Forget the popular idea of "making money while you sleep." The IRS has a much stricter, and frankly, less glamorous definition of passive income. Get it wrong, and you could face a nasty surprise on your tax bill.

Here’s the hook: if you work too hard on your "passive" business, the IRS might actually strip you of the tax benefits you were counting on. Their definition hinges on a critical concept called Material Participation. If you spend more than 500 hours a year on an activity, it’s usually not considered passive anymore. Understanding this distinction is the first step to mastering the tax code.

The Tax Man's Definition: It's All About How Much You Work

You might think that rental property or small business you started is a passive income goldmine. But the tax man sees it differently. If you're too hands-on, the IRS can reclassify that "passive" venture into an active business, and that changes everything.

The line in the sand here is a concept called material participation. It's basically the IRS's way of asking, "How involved are you, really?" They have a whole set of tests to figure out if your involvement is regular, continuous, and substantial. If it is, that income is considered active.

The 500-Hour Rule

The most straightforward test is the 500-hour rule. It’s simple: if you put in more than 500 hours on a business or rental activity during the year, it's almost certainly active in the eyes of the IRS. And they count everything—answering tenant calls, screening applicants, managing repairs, even marketing the property.

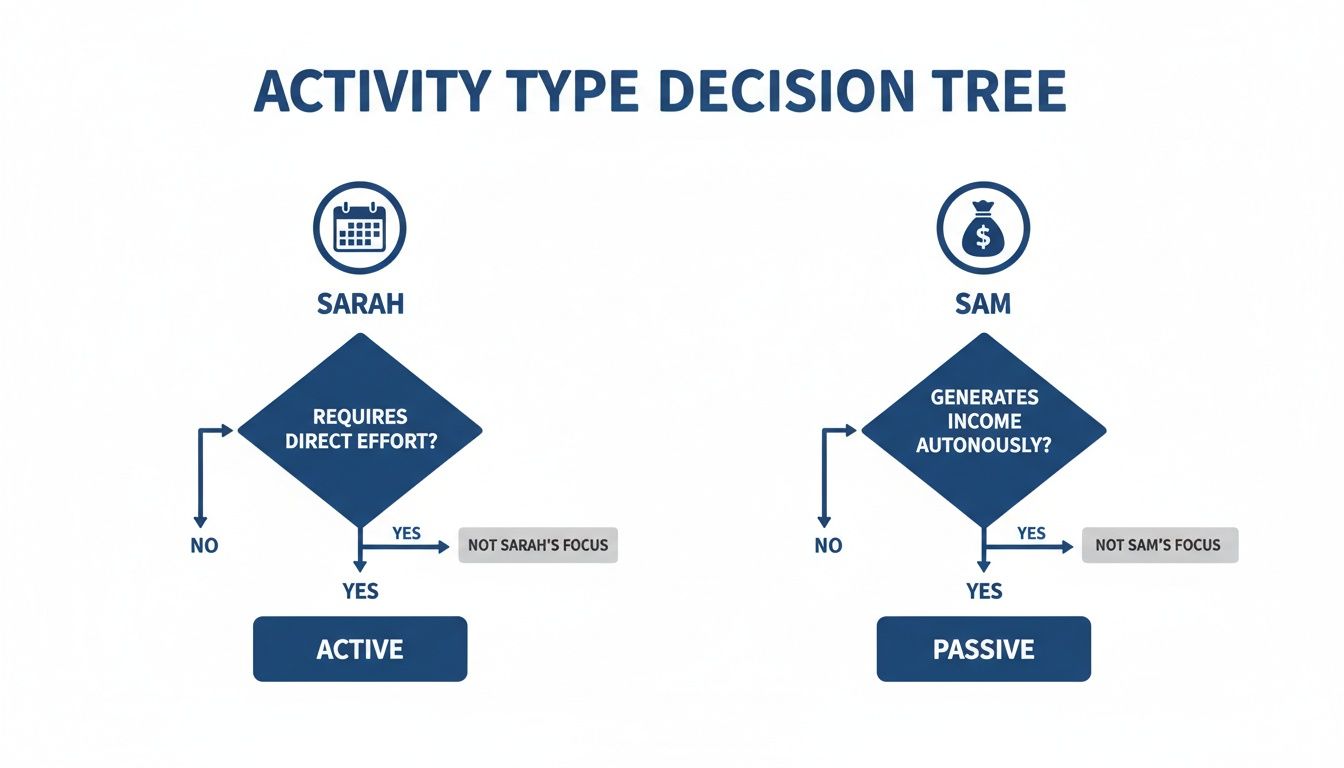

Let's look at two characters to see how this plays out in the real world.

