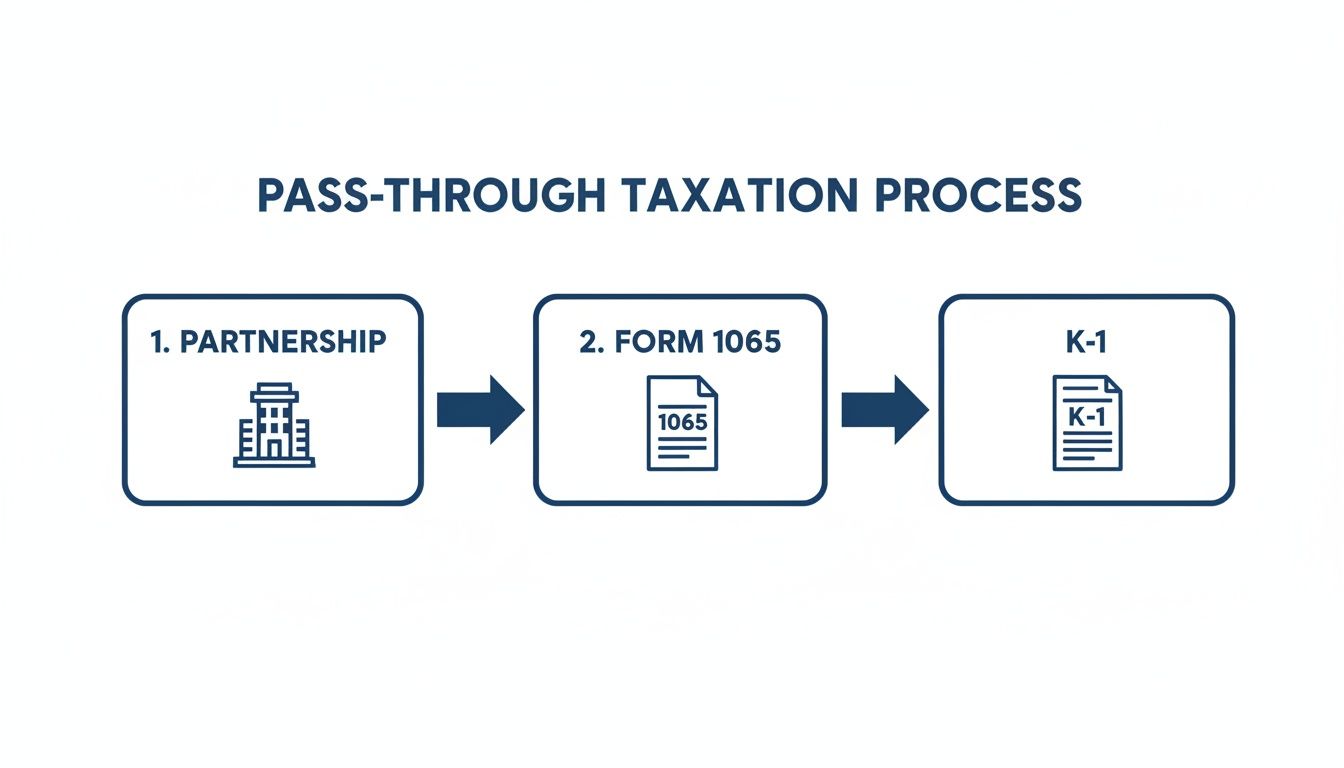

At the heart of partnership taxation lies the relationship between Form 1065 and its vital offshoot, the Schedule K-1. You can’t really talk about one without the other. Form 1065 is the master document, detailing the partnership's entire financial story for the year. The K-1, on the other hand, is the personal memo that breaks down that story for each individual partner.

This structure is what makes the whole system work, ensuring partnership income is taxed where it belongs: with the partners, not the business itself.

The Form 1065 and Schedule K-1 Connection

A partnership is what we call a pass-through entity. This is a crucial concept because it means the business sidesteps the double taxation that C corporations face. The partnership itself doesn't pay federal income tax. Instead, every dollar of profit, loss, deduction, and credit flows directly through to the partners.

Think of Form 1065 as the partnership's main tax ledger for the year. It’s where you tally up everything—gross receipts, operating costs, capital gains, charitable donations, you name it. Once you’ve calculated these totals on the form's Schedule K, the real work begins: allocating them.

