When it comes to your primary residence, the answer is refreshingly simple: condo association fees are not tax deductible. The IRS puts these payments in the same bucket as other personal living expenses, like your utility bills or basic home repairs.

But the story completely changes if you use your property to make money. Suddenly, those same fees can transform into valuable deductions that lower your tax bill.

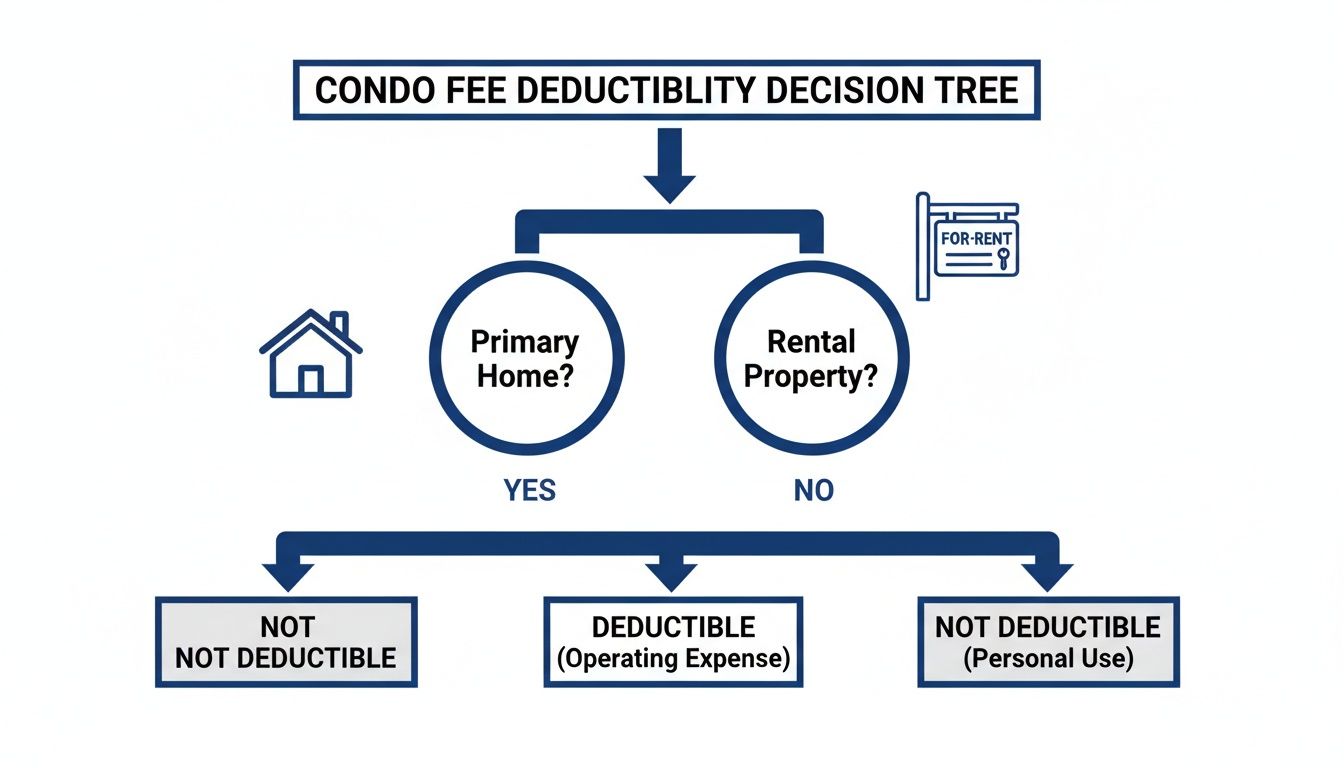

When Are Condo Association Fees Tax Deductible?

The question of whether you can deduct your condo or HOA fees comes down to one thing: how you use the property. Think of it like a car. If you're just driving to the grocery store, you can't deduct your gas and maintenance. But if you're a delivery driver using that same car for work, those costs become business expenses.

