

- Total Gain: Your final sale price minus that adjusted basis.

The magic happens when you separate your total gain. The amount equal to your accumulated depreciation is what gets hit with the recapture tax. Any profit left over is generally treated as a long-term capital gain, which usually comes with a much friendlier tax rate. Getting this distinction right is absolutely critical for smart tax planning.

Getting to Know the Key IRS Tax Rules

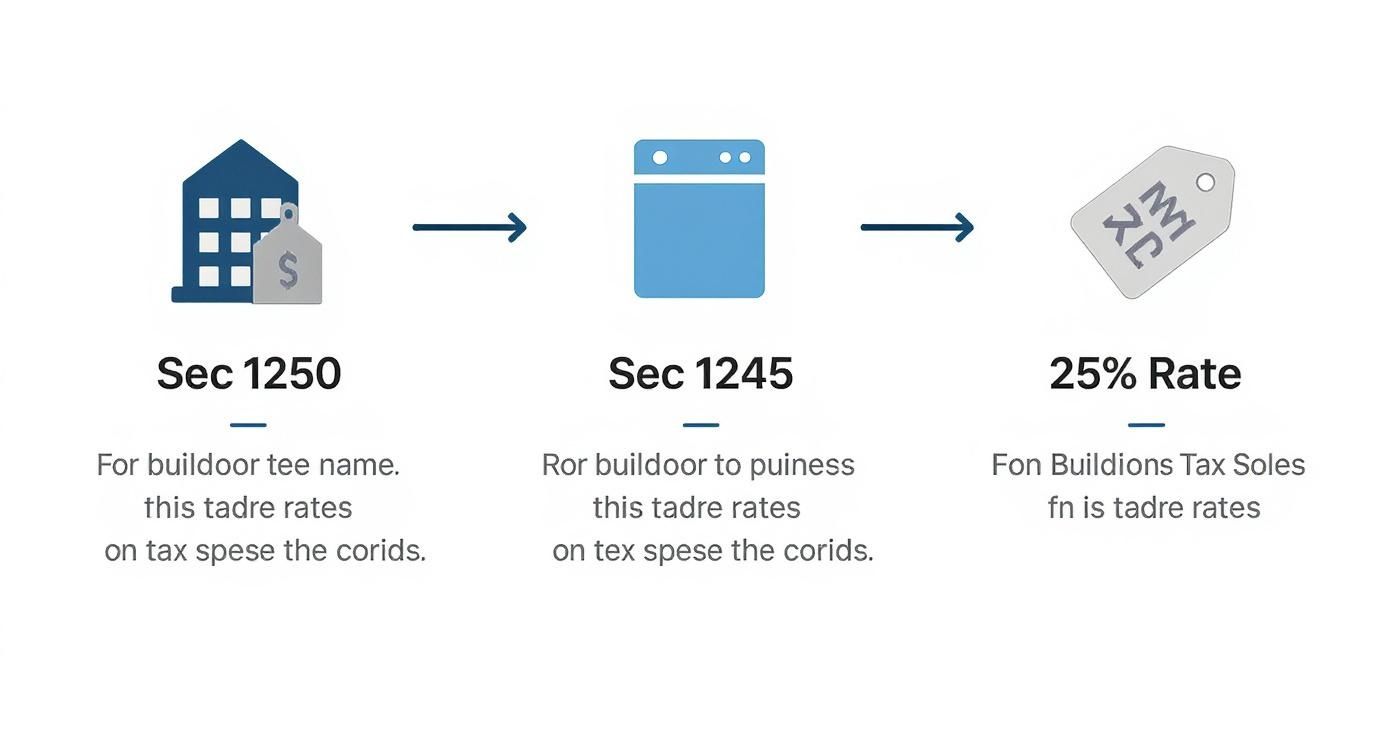

To really get a handle on depreciation recapture, you have to speak the IRS's language. The tax code is broken down into different sections, and for real estate investors, three names pop up again and again: Section 1250, Section 1245, and the all-important concept of "unrecaptured Section 1250 gain."

