Let's get right to the heart of the matter: there isn't a single, straightforward tax rate on S corp distributions. How a distribution is taxed depends entirely on a crucial figure known as your shareholder basis. Generally, you can take distributions tax-free up to the amount of your basis. After that, they become taxable as capital gains.

The Pass-Through Advantage of an S Corp

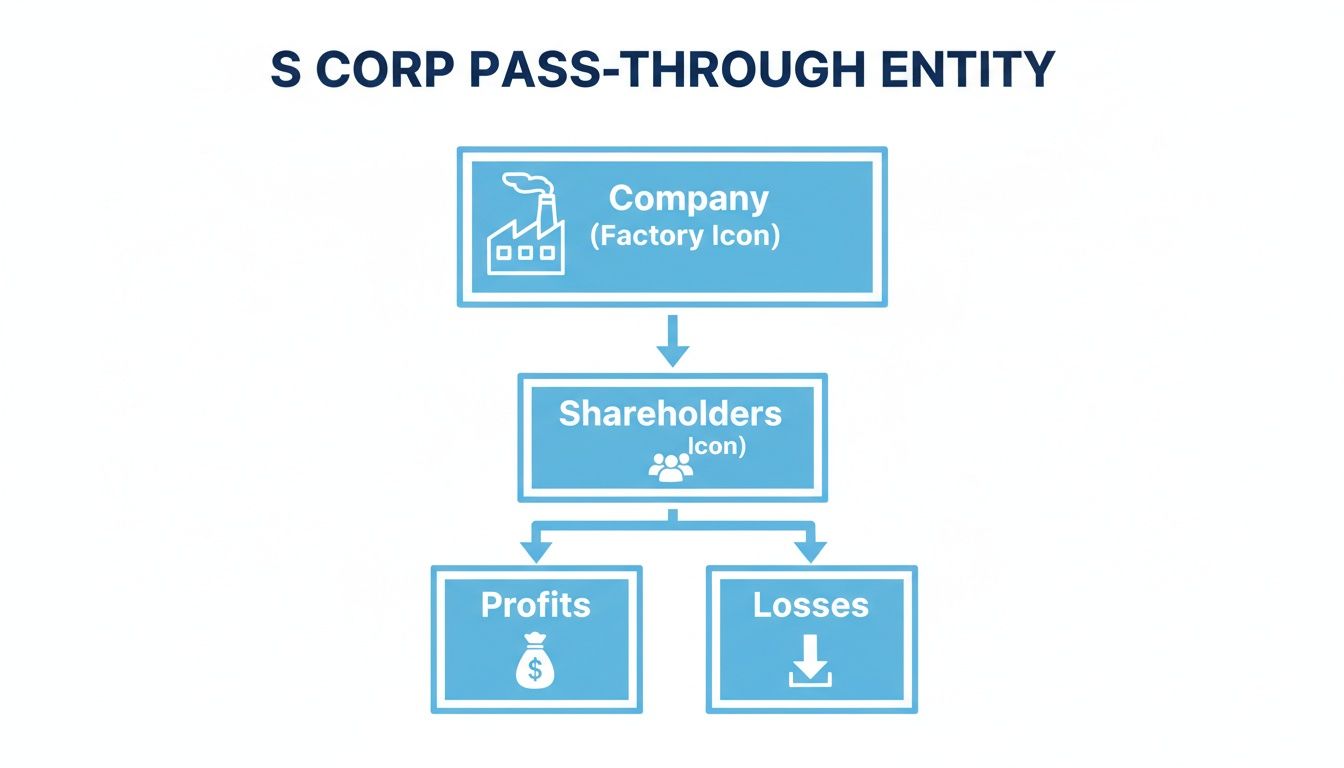

Before we can talk about distributions, we have to understand the fundamental benefit of an S corp: its pass-through taxation. This is what sets it apart from a traditional C corporation. A C corp gets hit with "double taxation"—the company pays corporate income tax, and then shareholders pay tax again on the dividends they receive.

S corps sidestep this entirely. The business itself pays no federal income tax. Instead, all profits and losses are "passed through" to the shareholders' personal tax returns. This is a critical point: you pay tax on your share of the company's net income every year, whether you actually take the cash out or not.

How Your Basis Dictates the Tax Outcome

Think of your shareholder basis as a running account of your after-tax investment in the company. It begins with the cash and property you first put in and then gets adjusted up or down each year based on profits, losses, and additional contributions.

