Filing an extension for your LLC buys you more time to get the paperwork right, but the deadlines can be tricky. For most multi-member LLCs, you're looking at a September 15 extended deadline. If you're a single-member LLC or your LLC is taxed as a C corporation, the date to circle on your calendar is October 15.

That extension gives you a full six months to file the return, but it does not give you more time to pay what you owe. That’s the single most important thing to remember.

Understanding Your LLC Tax Extension Due Dates

Think of a tax extension as a grace period for your paperwork, not your payment. It’s a common and costly mistake to believe that filing an extension pushes back your tax payment deadline. It doesn't.

Your original tax payment due date is set in stone. The extension just gives you a later date to submit the final, detailed report to the IRS.

How Your Tax Classification Sets the Calendar

The exact extended due date for your LLC boils down to one thing: its tax classification. While an LLC offers legal flexibility, for tax purposes, the IRS sees it as something else entirely—a sole proprietorship, a partnership, an S corp, or a C corp. That choice dictates your filing calendar.

The most critical takeaway is this: an extension to file is not an extension to pay. The IRS expects you to make a good-faith estimated payment of your tax liability by the original due date. Without that payment, your extension can be invalidated, and you’ll be hit with failure-to-pay penalties.

For most LLCs, the math is simple: the extension adds six months to your original deadline.

- An LLC taxed as a partnership files Form 1065. The original due date is March 15, so filing Form 7004 pushes that deadline to September 15.

- An LLC taxed as an S corporation also has a March 15 deadline, which extends to September 15.

- For an LLC treated as a C corporation, the original due date is typically April 15. An extension moves that to October 15.

LLC Tax Return Due Dates at a Glance (Calendar Year)

To simplify things, here's a quick summary of the key federal deadlines for LLCs that operate on a standard calendar year.

| LLC Tax Classification | Federal Tax Form | Original Due Date | Extended Due Date |

|---|---|---|---|

| Sole Proprietorship (Single-Member LLC) | Form 1040, Schedule C | April 15 | October 15 |

| Partnership (Multi-Member LLC) | Form 1065 | March 15 | September 15 |

| S Corporation (LLC Election) | Form 1120-S | March 15 | September 15 |

| C Corporation (LLC Election) | Form 1120 | April 15 | October 15 |

Getting these dates straight is the first step to a smooth tax season. Knowing exactly how your LLC is classified is the key to hitting your deadlines and keeping penalties at bay.