A simple way to think about it is to split your property into two parts: the physical building and all the "stuff" that makes it functional. The IRS taxes these two parts differently, and knowing which rules apply to which assets is the first step in managing your tax bill when you sell. This distinction isn't just academic—it directly changes how much you owe and the rate you pay.

Section 1250: The Rule for the Building

Section 1250 is the part of the tax code that deals with the building itself—the actual structure. Historically, its main purpose was to "recapture" any depreciation you claimed that was above and beyond the standard straight-line method. This was known as accelerated depreciation.

Now, if you bought your property after 1986, you're almost certainly using the straight-line method (where you deduct the same amount each year). So, the original intent of Section 1250 doesn't really apply to most modern investors. But its legacy created something incredibly important.

That something is the unrecaptured Section 1250 gain. This is simply the portion of your profit that equals the total straight-line depreciation you've taken over the years. The IRS taxes this specific slice of your gain not at your high ordinary income rate, but at a special, fixed maximum federal rate of 25%.

This is the big one for most real estate investors. Every dollar of depreciation you deducted against your ordinary income over the years gets "recaptured" when you sell and is taxed at that 25% rate. It’s a separate calculation from your regular capital gains.

Section 1245: The Rule for Everything Else

So, what about all the other things in and around your rental property? That's where Section 1245 comes in, and its rules are much tougher. This section covers all the tangible personal property you use for your investment.

What exactly is Section 1245 property? Think of things like:

- Appliances: Refrigerators, ovens, and dishwashers.

- Fixtures: Carpeting, blinds, and certain lighting.

- Equipment: Things like security systems or landscaping tools.

- Land Improvements: Fencing, sidewalks, and parking lots.

For these items, the rule is brutally simple. When you sell, any gain you realize that comes from the depreciation you took on these assets is taxed as ordinary income. There’s no special 25% rate here; you'll pay at your regular marginal tax rate, which could be as high as 37% at the federal level.

Putting It Together: Section 1250 vs. Section 1245

Seeing them side-by-side really clarifies how different the tax treatment is.

| Feature | Section 1250 Property (The Building) | Section 1245 Property (Appliances, Carpets) |

|---|---|---|

| Asset Type | Real property—the building and its structural components. | Personal property and land improvements. |

| Recapture Rule | Unrecaptured gain from straight-line depreciation is taxed. | All gain resulting from depreciation is recaptured. |

| Tax Rate | Maximum 25% federal rate. | Taxed as ordinary income (up to 37%). |

| Common Scenario | Affects the sale of any depreciated rental building. | Always a factor, but especially important if a cost segregation study was done. |

Back in the day, investors often used aggressive accelerated depreciation methods to get bigger tax deductions upfront. For example, a $1 million commercial building using a double-declining balance method could write off over 40% of its value in just the first few years. This felt great for cash flow initially, but it created a massive recapture tax bill down the road, with that extra depreciation being taxed as ordinary income. You can find a deeper dive into these kinds of tax strategies in research published by Vanderbilt Law Review.

By thinking of your property in these two buckets—building vs. personal property—you can start to see your future tax liability with much more clarity. The structure gets one set of rules, and everything else, from the stove to the sidewalk, gets a much harsher one. This is the level of detail you need for smart tax planning.

Calculating Depreciation Recapture Step by Step

Knowing the theory is one thing, but running the numbers is what really matters. The math behind depreciation recapture isn't rocket science, but it demands a methodical, step-by-step approach. Once you break it down, you can see your potential tax bill long before you ever list a property, which is crucial for making smart investment decisions.

Let's walk through a real-world example with a residential rental property. This will show you exactly how the IRS connects your purchase price, all those yearly depreciation deductions, and your final sale price to figure out your depreciation recapture tax.

Step 1: Determine Your Total Depreciation

First things first, you need to add up every single depreciation deduction you've ever claimed on the property. This total is your accumulated depreciation.

Imagine you bought a rental house ten years ago. For tax purposes, let's say the building itself (not the land) was valued at $275,000. The IRS says residential properties are depreciated over 27.5 years, so your annual deduction was calculated using the straight-line method:

- $275,000 / 27.5 years = $10,000 per year

You held the property for a decade, so the math is pretty simple:

- $10,000/year x 10 years = $100,000

This $100,000 is the magic number that drives the entire recapture calculation.