Your condo works the same way. For most people who live in their unit, the monthly fees are just part of the cost of enjoying their home and the shared amenities—the pool, the gym, the landscaped grounds. They're personal expenses, plain and simple.

However, the moment your condo starts acting like a business, the rules flip. This opens up significant tax-saving opportunities for two main groups:

- Real Estate Investors: If you rent out your condo, the fees are a direct cost of running your rental business.

- Business Owners & Self-Employed: If you use a portion of your condo exclusively as a home office, a percentage of the fees can be deducted.

This decision tree gives you a quick visual breakdown of the basic rules.

As you can see, it all boils down to how the property is being used.

To make it even clearer, here’s a quick summary table.

Condo Fee Deductibility at a Glance

| Property Use | Are Fees Deductible? | How It Works |

|---|---|---|

| Primary Residence | No | Fees are considered a non-deductible personal living expense. |

| Rental Property | Yes | Fees are 100% deductible as an ordinary and necessary business expense against rental income. |

| Home Office | Partially | A portion of the fees based on the square footage of your office is deductible as a business expense. |

This table provides a high-level overview, but the distinction between personal and business use is where the real strategy lies.

The Critical Distinction: Personal vs. Business Use

In the U.S., there are over 369,000 homeowners associations, and for the vast majority of their members, the fees they collect offer no tax break. You can find more HOA statistics on ThisOldHouse.com to see just how common this is.

The game-changer is when you treat your property as an investment. For landlords and real estate investors, 100% of the association fees for a rental unit become deductible. They are considered an "ordinary and necessary" expense of running a rental business and are used to directly offset the income your property generates.

The core takeaway is this: The IRS draws a hard line between personal living costs and the legitimate costs of doing business. It's your property's use—not its type—that determines whether your condo association fees are tax deductible.

Grasping this fundamental principle is the first step toward building a smart tax strategy for your real estate. For investors in high-cost areas like NYC, where common charges can be substantial, getting this right is absolutely essential for maximizing your returns.

When you own a rental property, the game changes completely. Suddenly, your condo isn't just a home; it's a business in the eyes of the IRS. This shift is crucial because it transforms your monthly association fees from a personal expense into a legitimate business cost.

For real estate investors, this is fantastic news. It means that 100% of the condo association fees you pay for a property that is purely a rental are tax deductible. These aren't minor write-offs; they are significant expenses that directly chip away at your taxable rental income, which you'll report on Schedule E (Supplemental Income and Loss).

Think about it this way: if you owned a storefront, you’d deduct rent, electricity, and security without a second thought. As a landlord, your condo is your "store," and the association fees cover essential services like maintaining the lobby, landscaping the grounds, or paying the building's security staff—all necessary for keeping your tenants happy and your investment sound.

A Real-World Example in NYC

Let’s put some real numbers to this. Imagine you own a rental condo in a hot Queens neighborhood. The numbers might look something like this:

- Monthly Condo Fee: $1,200

- Annual Condo Fees: $1,200 x 12 = $14,400

- Annual Rental Income: $48,000

By claiming the full $14,400 as a business expense, you directly lower your taxable rental income by that amount. In a high-tax city like New York, that single deduction can easily save you thousands of dollars in taxes every year. It’s a powerful tool for maximizing your return.

What About Mixed-Use Properties and Vacation Homes?

Things get a little more complex when a property pulls double duty—part personal getaway, part rental unit. This is a classic scenario for vacation homes. You can't just deduct 100% of the condo fees anymore. Instead, you have to prorate the expense.

The calculation is straightforward: you can only deduct the portion of your expenses that directly corresponds to the time the property was rented out.

The Proration Principle: If you rent your property for 75% of the year and use it personally for the other 25%, you can only deduct 75% of your condo fees and other related expenses.

This rule is a cornerstone of tax planning for property owners everywhere, from NYC to vacation hotspots around the globe. If you rent your place for nine months out of the year, you deduct 75% of your fees. Simple as that. You can find more details about how rental use impacts your tax deductions on AvenueLawFirm.com.

The Critical 14-Day Rule

Before you start prorating, you need to know about a specific IRS guideline known as the "14-day rule" (found in IRC Section 280A). It's a tripwire that can change everything.