That’s where the Schedule K-1 comes in. It’s the bridge that takes the partnership’s big-picture numbers and translates them into the specific amounts each partner needs for their own tax return. Since allocations are driven by the partnership agreement, one partner's K-1 can look completely different from another's.

Key Concepts in Partnership Taxation

To really get the hang of the Form 1065 and K-1 process, a few core principles are non-negotiable. These concepts dictate how everything is reported and ultimately shape what each partner owes Uncle Sam.

- Partner Basis: This isn't just the cash a partner put in. Basis is a partner's total tax investment in the business, adjusted year after year for their share of income, losses, and any money they take out. It’s a critical number because it sets the ceiling on how much in partnership losses a partner can deduct on their personal return. If you run out of basis, you can’t deduct any more losses.

- Separately Stated Items: Some financial items are special. They aren't just lumped into ordinary business income. Things like long-term capital gains, Section 179 deductions, and charitable gifts keep their unique tax character. They're broken out separately on the K-1 so each partner can handle them correctly on their own 1040.

- Tax Basis Capital Account: Now a required reporting item (you'll see it in Item L on the K-1), this tracks a partner's capital using tax accounting rules. It's not just a bookkeeping exercise; it gives the IRS a much clearer view of each partner's true economic position from one year to the next.

The Growing Importance of Partnership Filings

Understanding the nuances of Form 1065 has never been more critical. The partnership structure has exploded in popularity. From 2010 to 2019, the number of partnership returns filed in the U.S. jumped by nearly 27%, climbing from 3.3 million to 4.2 million.

The numbers behind those filings are staggering. In tax year 2019 alone, U.S. partnerships reported over $1.1 trillion in net income. A huge chunk of that was concentrated in real estate and financial services, sectors where we see many of our high-net-worth clients. If you're curious, the IRS SOI data analysis paints a fascinating picture of this growth.

Navigating partnership tax filings correctly is essential. Let’s look at the deadlines you absolutely cannot miss.

Key Form 1065 Filing Deadlines and Extensions

Meeting filing deadlines is non-negotiable to avoid automatic, and often substantial, penalties from the IRS. The table below provides a quick reference for the key dates for both calendar-year and fiscal-year partnerships.

| Filing Period | Original Due Date | Extended Due Date with Form 7004 |

|---|---|---|

| Calendar-Year Partnership (Jan 1 – Dec 31) | March 15 | September 15 |

| Fiscal-Year Partnership (e.g., Jul 1 – Jun 30) | The 15th day of the 3rd month after the tax year ends | The 15th day of the 9th month after the tax year ends |

Remember, filing Form 7004 grants an automatic six-month extension to file, not an extension to pay. If the partnership owes any tax (which is rare but possible with certain state or local taxes), that payment is still due by the original deadline. Mark these dates on your calendar—missing them is an expensive mistake.

A Practical Walkthrough of Form 1065

Completing Form 1065 is far more than a data-entry exercise; you're essentially crafting the official financial story of your partnership for the tax year. It all starts with the foundational details of the entity and builds toward the calculation of ordinary business income—the crucial figure that ultimately passes through to the partners. Let's break down the key sections, highlighting the critical decisions and common tripwires I see in my practice.

The first page of the 1065 is all about setting the stage. You'll input the basics: the partnership's name, address, and Employer Identification Number (EIN). But right here, you also make a huge decision—your accounting method. Choosing between cash basis and accrual basis accounting has lasting consequences for how you recognize income and expenses.

For instance, a service-based consulting firm might opt for the cash method. It's straightforward: revenue is recognized only when a client's payment actually hits the bank. On the other hand, a real estate partnership holding significant inventory or managing large receivables is almost always required to use the accrual method. This method matches income and expenses to the periods they're earned or incurred, regardless of when cash changes hands. Be warned: this choice is made on your very first return and can be a real headache to change later.

The infographic below gives a great visual of how the partnership's financial data flows from Form 1065 out to each partner via their individual Schedule K-1.

Think of it this way: Form 1065 is the source of truth, and the K-1 is the delivery vehicle that gets that tax information to the partners' personal returns.

Reporting Income and Guaranteed Payments

The income section, spanning lines 1a through 7, is where you tally up the partnership's earnings for the year. It kicks off with gross receipts or sales (line 1a), adjusted for any returns and allowances. From there, you subtract the cost of goods sold (line 2) to land on your gross profit. It's absolutely critical that these figures tie out perfectly to your internal books.

One area that frequently trips people up is guaranteed payments to partners, found on line 10. These are payments to a partner for their services or for the use of their capital, and they're determined without regard to the partnership's income.