Step 2: Calculate Your Adjusted Basis

Next up is your adjusted basis. This is just your original cost for the property minus all the depreciation you've taken. It’s the property’s value on your books for tax purposes—think of it as the investment you have left to write off.

Let's say your original cost basis (purchase price plus buying costs) was $350,000. We'll use the accumulated depreciation from Step 1 to find your adjusted basis:

- Original Cost Basis: $350,000

- Less Accumulated Depreciation: ($100,000)

- Adjusted Basis: $250,000

See how that works? Every dollar of depreciation you claim lowers your basis, which in turn increases the taxable gain you'll have when you sell.

Step 3: Figure Out Your Total Gain on the Sale

Now, let's jump to the day you sell the property. You get a great offer and sell it for $500,000. Your total gain is simply the sale price minus your adjusted basis.

- Sale Price: $500,000

- Less Adjusted Basis: ($250,000)

- Total Gain: $250,000

This $250,000 is your total profit according to the IRS. But here's the critical part: not all of this gain is taxed in the same way. The next step involves splitting this profit into two different buckets: the recaptured portion and the capital gains portion.

The diagram below shows how the IRS treats the different parts of a real estate sale for tax purposes.

As the visual shows, the building (a Section 1250 asset) is handled differently from personal property like appliances (Section 1245 assets). The depreciation taken on the building is what gets "recaptured" at that special 25% tax rate.

Step 4: Pinpoint the Recaptured Amount

This is where it all comes together. The portion of your gain subject to depreciation recapture is the lesser of two numbers: your total gain or your accumulated depreciation.

Let's look at our example:

- Total Gain: $250,000

- Accumulated Depreciation: $100,000

Because your accumulated depreciation ($100,000) is the smaller number, that’s the amount that gets "recaptured" and taxed at the 25% rate.

The way to think about it is this: The IRS is basically saying, "You made a profit of $250,000. The first $100,000 of that profit is only on the books because we let you take depreciation deductions. We're now taxing that portion back at a specific rate."

The rest of your gain is treated as a standard long-term capital gain:

- Total Gain: $250,000

- Less Recaptured Depreciation: ($100,000)

- Long-Term Capital Gain: $150,000

Step 5: Calculate Your Final Tax Liability

Now for the final step: calculating the actual tax bill. For this example, we’ll assume the maximum federal tax rates apply.

- Tax on Depreciation Recapture:

- $100,000 (Unrecaptured Section 1250 Gain) x 25% = $25,000

- Tax on Capital Gains:

- $150,000 (Long-Term Capital Gain) x 20% = $30,000

Your total federal tax from the sale is $55,000 ($25,000 + $30,000). Keep in mind this doesn't include any state taxes or the 3.8% Net Investment Income Tax that might also apply.

To make this even clearer, the table below summarizes the calculation from start to finish.

Sample Recapture Calculation for a Residential Property

| Calculation Step | Example Value | Description |

|---|---|---|

| 1. Original Cost Basis | $350,000 | The property's purchase price plus initial buying costs. |

| 2. Accumulated Depreciation | $100,000 | Total depreciation deductions claimed over 10 years of ownership. |

| 3. Adjusted Basis | $250,000 | Original Basis minus Accumulated Depreciation ($350k – $100k). |

| 4. Sale Price | $500,000 | The price the property was sold for. |

| 5. Total Gain | $250,000 | Sale Price minus Adjusted Basis ($500k – $250k). |

| 6. Depreciation Recapture | $100,000 | The lesser of Total Gain ($250k) or Accumulated Depreciation ($100k). |

| 7. Recapture Tax (at 25%) | $25,000 | The recaptured amount taxed at the special 25% rate ($100k x 0.25). |

| 8. Capital Gain | $150,000 | The remaining portion of the gain ($250k Total Gain – $100k Recapture). |

| 9. Capital Gain Tax (at 20%) | $30,000 | The capital gain portion taxed at the long-term rate ($150k x 0.20). |

| Total Federal Tax Liability | $55,000 | The sum of the recapture tax and the capital gains tax. |

By walking through these steps, you can get a solid estimate of your tax outcome and start planning your sale or next investment with confidence.