Here’s how it works:

- Rented for less than 15 days: If you rent out your home for 14 days or fewer all year, you get a break. You don't have to report any of that rental income to the IRS. The catch? You can't deduct any rental expenses, either, including your condo fees.

- Too much personal use: Your deductions can be limited if your personal use of the property is more than 14 days or more than 10% of the total days it was rented out, whichever is greater. You can still deduct prorated expenses, but only up to the amount of rental income you brought in. In this scenario, you can’t claim a rental loss to offset your other income.

For anyone with a mixed-use property, meticulous record-keeping is your best friend. You absolutely must keep a log of every single day the property was rented versus used personally. This is the evidence you’ll need to correctly prorate your condo fees and other expenses, ensuring you claim every dollar you're entitled to without getting into trouble with the IRS.

Using the Home Office Deduction to Your Advantage

So you're not a landlord, but you run your business out of your condo. Good news: there's another path to deducting those association fees. The home office deduction is a powerful tool for self-employed individuals who carve out a piece of their home exclusively for work.

If you’re a freelancer, consultant, or solo entrepreneur, this is for you. The IRS lets you write off a portion of your household expenses, and yes, that includes your monthly condo fees. The logic is simple: those fees maintain the building, provide security, and keep the lights on in the common areas—all things that indirectly support the space where you conduct your business. It's an indirect business cost, and you can claim your share.

Let's be clear, though. This deduction is specifically for the self-employed—those who file a Schedule C (Profit or Loss from Business) with their tax return. If you're a W-2 employee working from home, you're generally out of luck. The Tax Cuts and Jobs Act did away with this benefit for employees, even if you work remotely full-time.

Meeting the IRS Standard for a Home Office

Before you start crunching numbers, your workspace has to pass two strict tests from the IRS. They are not flexible on this.

- Exclusive Use: Your office space must be used only for your business. That desk in the corner of the guest room that doubles as a crafting table? That won't fly. It needs to be a dedicated, distinct area used for nothing but your work.

- Regular Use: You have to use the space consistently for your business. Dabbling in it once or twice a month isn't enough. It needs to be your primary place of business or a spot where you regularly meet with clients or customers.

These rules are the foundation of the deduction. If you don't meet them, you can't claim it. Period.

How to Calculate Your Deduction

Once you've confirmed your office qualifies, the math is pretty straightforward. The most common way to figure out your deduction is by using the square footage of your space.

The formula looks like this:

(Square Footage of Your Home Office / Total Square Footage of Your Condo) x Total Condo Association Fees = Your Deductible Amount

This little calculation gives you your business use percentage. You’ll apply this same percentage to other shared home expenses, too, like your utility bills, homeowners insurance, and general repairs.

Let's put it into practice. Say you're a freelance graphic designer living in a 1,200-square-foot condo in NYC. You’ve converted a spare bedroom that’s 150 square feet into your exclusive design studio.

- Step 1: Find your business use percentage.

150 sq. ft. (office) ÷ 1,200 sq. ft. (total) = 12.5% - Step 2: Add up your annual condo fees.

Your monthly fee is $900, so that’s $10,800 for the year. - Step 3: Calculate your deduction.

12.5% of $10,800 = $1,350

In this scenario, you get to deduct $1,350 of your condo fees as a business expense. This gets calculated on Form 8829, Expenses for Business Use of Your Home, and the final number flows over to your Schedule C.

The Absolute Need for Meticulous Records

The home office deduction is a known audit trigger for the IRS, which means your record-keeping has to be flawless. Think of it as your insurance policy. If they come knocking, you need to be ready to prove every penny.

Essential Records for an Audit-Proof Claim:

- A Floor Plan: A simple sketch of your condo's layout showing the dimensions of each room and clearly marking the office space.

- Photos or Videos: Dated pictures or even a quick video walkthrough that provides visual proof of the exclusive business setup.

- Condo Association Statements: A complete file of every monthly or quarterly statement showing what you were charged.

- Proof of Payment: Canceled checks, bank records, or credit card statements that show you actually paid the fees.