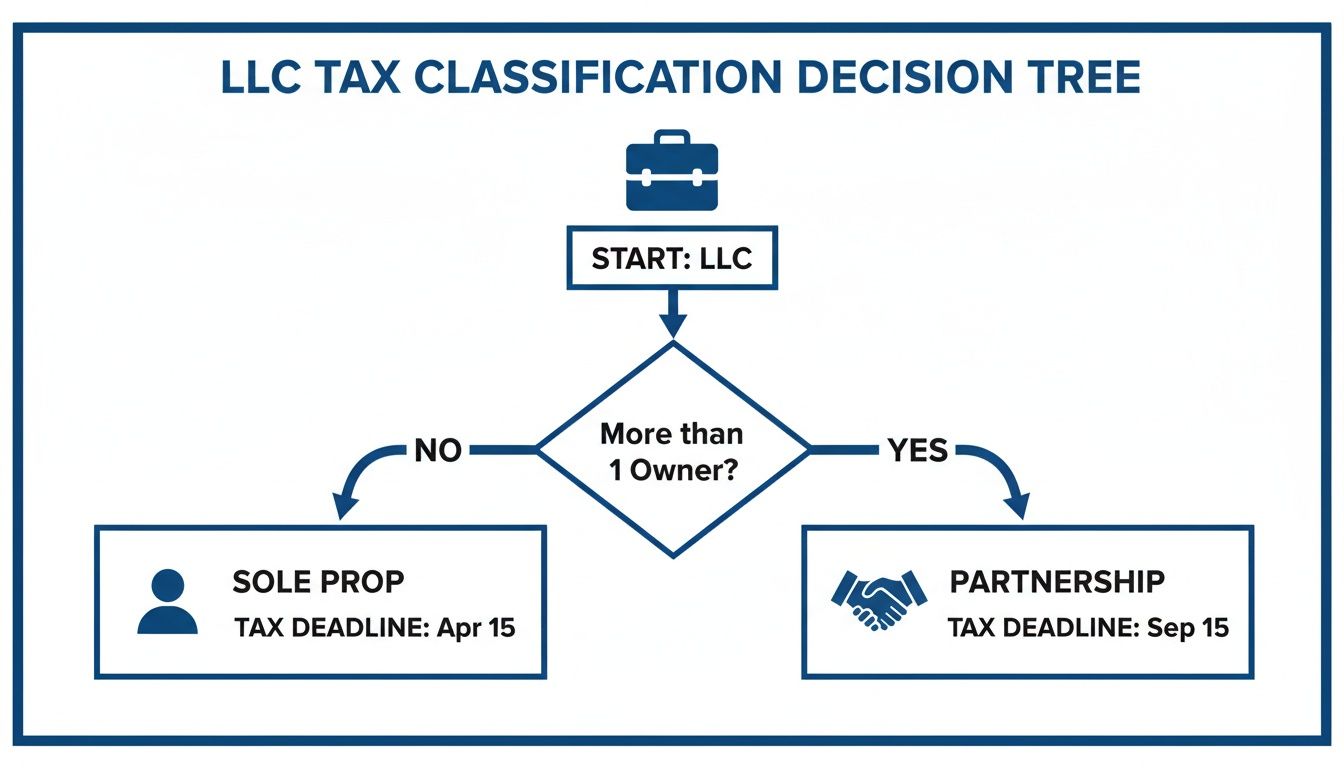

How Your LLC's Tax Structure Defines Your Deadline

The first thing to understand about an LLC tax extension is that there’s no single, universal deadline. Why? Because an LLC is what I like to call a "tax chameleon"—it can take on the tax identity of several other business structures. The specific choice you've made for your LLC is the single most important factor that sets your tax filing calendar.

This election determines your original due date, which extension form you need to file, and your final extended deadline. Getting this wrong is one of the most common—and costly—mistakes I see business owners make. It all starts with knowing exactly how the IRS sees your business.

Single-Member vs. Multi-Member LLCs

The first fork in the road is simple: how many owners (or "members") does your LLC have? This basic question establishes your default tax status and, by extension, the entire process for getting more time to file.

- Single-Member LLC (SMLLC): By default, the IRS treats an LLC with one owner as a sole proprietorship. This means the LLC itself doesn't file a separate business tax return. Instead, all your business income and expenses are reported on Schedule C of your personal Form 1040.

- Multi-Member LLC: If your LLC has two or more members, the IRS automatically classifies it as a partnership. The business files its own informational return (Form 1065), and you and your partners each get a Schedule K-1 that you’ll use for your personal tax returns.

This decision tree shows just how directly your LLC's structure connects to its tax deadline.

As you can see, the path is straightforward. The number of members points directly to a tax classification, which then dictates the filing timeline.

The Two Roads to an Extension: Form 4868 vs. Form 7004

Since LLCs can be taxed so differently, there are two separate forms for requesting an extension. You absolutely must use the right one.

If you have a single-member LLC taxed as a sole proprietorship, you’ll file Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. This form extends your personal tax return, which is where your LLC's activity is reported anyway. It pushes your filing deadline from April 15 to October 15.

For multi-member LLCs (and any LLCs that have chosen to be taxed as corporations), the business must file its own extension.

The modern six-month extension for business returns is handled through IRS Form 7004. As long as you file it by the original due date, the extension is automatic—no questions asked. The IRS doesn't require a reason. This single form covers partnerships, S-corps, and C-corps, making it the go-to for most business entities needing more time. You can find all the details on the IRS guidance on Form 7004.

So, a multi-member LLC files Form 7004 to extend its Form 1065 deadline from March 15 to September 15.

Electing Corporate Status and Its Impact

Just to add another layer, any LLC—whether it has one member or many—can formally elect to be taxed as a corporation. Business owners do this for various strategic reasons, and this choice completely changes the filing rules.

- S Corporation Election: If your LLC is taxed as an S Corp, it files Form 1120-S. Just like a partnership, the original due date is March 15. A properly filed Form 7004 extends that deadline to September 15.

- C Corporation Election: An LLC taxed as a C Corp files Form 1120. Its deadline aligns with the personal tax calendar—originally due April 15. Filing Form 7004 gives you an extension to October 15.

Knowing your LLC's tax classification is the bedrock of compliance. It tells you which form to file and what date to circle on your calendar, helping you avoid simple errors before they snowball into real problems.

The Critical Difference Between Filing and Paying

This is one of the most common—and costly—misunderstandings in the tax world. An extension to file your LLC's tax return is absolutely not an extension to pay your taxes. Think of it this way: your team has a major project deadline, and you get an extension to submit the final report. That doesn’t mean you can just skip the budget meeting where you’re supposed to present the project's financial impact.

The IRS operates on the same principle. Your original due date, whether it's March 15 or April 15, is the hard deadline for settling your tax bill. The extension simply gives you more time to get the paperwork right. Ignoring this distinction is a surefire way to rack up penalties and interest.