How Recapture Works in Special Situations

Real estate deals are rarely simple. While a straightforward sale has clear rules, many common situations can completely change how depreciation recapture is handled. For any serious investor, understanding these nuances is key to managing your tax burden and avoiding nasty surprises.

https://www.youtube.com/embed/DmF5Qv8GVnY

From deferring taxes with a like-kind exchange to the surprising rules for installment sales, the approach to recapture can shift dramatically. These scenarios demand careful planning to sidestep unexpected tax bills.

The Power of a 1031 Exchange

The 1031 exchange, or "like-kind exchange," is one of the most powerful tools in a real estate investor's tax-planning arsenal. When you execute one correctly, you can defer not just your capital gains but also the depreciation recapture tax that you'd otherwise owe.

Think of it as swapping one investment for another without cashing out. Instead of selling and paying taxes, you roll your entire gain—and its associated tax liability—into a new, similar property. From the IRS's perspective, you've simply continued your investment, not ended it.

But here’s the crucial part: a 1031 exchange defers the tax, it doesn't eliminate it. The recapture liability doesn't just vanish; it attaches itself to the new property. When you eventually sell that replacement property in a normal taxable sale, the deferred recapture from the original property comes due, right alongside any new recapture you’ve accumulated.

A cardinal rule for a successful 1031 is that the replacement property must be of equal or greater value. If you take cash out of the deal or receive other non-like-kind property (what's known as "boot"), that portion is immediately taxable. And the IRS dictates that recapture tax is recognized first, before capital gains.

The Installment Sale Trap

An installment sale, where the buyer pays you over several years, seems like a smart way to spread out your tax hit. It makes intuitive sense—you get the money over time, so you should pay the tax over time. While that’s generally true for the capital gains portion, a nasty surprise is waiting when it comes to depreciation recapture.

The IRS has a very specific—and very harsh—rule here.

All depreciation recapture must be recognized and paid in the year of the sale, no matter how little cash you actually receive. This can create a massive, immediate tax bill even when your bank account has only seen a small down payment.

Here’s a quick example of how painful this can be:

- You sell a property with $100,000 of accumulated depreciation.

- The deal is an installment sale over 10 years, and you only receive a $20,000 payment in Year 1.

- The IRS requires you to report the entire $100,000 of depreciation recapture as income in Year 1.

- This triggers a tax liability of up to $25,000 (25% of $100,000), even though you only collected $20,000 in cash.

As you can see, this rule can create a serious cash-flow crunch. You absolutely must factor in this upfront tax hit when structuring any seller-financed deal.

Inherited Properties and the "Step-Up in Basis"

Here's some good news. The rules for inherited property offer a powerful benefit that can wipe out depreciation recapture entirely. When an heir receives a real estate asset, its cost basis is "stepped up" to its fair market value on the date of the original owner's death.

This step-up in basis effectively wipes the tax slate clean.

Since the heir's new basis is the current market value, all the depreciation claimed by the previous owner is forgiven. If the heir turns around and sells the property for that same fair market value, there's no taxable gain to report—which means no depreciation recapture and no capital gains tax.

This makes holding onto appreciating real estate until death a cornerstone of estate planning for many families. It allows a lifetime of accumulated wealth to pass to the next generation without the huge tax bill that a sale would have triggered.

Proven Strategies to Defer Your Recapture Tax

While depreciation recapture is a certainty when you sell a profitable investment property, the timing of that tax bill is anything but. Experienced investors know better than to just accept the hit. They plan for it. Managing this liability is about looking beyond a single sale and focusing on your long-term wealth strategy.

Fortunately, you have several powerful tools at your disposal to control when—and if—you pay recapture tax. By putting these strategies into play, you can keep your capital working for you, grow your portfolio, and avoid sending a premature check to the IRS.

Master the 1031 Exchange

Hands down, the most powerful tool in the real estate investor's tax-deferral toolkit is the Section 1031 like-kind exchange. This incredible provision in the tax code lets you sell an investment property and roll all the proceeds into a new, similar one without triggering an immediate tax bill. Both your capital gains and your depreciation recapture get pushed down the road.