For self-employed real estate investors or entrepreneurs using part of their NYC condo as a home office, this deduction is a fundamental tax strategy. As the IRS details on Form 8829, it’s all about being self-employed and justifying the claim based on square footage. If you want to dig deeper, you can learn more about these HOA fee tax rules from Experian. Building an unassailable record is where professional guidance can really pay off, helping you claim what you're owed without raising any red flags.

Understanding Special Assessments and Capital Improvements

Not every check you write to your condo association is created equal, at least not in the eyes of the IRS. While your regular monthly fees cover the predictable costs of running the building—and are often deductible for a rental property—the rules change when the association hits you with a special assessment.

A special assessment is a one-off charge, separate from your usual dues, meant to fund a significant, often expensive, project. Grasping the distinction is key, because it completely changes when and how you can claim a tax benefit. It’s not an immediate expense; it's an investment in your property, and the tax code treats it that way.

The Key Difference: Repairs vs. Improvements

The IRS draws a bright line between two kinds of projects funded by these special assessments: repairs and capital improvements. This single distinction determines if you get a deduction now or later.

-

Repairs: Think of these as upkeep. They keep the property in good working order but don't add to its value or extend its life. Patching a leaky common-area roof or fixing the building's main garage door are classic examples. For a rental property, an assessment for these types of repairs is treated just like a regular condo fee—you can deduct it in the year you pay it.

-

Capital Improvements: These are the big-ticket items. These projects substantially add to the property's value, prolong its useful life, or adapt it for a new use. We're talking about replacing the entire building's roof, installing a brand-new elevator system, or a complete overhaul of the windows.

Most major special assessments fall squarely into this second category. When that happens, the rules for deduction flip entirely. You can't write off the cost as an immediate business expense. Instead, you have to capitalize it.

What It Means to Capitalize an Expense

"Capitalizing" an expense sounds like accounting jargon, but the idea is actually quite simple. Instead of subtracting the cost from your rental income this year, you add it to your property's cost basis.

Your property's cost basis is its official value for tax purposes. It begins with the price you paid for the condo, plus certain closing costs. When you pay for a capital improvement, you are officially increasing that baseline value.

A capital improvement assessment isn't a lost deduction; it's a deferred one. By adding the cost to your basis, you're setting yourself up for a significant tax break when you eventually sell the property.

This is a powerful long-term strategy. A higher cost basis means a smaller taxable profit (or capital gain) when you sell, which can translate into thousands of dollars in tax savings down the road. For any serious real estate investor, this is a fundamental part of managing tax liability over the life of an asset.

A Practical Example of Capitalization

Let's walk through a real-world scenario. Say you own a rental condo in NYC that you originally bought for $800,000. That's your starting cost basis.

A few years into your ownership, the condo board decides to replace all the building’s windows to boost energy efficiency. Your share of this special assessment is a one-time payment of $20,000.

Here’s the correct way to handle it:

- Don't Deduct It Now: You cannot claim the $20,000 as a rental expense on your Schedule E for the current tax year. It’s not an operating cost.

- Add It to Your Basis: Instead, you add that $20,000 directly to your property’s cost basis.

- Original Basis: $800,000

- Capital Improvement: +$20,000

- New Adjusted Basis: $820,000

Now, let's fast-forward a few years. You decide to sell the condo and get an offer for $1,100,000. Because you capitalized that assessment, your taxable gain has been reduced by $20,000. This directly lowers the final capital gains tax you'll owe, turning a hefty cash outlay from years ago into a valuable tax shield today.

Navigating NYC Co-op Rules and State Tax Nuances

While condos are a huge part of the real estate market, New York City has a unique beast that plays by a different set of rules: the cooperative apartment, or co-op. For co-op owners, the question "are condo association fees tax deductible?" gets a more complex—and often more rewarding—answer. It all comes down to a fundamental difference in how ownership is structured.

When you buy a condo, you're buying real property, plain and simple. But when you buy a co-op, you're technically buying shares in a corporation that owns the building. Those shares then grant you a proprietary lease for your apartment. This distinction is everything. Your monthly "maintenance fee" isn't just for the gym and doorman; it includes your proportional share of the entire building's underlying mortgage interest and property taxes.