Key Insight: Guaranteed payments are a business deduction for the partnership, which lowers its ordinary income. For the partner receiving them, however, they are considered self-employment income, reported on their K-1 and subject to self-employment taxes.

Imagine a managing partner in a real estate development firm who receives a fixed salary of $120,000 for her management work. The partnership deducts that $120,000 on page 1 of Form 1065. That same $120,000 then appears on her Schedule K-1 in Box 4a, ensuring it's properly taxed on her individual return.

Maximizing Business Deductions

The deductions section (lines 9 through 21) is where sharp tax planning can really move the needle. This is your chance to list all ordinary and necessary business expenses. You’ll see the usual suspects here:

- Salaries and wages for any non-partner employees.

- Rent paid for your office space or equipment.

- Taxes and licenses, like state franchise taxes or local business permits.

- Depreciation, including powerful elections like the Section 179 deduction.

That Section 179 deduction, in particular, is a game-changer. It allows a business to write off the full purchase price of qualifying equipment in the year you start using it, instead of slowly depreciating it over several years. For a tech startup, this could mean immediately deducting the entire cost of $50,000 in new servers and computers. This creates a significant, immediate drop in taxable income. The deduction itself is calculated on Form 4562, with the total flowing through to Form 1065, line 14.

Once you’ve subtracted all your allowable deductions from the partnership's total income, you arrive at the ordinary business income (or loss) on line 22. This one number is the culmination of all your core business operations and becomes the starting point for allocations on Schedule K. Getting this figure right is the first step to mastering the entire Form 1065 and Schedule K-1 process.

From the Partnership's Books to Each Partner's Pocket: Translating Schedule K

After you've wrestled with the numbers on page one of Form 1065 to arrive at the partnership's ordinary business income, your next stop is Schedule K. Think of it as the grand total—the complete financial picture of the partnership for the tax year. It's where every piece of income, every deduction, and every credit gets tallied up before a single dollar is allocated to the partners.

This schedule is the master blueprint. Every number that eventually lands on an individual partner's Schedule K-1 starts here. This is non-negotiable: the sum of the amounts on a specific line across all the partner K-1s must tie back perfectly to the total on the corresponding line of Schedule K. The IRS software checks this automatically, so getting it right is fundamental.

This is arguably the most critical juncture in the entire return process. You're moving from the partnership's world to the individual partner's world, and it’s all dictated by one foundational document.

The Partnership Agreement Is Your Rulebook

When it comes to allocations, the partnership agreement is king. This document governs exactly how every financial item—profits, losses, deductions, credits—is sliced and diced among the partners. While a simple 50/50 profit split is common, the agreements for the closely held businesses and high-net-worth clients we see are rarely that straightforward.

The agreement can get incredibly specific. For instance, two partners might share the day-to-day operating profits equally, but agree to a 70/30 split on capital gains from a real estate sale to account for one partner's larger initial investment. Your job is to translate these legal terms into tax figures.

Expert Tip: The IRS has a critical standard for these agreements: they must have "substantial economic effect." This isn't just jargon. It means the tax allocations must mirror the real-world economic arrangement. You can't just allocate all the losses to the high-income partner to give them a big tax break if they aren't actually bearing the financial brunt of those losses.

If your allocations don't pass this test, the IRS has the authority to throw them out and reallocate everything based on what it determines to be the partners' true interests. That's a messy and expensive situation you want to avoid.

Why Separately Stated Items Matter

A core concept in the form 1065 instructions schedule k-1 is the handling of separately stated items. These are specific types of income, loss, deduction, or credit that don't get lumped into the ordinary business income on page one. Instead, they flow through to the partners, keeping their original tax DNA intact.

This is a huge deal for the individual partner. Why? Because different types of income are taxed differently on a personal return. A long-term capital gain, for example, enjoys a much lower tax rate than ordinary business income. If you just buried that gain in the partnership's net income, the partner would lose that significant tax advantage and pay more than their fair share.

Here are some of the most common items you'll see passed through separately:

- Net rental real estate income (or loss), which partners report on their personal Schedule E.

- Interest and dividend income, which retains its character as portfolio income.

- Capital gains and losses (both short-term and long-term), flowing directly to Schedule D.

- Charitable contributions, which partners can deduct on Schedule A if they itemize.

- Section 179 deductions, which are subject to limitations at the individual partner level.

Each of these items gets its own line on Schedule K, ready to be distributed to the partners' K-1s while preserving its unique tax character.