- Side-Hustle Sarah: She owns an Airbnb but spends 20 hours a week managing it, coordinating cleaners, and answering guest inquiries. That's over 1,000 hours a year, so her "passive" side hustle is actually an active business in the eyes of the IRS.

- Silent Partner Sam: He invested in a friend's laundromat but never visits. He doesn't make decisions or show up to work—he just cashes the distribution checks. His involvement is minimal, so his income is truly passive.

Why the IRS Divides Your Income

So, why does the IRS care so much? It's all about putting your income into different buckets. They do this to stop people from using losses from one bucket (like a rental property) to wipe out the taxes they owe on income from another bucket (like their W-2 job).

This is where the infamous "passive loss trap" comes in. Generally, losses from a passive activity can only offset gains from other passive activities. You can't just use them to lower the tax bill from your day job.

Nailing this distinction is the first and most critical step in smart tax planning. It helps you classify your income correctly, predict what you'll owe, and start looking for ways to make the tax code work for you.

The Three Buckets of Income for Tax Planning

To build a smart tax strategy, you must see your money the way the IRS does. Imagine all your earnings flowing into three distinct "buckets." Each one holds a different kind of income, and more importantly, each comes with its own set of tax rules.

Getting these buckets mixed up is an easy mistake to make. Understanding which income goes where is the first, most crucial step in mastering passive income for tax purposes and planning like a pro.

Bucket 1: The Active (Earned) Income Bucket

This is money from your direct time and effort. If you have a W-2 job, earn tips, or run a business hands-on, your earnings flow right into this bucket. It's your most familiar income stream, but it's also the most heavily taxed, subject to both ordinary income tax and Social Security & Medicare taxes.

Bucket 2: The Passive Income Bucket

Here’s where things get interesting. For tax purposes, passive income comes from rental activities or businesses where you do not materially participate. You own a piece of the action, but you aren't involved in the day-to-day operations. This bucket was created specifically to stop investors from using "paper losses" from these ventures to wipe out taxes on their salaries.

Bucket 3: The Portfolio Income Bucket

This one is the classic source of confusion. Portfolio income often feels passive, but the IRS puts it in a completely separate bucket. This is money you make from investments like dividends, interest, and capital gains. The good news? It isn't subject to Social Security and Medicare taxes, and qualified dividends and long-term capital gains are often taxed at lower, preferential rates.

The Three Income Buckets Explained

This table breaks down the core differences in a simple, visual way.

| Income Type | Examples | Tax Treatment Highlight |

|---|---|---|

| Active (Earned) | Wages, Tips, Commissions | Subject to Social Security & Medicare taxes. |

| Passive | Rental Real Estate, Limited Partnerships | Losses can usually only offset passive gains. |

| Portfolio | Dividends, Interest, Capital Gains | Often confused with passive, but taxed at different rates. |

Understanding these three buckets is truly the first step toward smart tax planning. When you can confidently categorize your income, you can better predict your tax liability, sidestep common traps, and start finding ways to make the tax code work for you, not against you. You can dig into more corporate tax revenue data from the OECD to see how this fits into the bigger economic picture.

Meet Sarah and Sam: A Tale of Two Investors

Let's ditch the textbook definitions and get a real feel for how the IRS views passive income. Meet Side-Hustle Sarah and Silent Partner Sam. On the surface, they both own a piece of a business, but in the eyes of the tax man, they're playing two completely different games.

Side-Hustle Sarah: The Active Airbnb Host

Sarah owns an Airbnb and spends 20 hours a week managing it. She's deep in the weeds, handling everything from guest relations and coordinating cleaners to updating her online listing.

Because Sarah's involvement is so regular, continuous, and substantial (far exceeding the 500-hour test), her Airbnb income isn't passive at all. The IRS sees her as actively running a business. All that rental income flows straight into her Active Income Bucket.