When you take a distribution, its tax treatment falls into one of three distinct tiers. Which tier it falls into is determined solely by how the distribution amount compares to your basis at that moment.

One of the most common and costly mistakes S corp owners make is assuming all cash they pull from the business is tax-free. The reality is that the taxability of every single dollar is determined by your shareholder basis. Without meticulous basis tracking, you could inadvertently turn what should be a tax-free return of your own money into a surprise taxable event.

This tiered system is precisely why there's no simple answer to the "what's the tax rate" question. The rate could be 0%, 15%, 20%, or in some less common situations, it could even be taxed at your top ordinary income rate. Nailing down these tiers is the key to smart tax planning.

To make this crystal clear, here’s a quick breakdown of how any distribution you take from your S corp will be taxed.

How Your S Corp Distribution Is Taxed at a Glance

| Distribution Type | Tax Treatment | Effective Tax Rate |

|---|---|---|

| Distribution Up to Your Stock Basis | Return of Capital | 0% (Tax-Free) |

| Distribution Exceeding Stock Basis | Long-Term Capital Gain | 0%, 15%, or 20% (depending on your income) |

| Distribution from Former C Corp E&P | Ordinary Dividend | Ordinary Income Tax Rates (up to 37%) |

As you can see, keeping your distributions within your basis is the goal for tax-free withdrawals. Once you go beyond that, you start paying capital gains tax, and in the specific case of a company that used to be a C corp, you could even face dividend treatment.

How S Corp Pass-Through Taxation Actually Works

To really get a handle on the tax rate on S corp distributions, you first have to understand the engine driving the whole thing: pass-through taxation. A traditional C corporation pays its own corporate tax, but an S corp is different. It acts more like a conduit, passing its financial results directly to the owners.

Think of your S corp as a river. All the profits and losses it generates during the year flow right past any corporate-level tax dam. Instead, they flow directly into the personal "reservoirs" of the shareholders.

This flow gets documented on a critical tax form called a Schedule K-1. Every shareholder gets a K-1 that lays out their exact share of the company's income, deductions, and credits. You take those numbers and report them on your personal Form 1040.

The Reality of Phantom Income

Here’s a crucial point that catches many business owners by surprise: you are taxed on the company's profits whether you actually take a distribution or not. This is often called "phantom income" because you can end up with a tax bill for money that's still sitting in the company’s bank account.

Let's imagine you own a growing NYC consulting firm set up as an S corp. The business has a fantastic year, netting $200,000 in profit. You decide to be prudent and reinvest all of it back into the company to hire new staff and upgrade your tech. Even though you didn't pocket a dime, you’ll get a K-1 showing $200,000 of income, and you'll owe personal income tax on it.

It feels a bit strange at first, but this is a fundamental part of how S corps work. The good news is that this taxable income isn't just gone—it directly increases your shareholder basis, which is key for taking tax-free distributions down the road.

A Historical Game Changer for Entrepreneurs

The pass-through concept wasn't just some minor tax code adjustment; it was a massive shift designed to help small businesses escape the dreaded double taxation of C corporations. When Subchapter S was created back in 1958, the tax world was a very different place. The top corporate tax rate was a hefty 52%, and the top individual rate was an almost unbelievable 91%.

A dividend paid from a C corp to a high-income owner could face a combined effective federal tax rate nearing 96%. The S corp election completely flipped this script, allowing profits to be taxed just once at the shareholder's personal rate.

This change threw a lifeline to entrepreneurs, letting them keep more of their hard-earned capital for growth and personal wealth. Understanding this history helps explain why the S corp became—and still is—such a go-to choice for closely held businesses. You can explore more about the history of S corps and how they truly changed the game.

Tying It All Together

So, what does this all have to do with distributions? It’s simple, really. The income that passes through to you on the K-1—and gets taxed on your personal return—also increases your shareholder basis. Think of it as "pre-paying" the tax on those company earnings.

When you later take a distribution, you’re just withdrawing money that the tax system has already accounted for. This is precisely why distributions up to your basis are treated as a tax-free return of your investment. They aren't new income; they're simply the cash payout of profits you've already paid tax on.