Getting Special Allocations Right

This is where partnership tax preparation becomes both an art and a science, especially in sophisticated real estate or investment deals. A special allocation is any division of a tax item that doesn't follow the partners' standard profit-and-loss ratio. It’s a powerful way to reflect the unique contributions and risks of each partner.

Let's imagine a real estate partnership. Partner A puts up the cash for the down payment, and Partner B brings their management expertise to the table. Their agreement might include a special allocation:

- The first $50,000 of depreciation deductions each year goes 100% to Partner A, rewarding them for their capital at risk.

- Any income or other deductions after that are split 50/50.

This is a perfectly legitimate structure, provided it has substantial economic effect. The key is ensuring your tax software is set up to handle these specific instructions. You can't just apply a single percentage down the line. The integrity of each K-1 hinges on your ability to meticulously translate the nuanced terms of the partnership agreement into the return, a skill that's at the heart of the form 1065 instructions schedule k-1 guidelines.

A Box-by-Box Breakdown of Schedule K-1

The Schedule K-1 is where all the partnership's financial activity finally hits home for each partner. Think of it as the ultimate handoff—the critical document that translates the partnership’s complex operations into the specific numbers a partner needs for their own Form 1040.

For any professional handling these returns, getting every box right is non-negotiable. And for the partner receiving it, understanding what these numbers mean is just as important. Let’s walk through the key lines in Part III, which is the heart of the form.

This document is much more than a simple summary; it's a direct instruction sheet for the partner's personal tax return. An error here creates a domino effect, almost guaranteeing an incorrect 1040 and a potential notice from the IRS down the line.

Core Income and Loss Items

The first few boxes of the K-1 are the bread and butter, covering the most common types of pass-through income and loss.

-

Box 1 Ordinary Business Income (Loss): This is the big one. It's the partner's slice of the net profit or loss from the partnership's main business. This number flows directly from Form 1065, page 1, line 22, and partners will report it on Schedule E (Form 1040), Part II.

-

Box 2 Net Rental Real Estate Income (Loss): If the partnership is in the real estate game, this is where the partner's share of net income or loss from those properties shows up. It also lands on Schedule E, but it’s kept separate from the ordinary business income.

-

Box 3 Other Net Rental Income (Loss): This is a bit less common but covers rental income from things other than real estate, like leasing out heavy equipment. As you might guess, this also finds its way to Schedule E.

-

Box 4 Guaranteed Payments: This line is for payments made to a partner for their services or the use of their capital, which are calculated regardless of the partnership's profitability. It's treated as ordinary income and is almost always subject to self-employment tax.

Investment and Capital Gain Reporting

Beyond the daily grind, the K-1 carefully separates out investment-related income. This is absolutely critical because these items are often taxed at very different rates than standard business income.

For instance, interest income in Box 5 flows over to Schedule B of the partner's Form 1040. The same goes for dividends in Box 6a (Ordinary) and Box 6b (Qualified). That Box 6b number for qualified dividends is especially important, as those are taxed at the much friendlier long-term capital gains rates.

Speaking of capital gains, they get their own breakdown:

- Box 9a Net long-term capital gain (loss): The partner’s share of gains or losses from assets the partnership held for more than one year. This gets reported on Schedule D (Form 1040).

- Box 9b Collectibles (28%) gain (loss): If the partnership sold collectibles like art or precious metals, those gains are taxed at a special 28% rate and are flagged here to be reported separately on Schedule D.

Key Takeaway: The K-1’s entire structure is designed to preserve the tax character of each type of income. This is a huge benefit for the partner, who gets to take direct advantage of preferential tax rates for things like long-term capital gains on their personal return.

Decoding Box 13 Other Deductions

Box 13 can be a real head-scratcher. It's a catch-all for various deductions identified by codes, and it’s where many preparers trip up. The partnership must provide an attached statement that clearly explains what each reported code represents.

Some of the most frequent codes you'll see are:

- Code C Charitable Contributions: The partner’s portion of the partnership's donations. This is a personal deduction on the partner’s Schedule A (Form 1040), assuming they itemize.

- Code H Investment Interest Expense: This is interest on debt used to buy investments. The partner can deduct this on Form 4952, but only up to the amount of their net investment income.

- Code K Section 179 Deduction: This is the partner's share of the powerful Section 179 deduction. It's crucial to remember the partner must combine this amount with any other Section 179 expenses they have and apply the overall limitations at the individual level.