This structure unlocks a significant tax advantage that condo owners just don't get.

Unlocking the Co-op Shareholder Deduction

Because co-op shareholders are effectively paying the building's core property expenses through their maintenance fees, the IRS lets them deduct their portion of these costs. In a high-tax environment like NYC, this is a powerful benefit.

Every year, the co-op's board sends its shareholders a letter detailing exactly how much of their total annual maintenance payments went toward two key deductible items:

- Real Estate Taxes: Your slice of the property tax bill for the entire building.

- Mortgage Interest: Your share of the interest paid on the building's underlying mortgage.

This information is typically summarized on IRS Form 1098, which the co-op provides. Think of this form as your golden ticket—it has the precise figures you need to claim these deductions on Schedule A of your personal tax return.

For a co-op owner, a large part of the monthly maintenance fee isn't just a personal expense; it's a pass-through of deductible homeownership costs. This can make the true cost of ownership lower than it appears on the surface.

A Co-op Deduction Example

Let's break down how this works with a real-world example. Imagine you're a co-op shareholder in Manhattan paying $2,500 a month in maintenance fees. That adds up to $30,000 for the year.

At tax time, you get a letter from your co-op board stating that 45% of the maintenance fees collected were used to pay the building's property taxes and mortgage interest.

- Your Calculation: $30,000 (Total Annual Maintenance) x 45% = $13,500

This $13,500 is the amount you can potentially claim as an itemized deduction. This directly reduces your taxable income, offering substantial savings that a condo owner in a similar unit wouldn't get from their common charges alone.

State and Local Tax (SALT) Cap Considerations

While the co-op deduction is a major perk, NYC residents also have to contend with the federal State and Local Tax (SALT) deduction cap. The Tax Cuts and Jobs Act (TCJA) limited the amount of state and local taxes that taxpayers can deduct on their federal returns to $10,000 per household, per year.

This cap is an all-in-one limit that includes:

- State and city income taxes

- Property taxes (including your co-op's pass-through amount)

- Sales taxes (if you choose to deduct them instead of income taxes)

For many high-income New Yorkers, their state and city income taxes alone easily push them over the $10,000 limit. This means that while your co-op's property tax portion is technically deductible, you might not see any additional federal tax benefit from it if you've already hit the SALT cap.

However, the story doesn't end there. These deductions can still be valuable on your New York State tax return, which has its own set of rules. Navigating this interplay between federal caps and state benefits requires careful tax planning, which is a core service we provide at Blue Sage Tax & Accounting Inc.

How to Build an Audit-Proof Record for Your Deductions

Knowing you can deduct your condo fees is one thing; proving it to the IRS is another. When it comes to tax deductions, the burden of proof is always on you. A meticulous, well-organized file isn't just about good habits—it's your front-line defense in case of an audit.

Think of it this way: you’re building a case file for your property's finances. Every statement, receipt, and log is a piece of evidence that justifies the numbers you put on your tax return. This isn't just about avoiding a stressful audit; it's about confidently managing your investments and maximizing your legitimate tax benefits year after year.

The Essential Documentation Checklist

Your goal is to have a file so clear and complete that it tells the entire story of your expenses without you having to say a word. If an auditor comes knocking, you want to be able to hand over a folder that leaves no room for questions.

At a minimum, every property owner needs to keep these core documents:

- Condo Association Statements: Don't throw these away. Keep every single monthly or quarterly statement you receive. They're the official record of what you were charged.

- Proof of Payment: This is absolutely critical. You need to show the money actually left your account. Canceled checks, bank statements highlighting the withdrawal, or credit card receipts all work perfectly.

- Special Assessment Invoices: For those one-off charges, hold onto the specific invoice from the association. Make sure it explains exactly what the money was for—a new roof, lobby renovation, or emergency plumbing repairs. This detail is what separates a deductible repair from a non-deductible capital improvement.