Making a Good-Faith Estimated Payment

To get a valid extension, you have to make a good-faith estimate of your total tax liability for the year and pay at least that amount by the original deadline. This payment usually goes in with your extension form, whether that’s Form 7004 for the business or Form 4868 for a single-member LLC.

So, what exactly is "good faith"? It’s not a wild guess. It means you have to use the real financial data you have on hand—like your P&L statements and balance sheets—to make a reasonable calculation of your income, deductions, and what you’ll ultimately owe.

The IRS has a low tolerance for lowball estimates. If you show "scant evidence" of a real attempt to figure out your tax liability, they can invalidate your extension. If that happens, your return becomes retroactively late, and the penalties kick in immediately.

This isn't an optional step. For a profitable real estate partnership or a family business, this estimated payment can be a significant check to write. That’s why it’s critical to review your finances well ahead of the deadline to make sure the cash is ready.

The High Cost of Underpayment

Even if you get an approved extension to file, failing to pay your estimated tax by the original due date triggers immediate financial consequences. The IRS penalty system is designed to hurt, and the costs can snowball faster than you’d think.

You’re looking at two main penalties:

- Failure-to-Pay Penalty: This is 0.5% per month (or even part of a month) on the unpaid tax. It keeps building until you pay in full, up to a cap of 25% of what you owe.

- Interest on Underpayment: On top of the penalty, the IRS charges interest on the unpaid balance. The rate changes quarterly and, worse, it compounds daily, turning a small debt into a much bigger problem over time.

A Practical Example of Penalties in Action

Let’s walk through a scenario. A multi-member LLC based in New York City invests in real estate. It was a good year, and the partners calculate their federal tax liability to be $100,000. They file Form 7004 on time by March 15 to get an extension, but they don't send in the payment.

Here’s how the damage unfolds:

- Failure-to-Pay Penalty: The 0.5% monthly penalty starts ticking right away. On $100,000, that’s $500 every single month.

- Accruing Interest: Interest also begins compounding daily on the full $100,000 from March 15 onward.

If they finally pay up when they file their return on the extended due date for an LLC tax return with extension in September, they’ve already racked up six months of penalties ($3,000) plus all that daily compounded interest. What was a manageable tax bill has now become a much more expensive, and entirely avoidable, problem. For high-net-worth individuals with significant pass-through income, these kinds of penalties can easily climb into the tens of thousands.

Navigating New York State and NYC Tax Extension Rules

Securing a federal extension is a great first step, but it's only half the battle if you operate in a place like New York. A very common—and costly—misconception is that filing for a federal extension automatically takes care of your state and city obligations. It doesn't. This single assumption can trigger a wave of unexpected penalties from Albany and New York City, even when you think you've done everything right.

Think of it like getting a visa for a country; that visa doesn’t automatically grant you access to every restricted region within its borders. Your federal extension works much the same way—it's not a universal pass for state and local tax filings. New York, in particular, has its own rulebook you need to follow.

When a Federal Extension Is Enough for New York State

The good news? New York State does try to keep things simple in some cases. For many LLCs, New York automatically honors a properly filed federal extension. If you filed Form 7004 for your partnership or S-Corp, or Form 4868 for your single-member LLC, you generally don't need to file a separate state extension request.

But there's one critical condition: you must not owe any New York State tax. If you've made timely estimated payments all year and project a zero balance or are due a refund, the federal extension is usually all you need. In that scenario, your extended NYS due date simply mirrors the federal one—September 15 for partnerships and S-Corps, and October 15 for sole proprietorships.

This convenience disappears the moment you have a state tax bill.

If your LLC owes New York State taxes, you must file a separate state extension and pay the estimated tax you owe by the original deadline. Relying on your federal extension without paying the state will absolutely result in late-payment penalties, no matter what you filed with the IRS.

How to File a New York State-Specific Extension

When you do have a tax payment due to New York, you need to proactively file for a state extension. The form you'll use depends on how your LLC is taxed, just like at the federal level.

- For LLCs taxed as partnerships or individuals (SMLLCs): You’ll need to file Form IT-370, Application for Automatic Six-Month Extension of Time to File for Individuals.

- For LLCs taxed as corporations: The correct form is NYS Form CT-5, Request for Six-Month Extension to File.

Filing the right form along with your estimated payment is non-negotiable. It tells New York that you know you have an obligation and intend to file a complete and accurate return, you just need a bit more time to get it done.