Silent Partner Sam: The Hands-Off Investor

Now, let's turn to Sam. He invested in his friend's new laundromat as a limited partner. His involvement is purely financial; he provided capital and gets a cut of the profits in return. He has zero input on management decisions and never visits the business.

Sam's investment is the textbook definition of a passive activity. His complete lack of "material participation" means his laundromat income lands squarely in his Passive Income Bucket. He's a true silent partner.

Why This Distinction Changes Everything

Putting Sarah and Sam side-by-side makes the IRS's main point crystal clear: it’s not what you own, but what you do with it. This has huge tax implications. If Sarah's Airbnb loses money, she can likely deduct those losses against her other active income. But if Sam's laundromat posts a loss, those "passive losses" are generally stuck. He can only use them to offset gains from other passive investments.

Don't Get Caught in the "Passive Loss" Trap

One of the most gut-wrenching surprises for new investors is hitting the Passive Activity Loss (PAL) trap. You see a loss on your rental property's tax return and think, "Great, a tax write-off!" only to find out you usually can't use it to lower the taxes on your 9-to-5 salary.

The IRS essentially builds a firewall around your passive activities. The PAL rules dictate that losses generated inside the passive bucket must stay there. They can only be used to offset gains from other passive activities. You can find more details on how corporate tax rates have evolved over time.

Let’s walk through a quick example:

- You earn $150,000 from your day job (Active Income).

- Your rental property has a $10,000 paper loss for the year (Passive Loss).

The rookie mistake is thinking your taxable income is now $140,000. Nope. The PAL rules block that move. The $10,000 passive loss is "locked" or "suspended." You still owe tax on your full $150,000 salary.

The Secret Keys to Unlocking Your Losses

So, are those losses locked away forever? Not necessarily. The IRS provides a few "keys" that can unlock the trap, but you have to meet the requirements to a T.

- The $25,000 Allowance: This is a special rule for moderate-income earners. If you "actively participate" in your rental (a lower bar than material participation) and your Modified Adjusted Gross Income (MAGI) is under $100,000, you can deduct up to $25,000 in passive rental losses against your regular income. This benefit phases out and disappears completely once your MAGI hits $150,000.

- The "Holy Grail": Real Estate Professional Status (REPS): This is the ultimate prize for serious investors. If you qualify for REPS, the PAL firewall comes down entirely for your rental activities. It allows you to turn passive losses into active ones to save thousands on taxes. Qualifying is tough—it requires proving you spend more than 750 hours and over 50% of your total working time in real estate trades.

Creating "Tax Alpha": Your Strategic Advantage

Knowing about the passive loss trap is one thing. Learning the escape hatches is where you really start to create "tax alpha"—a term for the value you add by legally slashing your tax bill.

Let's dig into the powerful strategies that can turn paper losses from your real estate into real, tangible tax savings.

Depreciation: The Engine of "Paper Losses"

First, you have to understand where these "losses" come from. It's usually depreciation. This is the secret sauce of real estate investing—a non-cash expense that lets you write off a portion of your property's value each year for "wear and tear." This is how you can have cash in your pocket while showing a "loss" on paper. And it’s this exact paper loss that gets snagged by the PAL rules.

Strategy 1: The $25,000 Special Allowance

As mentioned, the IRS cuts some slack for hands-on landlords with moderate incomes. This allowance lets you deduct up to $25,000 in passive rental losses against your nonpassive income—like the salary from your day job.

To qualify, you have to hit two key marks:

- Active Participation: You generally meet this standard if you're involved in big decisions like approving tenants or okaying major repairs, even if you use a property manager.

- Income Threshold: Your Modified Adjusted Gross Income (MAGI) must be $100,000 or less to claim the full $25,000 deduction. The benefit disappears completely once your MAGI hits $150,000.

Strategy 2: Real Estate Professional Status (REPS)

For serious, high-income investors, this is the ultimate prize. Achieving Real Estate Professional Status (REPS) completely shatters the wall between your passive and active income buckets.

When you qualify for REPS, your rental losses can be treated as active losses, which you can then use to offset your other active income—your salary, your spouse's W-2 income, business profits—with no dollar limit. The tax savings can be massive.

But the requirements are tough, and the IRS is watching. You must meet both of these tests each year:

- The 750-Hour Test: You have to spend more than 750 hours during the year working in real estate trades or businesses.