Strong record-keeping turns tax time from a frantic scramble into a calm, strategic process. An organized file doesn't just protect you from an audit; it gives you a clearer picture of your property's financial health, empowering smarter decisions all year long.

Documentation for Specific Scenarios

Sometimes, the basics aren't enough. If you’re claiming a home office or prorating expenses for a rental, you’ll need more detailed records to back up your specific calculations.

For Home Office Deductions:

- A Measured Floor Plan: You don't need a professional blueprint. A simple, hand-drawn sketch of your condo's layout showing the total square footage and the specific measurements of your office space is essential. This is how you'll prove your business-use percentage.

- Dated Photographs: A few pictures of your dedicated workspace can be powerful visual proof. They show an auditor that the space is set up and used exclusively as an office, not as a guest room with a desk in the corner.

For Mixed-Use (Rental/Personal) Properties:

- Usage Logs: This is non-negotiable. Keep a simple calendar or log tracking every single day the property was rented out versus used personally. This log is the foundation for prorating all your expenses correctly.

When you assemble these documents throughout the year, you’re doing more than just prepping for taxes. You're operating like a savvy investor, building a professional-grade financial management system for your property. That level of detail and organization is what provides true peace of mind and protects the long-term value of your real estate portfolio.

Frequently Asked Questions About Condo Fee Deductions

When it comes to condo fee deductions, the devil is always in the details, especially when your property serves more than one purpose. Let's tackle some of the most common questions we hear from clients to clear up the confusion.

Can I Deduct Condo Fees If I Work from Home for an Employer?

Unfortunately, no. If you’re a W-2 employee, even a fully remote one, you can't deduct a portion of your condo fees for a home office. This popular deduction was a casualty of the Tax Cuts and Jobs Act (TCJA) back in 2017, which eliminated the miscellaneous itemized deduction for home office expenses.

To deduct a portion of your condo fees, you absolutely must be self-employed—think freelancer, independent contractor, or small business owner. The deduction is only available to those who file a Schedule C and meet the IRS’s strict “exclusive and regular use” test for their workspace.

What if I Use My Rental Condo for a Personal Vacation?

This is a classic scenario that requires careful tracking. If you use your rental property for personal getaways, you have to be mindful of the proration rules. The IRS gets picky if your personal use exceeds the greater of 14 days or 10% of the total days it was rented out at a fair price.

When you cross that line, your deductions get limited. You'll need to meticulously allocate all your expenses, including the condo fees, between the days it was a rental and the days it was your personal retreat. Only the rental portion is deductible. Keeping a detailed log of personal vs. rental days isn't just good practice; it's essential for a defensible tax return.

The bottom line is that you can only deduct expenses for the time the property is actively operating as a rental. Meticulous tracking is the only way to correctly separate business from personal use.

How Do I Treat an Assessment for Repairs vs. Improvements?

The difference here is critical and has a big impact on your taxes. Think of it this way: a special assessment for a simple repair, like patching a leaky roof in a common area, is a current expense. For a rental property, you can deduct that cost in the year you pay it, just like any other maintenance fee.

But an assessment for a capital improvement—something that adds significant value or extends the life of the property, like a brand-new roof or a modern elevator system—is handled differently. You can't deduct it immediately. Instead, you "capitalize" it, meaning you add the cost to your property's basis. This doesn't give you an immediate break, but it will reduce your taxable capital gains when you eventually sell the property.

Where Do I Report Deductible Condo Fees on My Tax Return?

Knowing where to put the numbers is just as important as knowing what you can deduct. The right form depends entirely on how you're using the property.

- For a Rental Property: Your deductible condo association fees will be listed as an operating expense on Schedule E (Supplemental Income and Loss).

- For a Home Office: You’ll first calculate the deductible portion of your fees on Form 8829 (Expenses for Business Use of Your Home). The final number from that form then carries over to your Schedule C (Profit or Loss from Business).

Getting these details right is the foundation of a solid financial strategy for your real estate. At Blue Sage Tax & Accounting Inc., we help NYC investors make sense of these complex rules to stay compliant and maximize their returns. If you're ready for proactive planning, contact us to see how we can help.