The Extra Layer: New York City Taxes

For any business with a footprint in the five boroughs, compliance gets even more complex. New York City levies its own taxes, like the Unincorporated Business Tax (UBT) or the General Corporation Tax (GCT), and these come with their own unique extension requirements.

Just as with the state, an extension to file is not an extension to pay your NYC tax bill. You have to estimate your city tax liability and send that payment in with the proper city-specific extension form by the original due date. Forgetting this step is a frequent and expensive mistake for NYC-based businesses, especially in real estate and finance where incomes can be significant.

Getting these State and Local Tax (SALT) details right is fundamental to protecting your assets. The due date for an LLC tax return with extension isn't just a single federal date; it's a multi-layered deadline that demands serious local diligence.

The Real Cost of Missing Your Extended Deadline

Filing a tax extension gives you a crucial six-month breather to get your paperwork in order, but that's where the flexibility ends. It's a hard stop. There are no more grace periods.

Blowing past that extended due date—whether it's September 15 or October 15—triggers a series of painful financial penalties that can quickly eat into your business profits and personal wealth. Treating this deadline as a "soft" target is one of the costliest mistakes you can make. The IRS sees it as the absolute last day to file, and the penalties for missing it are far more severe than those for simply paying late.

The Two-Headed Monster of IRS Penalties

When you miss the extended due date for your LLC tax return, you’re usually staring down two different penalties that can stack up at the same time, creating a real financial mess.

- Failure-to-File Penalty: This is the big one. It’s calculated at 5% of the unpaid tax for each month (or even part of a month) that your return is late.

- Failure-to-Pay Penalty: This penalty keeps ticking on any balance you didn't pay by the original due date. It’s calculated at 0.5% of the unpaid tax for each month the tax isn't paid.

When both penalties apply, the IRS combines them. They reduce the failure-to-file penalty by the amount of the failure-to-pay penalty, but the total combined hit is still capped at 5% per month. To make matters worse, the IRS charges interest, which compounds daily, on both the unpaid tax and the penalties themselves.

The IRS failure-to-file penalty is punitive on purpose. It’s designed to be ten times harsher than the failure-to-pay penalty to send a clear message: don't ignore your filing obligations just because you got an extension.

How Penalties Can Snowball: A Real-World Example

Talking about percentages is one thing, but seeing the actual dollar damage really brings it home. Let’s walk through a scenario for a profitable, closely held business.

Imagine an NYC-based real estate LLC, taxed as a partnership, that had a great year. The partners did everything right and filed Form 7004, pushing their filing deadline to September 15. But then life got in the way, and due to an oversight, they didn't file their return or pay their remaining federal tax liability of $200,000 until February 20 of the next year.

Here’s how that financial hit breaks down:

- Late Period: The return is late for part of September, all of October, November, December, January, and part of February. For penalty math, the IRS rounds up and calls that six months.

- Failure-to-File Penalty: This penalty maxes out at 25% after five months. So, 25% of $200,000 is a staggering $50,000.

- Failure-to-Pay Penalty: This would have been quietly accumulating since the original March 15 deadline.

- Daily Interest: On top of all that, interest would be compounding daily on the initial $200,000 tax bill and on the penalties as they piled up.

Just like that, a simple oversight turns a $200,000 tax bill into a total liability well over $250,000 in less than six months. For high-net-worth individuals who get large K-1 distributions from their businesses, missing an extended October 15 deadline can lead to the same kind of devastating result.

As you can discover more insights about LLC tax extensions on venturesmarter.com, the penalties are tied directly to the amount of tax you owe, which means the stakes get incredibly high for successful businesses. This is exactly why the due date for an LLC tax return with extension must be treated as a non-negotiable, final deadline. It’s absolutely essential for preserving your financial health.

How to Correctly File Your LLC Tax Extension

Filing for a tax extension isn't about dodging your responsibilities. It’s a smart, strategic play to buy the time needed to get your tax return right. When you do it correctly, the process is straightforward and can save you a world of stress and potential penalties.

Think of it as a pre-flight checklist. By methodically going through a few key steps, you ensure you have everything in order for a smooth landing on your new, extended due date. It all starts with knowing exactly what kind of business you’re running in the eyes of the IRS.

Step 1: Confirm Your LLC's Tax Classification

First things first: you absolutely must know how your LLC is classified for tax purposes. Is it a disregarded entity treated like a sole proprietorship? A partnership? Or has it elected to be an S corp or C corp? This single detail is the bedrock of the entire process.

Your tax classification dictates which extension form to use and what your original deadline is. Getting this wrong can invalidate your extension from the get-go. For instance, filing Form 4868 for a multi-member LLC is a non-starter. Always double-check your status before you do anything else.