Understanding and Tracking Your Shareholder Basis

When it comes to the tax rate on S corp distributions, your shareholder basis is the single most important number you need to know. Think of it as your after-tax investment in the business—a running tally of your skin in the game. Getting this calculation right isn't just a bookkeeping chore; it's what separates a tax-free withdrawal from a taxable one.

At its heart, your basis calculation is a straightforward formula. You start with your initial investment, and then it moves up and down each year. Company profits and any new capital you put in will increase your basis. On the flip side, distributions and company losses will decrease it. It’s a living number that changes with the fortunes of your business.

This diagram illustrates how S corp profits and losses "pass through" the company directly to the shareholders, which is the core mechanism that impacts your basis.

This visual is a great reminder that the S corp itself doesn't pay income tax. Instead, all of its financial results—good and bad—flow directly to you as the owner.

Your Initial Stock Basis

Your starting basis is simply what you put in to get your stock. In many cases, this is clean and simple, like a $100,000 cash investment to launch the company.

Things get a little trickier if you contributed property instead of cash. Your initial basis isn't the property's current market value. Instead, it’s the adjusted basis of that property. For example, say you contributed equipment you originally bought for $50,000 and have since taken $10,000 in depreciation. Its tax basis is now $40,000. Even if that equipment is currently worth $60,000, your starting stock basis is just $40,000. This is a critical distinction that often trips people up.

How Yearly Adjustments Change Your Basis

Once you've set your starting point, you have to adjust your basis every single year. Meticulous tracking here is completely non-negotiable, as each year's activity directly impacts the next.

Your basis goes up by:

- Your share of the S corp’s income. This includes both taxable and tax-exempt income that flows through to you on your Schedule K-1.

- Additional capital contributions. Any new cash or property you inject into the business increases your basis.

Your basis goes down (but never below zero) by:

- Distributions you receive. These are treated as a return of your investment, so they logically reduce your basis.

- Your share of the S corp’s losses and deductions. Just like profits build up your basis, losses will chip away at it.

Keeping an accurate, up-to-date basis schedule is your best defense against a surprise tax bill. It's the official scorecard that proves your distributions are a tax-free return of your own capital, not taxable income.

A Practical Example of Basis in Action

Let’s walk through a real-world scenario with Sarah, a real estate developer in NYC, to see how basis works over time.

Year 1: Sarah launches her S corp with a $250,000 cash investment. Her initial basis is $250,000. The business breaks even for the year.

Year 2: The market is hot. The company generates a profit, and Sarah's share of the net income is $150,000. She decides to take a $50,000 distribution.

- Start of Year 2 Basis: $250,000

- Add: Net Income $150,000

- Subtract: Distribution ($50,000)

- End of Year 2 Basis: $350,000

That $50,000 distribution is completely tax-free because she had more than enough basis to cover it.

Year 3: The market cools significantly. The S corp has a net loss, and Sarah's share is ($75,000). She also takes a large $300,000 distribution for a down payment on a personal property.

- Start of Year 3 Basis: $350,000

- Subtract: Net Loss ($75,000)

- Basis Before Distribution: $275,000

Now, let's look at that $300,000 distribution. It gets split into two parts:

- The first $275,000 is a tax-free return of basis. This withdrawal reduces her basis all the way down to $0.

- The remaining $25,000 is more than her basis. This excess amount is taxed as a long-term capital gain.

This multi-year example makes it clear that the tax rate on S corp distributions isn't a single, fixed number; it's all about where the distribution lands in this "waterfall" of basis. Sarah's distribution was taxed at both 0% (for the return of basis) and the capital gains rate (for the excess). This powerful flexibility is why the S corp has been so popular for decades. In fact, IRS data shows S corps became the most common corporate entity choice back in 1997, mainly because they avoid the dreaded double taxation of C corps. You can read more S corporation statistics on IRS.gov.

For high-net-worth business owners in New York, this structure means that while their pass-through profits can be taxed at steep combined federal, state, and city rates—potentially over 51.5%—the distributions themselves can often be pulled out of the company completely tax-free.