Don’t just glance at the codes; always dig into the attached statements for Box 13. These deductions can seriously reduce a partner’s tax bill, but only if they’re reported correctly on the proper forms.

Navigating Box 20 Other Information

Like Box 13, Box 20 uses codes to convey a ton of extra information that directly impacts the partner’s tax situation. This is where you find the nitty-gritty details for things like basis, at-risk limitations, and other complex calculations.

By far, the most important item here for most clients is Code AA Section 199A Information. This gives the partner the raw data—Qualified Business Income (QBI), W-2 wages, and UBIA of qualified property—needed to calculate their QBI Deduction on Form 8995. This deduction can be worth up to 20% of their QBI, making it one of the most valuable tax breaks available to pass-through owners.

Another critical piece of data is in Item L, which reports the partner's capital account. Back in February 2021, the IRS implemented a major shift by mandating tax basis capital reporting for most partnerships. This forces partnerships to meticulously track each partner’s capital on a tax basis, reconciling every contribution, distribution, and allocation each year. As explained in KPMG’s analysis of this rule change, this was part of a broader IRS effort to get better data, especially from complex PE and real estate funds.

Getting the K-1 right is a detailed, box-by-box process. Each number tells a part of the story, and together they provide the complete roadmap for the partner's personal tax return.

Navigating Common Pitfalls and Complex Scenarios

Once you've handled the basic entries on a Form 1065, you get to the real work. This is where even experienced preparers can get tripped up—the complex scenarios that, if mishandled, can create major tax headaches for the partners and attract serious penalties for the partnership itself.

Successfully preparing a partnership return isn't just about filling in boxes; it's about anticipating these challenges before they become problems. From the painstaking process of tracking partner basis to untangling a web of multi-state tax rules, getting the details right is everything. Let's dive into some of the most common—and high-stakes—issues I see in my practice.

The Critical Task of Tracking Partner Basis

One of the most essential yet frequently fumbled responsibilities is tracking each partner's outside basis. While the partnership reports a partner's capital account on the K-1, it’s ultimately the partner's responsibility to track their own tax basis. Think of this number as the gatekeeper for deducting losses and the key to figuring out if distributions are taxable.

A partner can only deduct partnership losses up to the amount of their basis. If their basis hits zero, any further losses get suspended and carried forward until they have enough basis in a future year. Overlooking this rule often leads to improperly claimed deductions that get flagged and reversed by the IRS.

Pro Tip: Distributions are usually tax-free as long as the partner has basis to cover them. But here’s the classic "gotcha" moment: cash distributions that exceed a partner's basis are treated as a capital gain. This surprises many partners who aren't closely watching their basis numbers from one year to the next.

Multi-State Operations and Apportionment

Things get exponentially more complicated when a partnership does business across state lines. Suddenly, you're not just filing a federal Form 1065. You most likely have filing obligations in every single state where the partnership has a footprint, which immediately brings apportionment into play.

Apportionment is simply the method used to slice up the partnership’s income among the states where it was earned. The catch? Every state has its own unique formula, usually a blend of the partnership's property, payroll, and sales in that state. This requires meticulous record-keeping and a solid grasp of each state's specific tax code.

The end result is that the partnership often has to issue state-specific K-1s. These supplemental forms give each partner the exact numbers they need to file their individual non-resident state tax returns—a crucial final step to being fully compliant.

The High Cost of Filing Errors

The IRS isn't messing around when it comes to accuracy and deadlines. The penalties for late or incorrect filings can be brutal, especially for partnerships with a lot of investors.

According to the official IRS Partner’s Instructions for Schedule K‑1 (Form 1065), a pass-through entity that fails to provide the required K-1s can face a $330 penalty per failure. That’s capped at a hefty $3,987,000 per year. If the IRS determines the failure was intentional, the penalty doubles to $660 per K-1 with no maximum cap. For a closely held fund or business, these penalties can spiral into the seven-figure range in a hurry.

Common Schedule K-1 Errors and How to Fix Them

Staying on top of the intricate form 1065 instructions schedule k-1 means being on guard for common mistakes. A small slip-up on the preparer's end can create a big problem for the partner.