Step 2: Gather Financials and Estimate Your Tax Liability

With your classification locked in, it's time to pull together your key financial documents—profit and loss statements, balance sheets, and records of any major transactions throughout the year. The goal here is to arrive at a reasonable, good-faith estimate of your total tax bill.

This is the most critical part of the whole exercise, because an extension to file is not an extension to pay. You are still required to calculate and pay what you owe by the original deadline. A careful review of your numbers is non-negotiable.

A word of caution: The IRS expects a reasonable estimate. If you file an extension with a zero payment or a suspiciously low number when you clearly had a profitable year, they have the authority to invalidate the extension. That would make your return retroactively late, and penalties and interest would start ticking from the original due date.

Step 3: Complete and Submit the Right Extension Form

Now, you can tackle the paperwork. The form you need is tied directly to your tax classification:

-

Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return: This is the form for single-member LLCs taxed as sole proprietorships. Your business activity flows through to your personal Form 1040, so this extends your personal filing deadline to October 15.

-

Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns: This is the go-to form for multi-member LLCs (partnerships) and any LLC that has formally elected to be taxed as an S corporation or a C corporation. This provides an automatic six-month extension for the business's return.

You have to get the correct form filed—either electronically or by mail—before the clock strikes midnight on your original tax deadline.

Step 4: Pay Your Estimated Tax by the Original Deadline

Filing the form is only half the battle. You also have to send your estimated tax payment to the IRS by the original due date—that’s March 15 or April 15 for nearly all calendar-year filers. You can pay easily through the IRS Direct Pay website, mail a check with your extension, or use other approved payment methods.

Making this payment on time is essential. If you don't, you'll get hit with failure-to-pay penalties and interest, even if you filed the extension paperwork perfectly.

Step 5: Mark Your New Deadline on the Calendar

Once your form is filed and your payment is sent, take one final, simple step: mark your new extended due date in big, bold letters on your calendar.

Whether it’s September 15 or October 15, treat this new date as a hard, final deadline. Missing it will trigger much harsher failure-to-file penalties, completely negating all the work you put into securing the extension in the first place.

Your Top LLC Tax Extension Questions, Answered

Even with the best planning, specific questions always pop up around tax extensions. Let's tackle some of the most common ones we hear from business owners to clear up any lingering confusion about the extended due dates for LLC tax returns.

Think of this as your quick-reference guide for a stress-free filing season.

Can I Get Another Extension After the First One?

The short answer is almost always no. That six-month extension you get with a Form 7004 or Form 4868 is typically a one-shot deal. The IRS views it as an automatic, generous window to get your documents in order.

Further extensions are incredibly rare and are generally reserved for taxpayers in federally declared disaster areas. It’s critical to treat your extended deadline—whether it's September 15 or October 15—as the final, hard stop.

What if I Paid Too Much With My Extension?

Overpaying your estimated tax is a good problem to have—it's far better than underpaying. If you send in more with your extension than your final tax bill shows you owe, that extra cash simply sits as a credit on your account.

Once you file the complete return, you have a couple of choices:

- You can get the entire overpayment back as a tax refund.

- Or, you can apply some or all of it toward your estimated taxes for the next year.

This flexibility is why we often advise clients to err on the side of caution. A slight overpayment is a smart move that helps you sidestep any nasty surprises with underpayment penalties and interest.

Does Filing an Extension Make Me an Audit Target?

This is a persistent myth that causes a lot of unnecessary stress. Let's be clear: filing for an extension does not increase your chances of being audited.

Extensions are a standard, legitimate part of the U.S. tax system used by millions of individuals and businesses every year. The IRS understands that complex financial situations need more time. In fact, filing a rushed, inaccurate return to meet the original deadline is far more likely to raise a red flag than filing a complete, well-documented return on an extended one.

An extension signals diligence, not avoidance. It shows you’re taking the time to get it right, whether you're waiting on K-1s from a real estate partnership or finalizing the books for your closely held business.

Does My New York LLC Need Its Own Extension?

This is where it gets tricky, and the answer really depends on your specific situation. New York State will often accept a federal extension automatically, but there’s a big catch: this only applies if you owe zero NYS taxes.

If you have a New York tax bill to pay, you absolutely must file a separate state extension form. For single-member LLCs, that’s typically Form IT-370. For LLCs taxed as corporations, it's Form CT-5. Just as with the IRS, you have to pay what you expect to owe by the original deadline to keep the state from hitting you with penalties.

At Blue Sage Tax & Accounting Inc., we transform complexity into clarity. We partner with successful individuals, family offices, and businesses to manage every detail of tax compliance and planning, ensuring you meet every deadline with confidence. Schedule a consultation today.