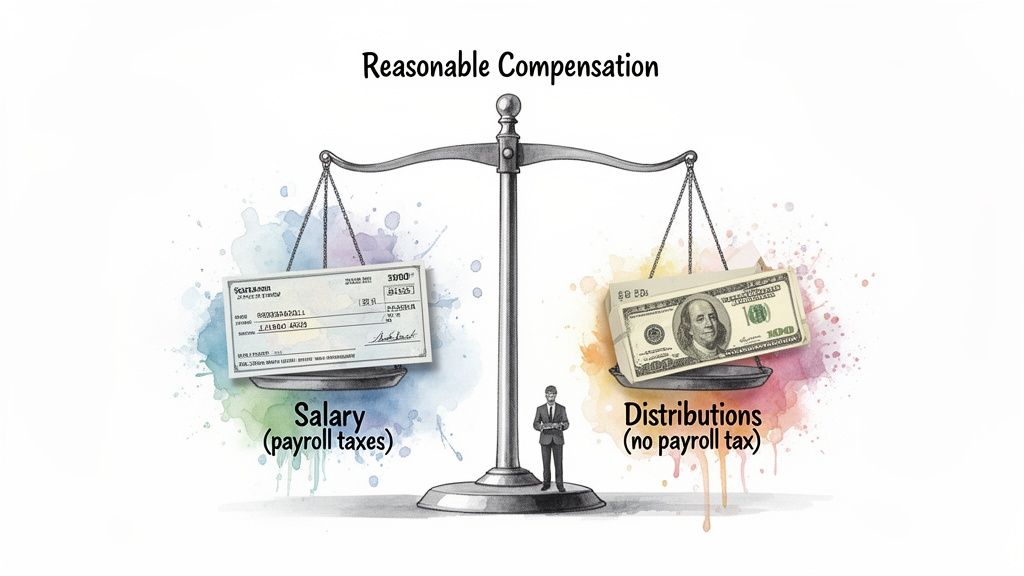

The Critical Role of Reasonable Compensation

While your shareholder basis is the key to unlocking tax-free distributions, there’s another piece of the puzzle that’s just as important: reasonable compensation. If there's one area where the IRS pays close attention to S corporations, this is it.

The whole appeal of S corp distributions is that they aren't hit with self-employment or payroll taxes (Social Security and Medicare). That’s a huge deal. For 2024, those taxes add up to 15.3% on the first $168,600 of earnings and 2.9% on anything above that. This creates a tempting opportunity for shareholder-employees to pay themselves a tiny salary and take the rest as a distribution, sidestepping a hefty tax bill.

Of course, the IRS is wise to this. They mandate that any shareholder who's actively working in the business must be paid a reasonable salary before a single dollar is taken as a distribution. That salary runs through payroll, gets hit with all the usual taxes, and is reported on a W-2, just like any other employee.

So, What's Considered "Reasonable"?

The word "reasonable" can feel frustratingly subjective, but the IRS isn't trying to trick you. They simply expect you to be paid what someone else would be paid for doing the same job. You can't just pull a number out of thin air; it has to be a figure you can defend if they ask.

To land on a defensible salary, you need to weigh a few key factors:

- Your Role and Responsibilities: What do you actually do? Are you the CEO, the lead technician, the head of sales, or all three? Your pay should line up with the market rate for those roles.

- Time and Effort: How much are you working? A full-time founder running the show should have a much different salary than a shareholder who only consults a few hours a week.

- Experience and Training: Your background, skills, and years in the trenches add real value. That expertise should be reflected in your compensation.

- Market Benchmarks: What are similar companies in your city or region paying for comparable work? Data from the Bureau of Labor Statistics or private compensation reports can give you a solid starting point.

- Company Performance: The S corp's profitability and financial health are also part of the equation. A thriving business can support a higher salary than one that's just scraping by.

The IRS isn’t looking for you to nail a perfect, scientifically calculated number. They’re looking for a good-faith effort to pay yourself what your work is genuinely worth. The best thing you can do is document your research and the factors you considered—that's your strongest defense in an audit.

Trying to game the system here is a major red flag. If the IRS determines your salary is unreasonably low, they have the power to reclassify your distributions as wages. Suddenly, you’re on the hook for back payroll taxes, plus penalties and interest. It’s a costly mistake you don’t want to make.

The Financial Impact of Getting It Right

When you dial in the right balance between salary and distributions, the tax savings can be substantial. Let’s walk through a quick example to see it in action.

Imagine Alex, an architect in NYC who is the sole shareholder of his S corp. The business brings in $300,000 in net profit before he pays himself.