Here’s a look at some of the most frequent errors I encounter and how you can get ahead of them.

| Common Error | Potential Impact | Pro-Tip for Correction |

|---|---|---|

| Incorrect Basis Reporting | Partners may improperly deduct losses or miscalculate gains on distributions. | Maintain a dedicated schedule to track each partner's outside basis annually. This should account for all contributions, distributions, and their share of income/loss. |

| Ignoring State Apportionment | Failure to file in all required states, leading to penalties and back taxes for both the partnership and partners. | Perform an annual nexus study to map out all state filing obligations. Use this to prepare accurate state-specific K-1s for every non-resident partner. |

| Misclassifying Guaranteed Payments | Payments are not properly deducted by the partnership or reported as self-employment income by the partner. | Your partnership agreement should explicitly define guaranteed payments vs. distributions. Report them on Form 1065 (Line 10) and the partner's K-1 (Box 4a). |

| Failing to Provide K-1s on Time | Partners can't file their personal returns on time, which triggers penalties for the partnership. | Set a hard internal deadline for finalizing the Form 1065 that leaves plenty of breathing room to issue K-1s well before the March 15 due date. |

By proactively addressing these areas, you not only ensure compliance but also provide significant value to the partners who rely on these documents for their own tax filings.

Form 1065: Your Questions Answered

Even after you've waded through the instructions, you're bound to have questions. Partnership tax has its quirks, and it's completely normal to hit a few stumbling blocks. Here are some of the most common questions that pop up, with practical answers to help you navigate the real-world side of Form 1065 and Schedule K-1.

What’s the Real Difference Between a Partner's Basis and Their Capital Account?

This is easily one of the most confusing areas, but getting it right is crucial. Think of it this way: a partner's capital account, which you see in Item L on the K-1, is the "inside" view. It’s a bookkeeping number that tracks what a partner put in, what they took out, and their slice of the partnership’s profit or loss.

The partner's "outside basis," on the other hand, is the full picture for tax purposes. It starts with the capital account but adds a critical piece: the partner's share of the partnership's debt. This outside basis is the number that really matters. It dictates how much loss you can actually deduct and determines if any distributions you receive are tax-free returns of capital or taxable events.

The partnership tracks the capital account, but each partner is ultimately responsible for tracking their own outside basis.

Can I Just File Form 1065 Myself? Do I Really Need a Professional?

Technically, yes, a partner can prepare and file Form 1065. But should you? In almost every case, the answer is a firm no. This isn't just about filling in boxes; it's about navigating a minefield of complex rules.

Things like special allocations, basis tracking, multi-state reporting, and the new K-2/K-3 requirements for international activity can easily trip up even the most diligent business owner. A single mistake on the 1065 creates a domino effect, leading to incorrect K-1s for every single partner. That can mean a cascade of amended personal returns, frustrating delays, and a much higher chance of attracting unwanted IRS attention and penalties.

Hiring a good tax professional isn't just about compliance. They often find tax-saving strategies—like optimizing depreciation or expense allocations—that can easily save you more than their fee.

Why Does My K-1 Show a Loss When the Partnership Made Money?

This is a classic scenario, especially for anyone invested in real estate. It boils down to the difference between cash in your pocket and "income" on paper for tax purposes. The biggest culprit here is usually a large, non-cash deduction like depreciation.

Imagine a partnership owns an apartment building. The rent collected easily covers the mortgage, taxes, and other operating costs, leaving the partnership with positive cash flow. But for tax purposes, the partnership gets to take a huge depreciation deduction on the value of the building itself. This paper expense can be large enough to wipe out the cash profit and create a net tax loss.

That tax loss then flows through to you on your Schedule K-1. If you have enough basis, you might even be able to use that loss to offset other income on your personal tax return.

It's essential to analyze the entire K-1, not just the final income or loss figure in Box 1, to grasp the full financial picture.

What Do I Do If I Get a Corrected Schedule K-1?

It happens. You've already filed your personal tax return, and then a "Corrected" Schedule K-1 shows up in the mail. If this happens, you almost certainly need to amend your personal return.

You’ll need to file a Form 1040-X, Amended U.S. Individual Income Tax Return. The new K-1 has different numbers for your share of income, deductions, or credits, which means the tax you originally calculated is now wrong. Taking the time to file an amended return is the only way to make sure you've paid the right amount of tax and avoid potential IRS notices and penalties later on.

Navigating the complexities of Form 1065 and Schedule K-1 requires precision and foresight. At Blue Sage Tax & Accounting Inc., we specialize in providing proactive tax planning and compliance for closely held businesses and high-net-worth individuals, ensuring your financial strategy is sound and your filings are accurate. Partner with us for clarity and confidence in your tax matters by visiting our official website.