The key word here, however, is deferred. It's not eliminated. The recapture tax liability you built up on the first property simply attaches itself to the new one. When you eventually sell that replacement property in a standard taxable sale, the recapture from the original property finally comes due, along with any new recapture.

A successful 1031 exchange demands precision and strict adherence to IRS rules. You have a tight window: you must identify a potential replacement property within 45 days of the sale and close on it within 180 days. To defer all taxes, the new property's value and any associated debt must be equal to or greater than the property you sold.

Hold Property for the Long Term

Sometimes the most brilliant strategy is the simplest one: just don't sell. A recapture event is never triggered as long as you hold onto the property. This aligns perfectly with a long-term buy-and-hold strategy, letting the property appreciate and generate rental income year after year.

This approach becomes even more powerful when integrated into your estate plan. When you pass away, your heirs inherit the property at what's called a stepped-up basis—its fair market value at the time of your death. This one move effectively erases every dollar of depreciation you ever claimed. Your heirs can then sell the property for its new, higher value and pay zero capital gains and zero depreciation recapture. It's a complete tax reset.

Strategically Time Your Sale

If a 1031 exchange isn't in the cards and you're set on selling, timing is everything. Your recapture tax rate is directly linked to your ordinary income tax bracket. Selling in a year when your other income is lower can make a huge difference in the final tax bill.

Consider these timing tactics:

- Sell in a lower-income year: If you're planning to retire, shifting careers, or expecting a temporary dip in business income, that might be the perfect moment to pull the trigger on a sale.

- Harvest losses to offset gains: Do you have capital losses from other investments, like a bad run in the stock market? You can use those losses to offset the capital gain portion of your real estate sale, which can dramatically reduce or even eliminate the overall tax liability.

Ultimately, managing depreciation recapture comes down to proactive, forward-thinking planning. Whether you're chain-linking 1031 exchanges to build a real estate empire or holding assets to pass on to the next generation, these strategies put you in control. A good tax advisor can be invaluable here, helping you map out the best path for your specific financial goals.

Common Questions About Depreciation Recapture

When you get into the weeds of real estate taxes, depreciation recapture can be a real head-scratcher. Let's clear up some of the most common questions investors ask when trying to apply these rules to their own properties.

Can I Avoid Recapture by Not Claiming Depreciation?

This is a classic question, but the answer is a firm no. The IRS has a rule they call the "allowed or allowable" standard.

What this means is they don't care if you actually took the depreciation deduction on your tax returns. They will tax you on the amount you could have taken. Because of this, you're always better off claiming the depreciation you're entitled to each year.

Does Recapture Apply to My Primary Home?

For the most part, no. You can't depreciate your primary residence, so there's nothing to recapture when you sell it.

But there's a big exception: if you've ever used part of your home for business. This could be a home office, a studio, or a room you rented out. If you claimed depreciation on that portion of your home, you will have to recapture that specific amount when you sell.

The line is drawn between personal and business use. Recapture only ever applies to the part of the property you depreciated.

What’s the Difference Between Capital Gains and Recapture?

It’s easy to mix these up, but they are two totally different taxes calculated on the profit from your sale.

Capital gains tax applies to the property's appreciation—the increase in its market value from when you bought it to when you sold it. The federal tax rates for long-term gains are 0%, 15%, or 20%.

Depreciation recapture is a separate tax on the part of your gain that comes from the depreciation deductions you took, which lowered your cost basis. For real estate, this is taxed at a special maximum rate of 25%.

Is Depreciation Recapture Considered Ordinary Income?

It depends on what you're selling.

When we're talking about the building itself (what the tax code calls Section 1250 property), the recapture is taxed at that special 25% maximum rate, not at your regular income tax rate.

However, if you've depreciated personal property within the building—things like appliances, carpeting, or fixtures (Section 1245 property)—that portion of the gain is recaptured as ordinary income. This means it gets taxed at your marginal rate, which can be significantly higher.

Getting depreciation recapture right takes more than just understanding the rules; it requires smart, forward-looking planning. At Blue Sage Tax & Accounting Inc., we specialize in proactive tax strategies that help real estate investors minimize their liabilities and keep more of their returns. Learn more about our advisory services to see how we can help.