Scenario 1: All Profit as Salary

If Alex treats the entire $300,000 as a W-2 salary, his payroll tax bill would be steep:

- Social Security Tax (12.4% on the first $168,600): $20,906

- Medicare Tax (2.9% on $300,000): $8,700

- Total Payroll Tax: $29,606

(Note: This is simplified, as the cost is split between employer and employee, but the total hit to the business is the same.)

Scenario 2: Optimized Salary and Distribution

After researching the market, Alex determines a reasonable salary for his role and experience is $120,000. He pays himself that amount and takes the remaining $180,000 as a distribution.

- Social Security Tax (12.4% on $120,000): $14,880

- Medicare Tax (2.9% on $120,000): $3,480

- Total Payroll Tax: $18,360

The $180,000 distribution is completely free of payroll taxes. Just by structuring his compensation correctly, Alex saves $11,246 in a single year. That’s cash he can reinvest, put toward retirement, or use for personal goals—all while staying completely compliant. This is the real power of the S corp when you know how to use it.

Navigating State and NYC Taxes for S Corps

Getting the federal rules for S corp distributions down is a huge hurdle. But if you're a business owner in New York, and especially New York City, there’s a whole other labyrinth of state and local taxes to navigate. One of the costliest assumptions I see people make is thinking a tax-free distribution on their federal return is automatically clear on their New York return.

That's a definite "no."

The pass-through concept holds true, but that’s precisely the point. The S corp's income flows to your federal Form 1040, and it also flows straight to your New York State (NYS) and New York City (NYC) personal income tax returns. So even if you take a $100,000 distribution that counts as a tax-free return of basis for federal purposes, the $100,000 of profit that created that basis was fully taxed by NYS and NYC in the year you earned it.

This means the profits funding your distributions face some of the steepest state and local tax rates in the entire country. For high earners, you could be looking at a combined hit of up to 10.9% for New York State plus another 3.876% for New York City.

New York’s Entity-Level S Corp Taxes

Another surprise for many is that New York State doesn't give S corporations a completely free pass at the entity level, unlike the federal government. Most S corps doing business in NYS have to pay a Fixed Dollar Minimum (FDM) tax. It’s an annual tax calculated based on the corporation's gross receipts, and it can be anywhere from $25 to $4,500.

If your business operates within the five boroughs, the New York City General Corporation Tax (GCT) might also come into play. The S corp election does grant an exemption from the main GCT, but some S corps can still get hit with a capital-based tax or an alternative minimum tax, depending on their financial makeup. These are just part of the local compliance puzzle.

A Strategic Workaround: The PTET Election

One of the most important developments in state tax planning for S corps is the Pass-Through Entity Tax (PTET). This is a voluntary tax that the S corporation can elect to pay on its income for its shareholders.

At first glance, this sounds crazy. Why would you volunteer to pay a tax? It all comes down to the federal State and Local Tax (SALT) deduction cap, which famously limits individuals to deducting a mere $10,000 of state and local taxes on their personal returns.

The PTET is an elegant way around that cap:

- The S corporation pays the state income tax directly.

- This payment is treated as an ordinary business expense, fully deductible on the S corp's federal tax return. It completely sidesteps the shareholder's personal $10,000 SALT limit.

- The shareholders then get a dollar-for-dollar credit on their personal NYS income tax returns for the PTET paid on their behalf.

By electing PTET, the S corporation essentially converts a non-deductible personal state tax payment into a fully deductible business expense at the entity level. For high-income shareholders in NYC who are already maxing out their SALT deduction, this strategy can result in significant federal tax savings.

This election has become a powerful tool for lowering the overall tax bite for S corp owners in high-tax states like New York. It really drives home the point that you have to look at federal, state, and city rules together to understand the true tax rate on S corp distributions.

For a deeper dive into the specifics, you can learn about the NYC PTET on the city's official government website.

Taking S Corp Strategy to the Next Level

Once you’ve got a firm handle on the basics—like calculating your basis and paying yourself a reasonable salary—you can start thinking more strategically. This is where you move past just staying compliant and begin using your S corp as a powerful tool for building wealth, growing the business, and even planning for the next generation.

One of the most effective strategies involves timing your distributions. Let's say you know your personal income will be lower next year. You might decide to take a distribution that you know will exceed your basis, intentionally triggering a capital gain. Why? Because you can recognize that gain in a year where you’ll pay tax at a lower rate, maybe 15% instead of the higher 20% bracket. It's about playing the long game.