- The More-Than-Half Test: The time you spend on real estate work has to be more than 50% of the total time you spend working in all personal services combined.

A Word of Caution: The IRS scrutinizes REPS claims. Meticulous, contemporaneous time logs detailing your hours and activities aren't just a good idea—they're your only defense in an audit.

The shift toward passive income is a massive part of our economy. By understanding and using these strategies, you can make sure your investments are working as hard for you as possible from a tax perspective. You can explore more about the global trends in corporate tax statistics to see the bigger picture.

Your Actionable Passive Income Tax Checklist

Alright, let's put all this theory into action. Run through these questions for your own portfolio. It’ll help you spot opportunities and get you ready for a much more productive chat with your tax advisor.

First, Nail Your Income Categories

The bedrock of any solid tax plan is getting the categories right.

- The Bucket Test: Have I sorted every single income stream I have into the right bucket: Active, Passive, or Portfolio?

- The Side-Hustle Reality Check: Is my "passive" business truly passive? Or am I spending more than 500 hours a year on it, making it an active business in the eyes of the IRS?

- The Logbook Imperative: Am I keeping a detailed, real-time log of the hours I spend on my rental properties? This is your ironclad proof for an audit.

Next, Get a Handle on the Passive Loss Rules

Once everything is sorted, the next step is figuring out how your gains and losses can (or can't) work together. Tripping over the Passive Activity Loss (PAL) rules is one of the easiest and most expensive mistakes an investor can make.

The whole reason the IRS created the "passive" bucket was to stop people from using losses from hands-off investments to wipe out taxes on their regular W-2 income. The default rule is simple: passive losses get "trapped" and can only be used against passive gains.

Finally, Hunt for Strategic Openings

Don't just assume your losses are stuck forever.

- The $25,000 Question: Is my MAGI under the $150,000 phase-out, and do I "actively participate" in my rentals? If so, I might be able to deduct up to $25,000 in rental losses.

- The Proving Ground: Am I a serious, full-time real estate player? Qualifying as a Real Estate Professional (REPS) is the ultimate key to using rental losses to offset your active income without limits.

Working through these questions will give you the clarity you need to stop reacting to the tax code and start managing it.

Common Questions About Passive Income and Taxes

Figuring out what the IRS considers "passive income" can feel like navigating a maze. Let's clear up some of the most common questions investors and business owners ask.

Is My Rental Income Always Passive?

You'd think so, but not always. The IRS automatically labels rental real estate as a passive activity, but your personal involvement can flip that switch.

If you can prove you’re a Real Estate Professional (REPS) and you materially participate in your rental properties, that income (and those losses) can be reclassified as nonpassive, or active. It's a tough standard to meet, but the tax benefits can be huge if you qualify.

Can I Use Losses From My Rental Property to Lower My W-2 Taxes?

In most cases, no. This is the whole point of the Passive Activity Loss (PAL) rules. Passive losses are stuck in their own lane and can generally only offset passive gains.

There is one major exception, though: the $25,000 special allowance for rental real estate. If you "actively participate" (a lower bar than material participation) and your Modified Adjusted Gross Income (MAGI) is under $100,000, you might be able to deduct up to $25,000 in rental losses from your regular income. This tax break phases out completely once your MAGI climbs to $150,000.

What If I Have Passive Losses Piling Up But No Passive Income?

Don't worry, those losses aren't lost forever. They get carried forward year after year, waiting for you to have some passive income to offset.

Here's the key: All of those suspended passive losses are fully unlocked and become deductible in the year you sell the entire property or activity. This can lead to a substantial tax deduction when you finally dispose of the asset.

Does Setting Up an LLC or S Corp Change the Passive Income Rules?

The legal structure of your business—whether it's an LLC, S Corp, or partnership—doesn't decide if the income is passive or active. It all comes back to one thing: material participation.

If you're a silent partner in an S Corp who just puts in cash, your share of the profits is passive. But if you're the one on the ground running the day-to-day operations, that same income is considered active.

Getting these rules right—from active participation to loss limitations—takes careful planning. At Blue Sage Tax & Accounting Inc., we work with investors and business owners to build smart, forward-thinking tax strategies. See how our team can help you get ahead at https://bluesage.tax.