Reinvest or Take the Cash? The Classic S Corp Dilemma

Every business owner grapples with this: how much profit do I pull out, and how much do I leave in the company to grow? There’s no magic formula here. It’s a constant tug-of-war between fueling future expansion and rewarding the shareholders (yourself) today.

Leaving profits in the company can be a fantastic way to fund growth without taking on debt or giving up equity. Those retained earnings boost your stock basis, which sets you up for larger tax-free distributions down the road when the business is more established. Think of it as deferred gratification—a strategy that can massively increase your company's long-term value.

Deciding whether to distribute or retain earnings is a defining moment for any business owner. A distribution puts cash in your pocket right now. Retained earnings are an investment in the company’s future. The right call depends entirely on your business's need for capital and your personal financial situation.

When an S Corp Isn't the Right Fit

As popular as the S corp is, it's not a one-size-fits-all solution. It can be a particularly tough fit for companies that need to pour every last dollar back into the business and don’t plan on making distributions for a long time. This is where the classic S corp vs. C corp debate comes roaring back, especially when tax laws change.

A fantastic analysis from The Tax Adviser really drives this point home. When the Tax Cuts and Jobs Act (TCJA) dropped the C corp rate to a flat 21%, the whole calculation changed for many business owners.

If you're in a high-tax state like New York, your S corp profits can get hit with a combined tax rate north of 51%. Suddenly, that flat 21% C corp rate for retained earnings looks pretty appealing. For businesses that plan to distribute over 40% of their income, a C corp can sometimes create better after-tax cash flow by retaining earnings at that lower rate and paying out salaries. This is a perfect example of why you need sharp, ongoing advice to make sure your business structure is still working for you as your goals and the tax code evolve.

Common Questions About S Corp Distribution Taxes

Even after you get a handle on the concepts of basis and reasonable compensation, real-world situations can still be tricky. Let's tackle some of the most frequent questions we hear from S corp owners about their distributions.

Think of this as a quick-reference guide to clarify those lingering points of confusion and reinforce what we've already covered.

Can I Take a Distribution if My S Corp Has a Loss?

The short answer is yes, but you have to tread very carefully here. When your business takes a loss for the year, that loss eats into your shareholder basis. Any distribution you take on top of that reduces it even further.

Here's the trap: if the one-two punch of the business loss and your distribution wipes out your basis, any amount you take beyond that is treated as a taxable capital gain. This is why tracking your basis with your accountant is absolutely critical in a loss year—it helps you avoid a nasty, unexpected tax bill.

What Is the Difference Between a Distribution and a Dividend?

In the S corp world, a "distribution" is generally a tax-free return of your own money—your investment, or basis. A "dividend," on the other hand, is a term we usually associate with C corporations. It’s a taxable payment made from the C corp's after-tax profits.

The lines can get blurry, though, if your S corp has a past life as a C corp.

If an S corporation still has leftover "earnings and profits" from its C corp days, any distributions you take after your basis hits zero can be treated as taxable dividends. This is a crucial distinction, as these are often taxed at less favorable ordinary income rates.

Do I Have to Take Distributions Equally with Other Shareholders?

Yes. This is a hard-and-fast rule with no exceptions. S corporations are built on the "one class of stock" requirement, which means all distributions must be made pro-rata. In plain English, that means you pay out based on each shareholder's ownership percentage.

For example, if you own 70% and your partner owns 30%, you must take 70% of the total distribution, and they must take 30%. Deviating from this is a huge compliance mistake that can actually get your S corp status terminated by the IRS, creating a cascade of painful tax problems.

How Does the QBI Deduction Affect My Distributions?

This is a common point of confusion, but the Qualified Business Income (QBI) deduction has no direct effect on how your distributions are taxed.

The QBI deduction (also known as Section 199A) is something you calculate on your personal tax return. It’s based on the net profit that passes through from the S corp to you, and its job is to lower your overall taxable income. It doesn't change the nature of the money you pull out of the business. A distribution is still either a tax-free return of basis or a taxable capital gain, completely separate from your QBI calculation.

Navigating the complexities of S corp taxation requires proactive and precise guidance. At Blue Sage Tax & Accounting Inc., we partner with closely held businesses in New York City to ensure every financial move is optimized for tax efficiency and long-term growth. Schedule a consultation with our experts today.