When you're self-employed, filing your taxes boils down to a pretty straightforward process: you report what you made, subtract what you spent, and calculate the tax on what's left. The real key is to track every single dollar—both coming in and going out. This diligence is what allows you to accurately figure out your net profit, which is the number the IRS actually taxes you on.

What Are Your Self-Employment Tax Obligations?

Making the leap from a traditional W-2 job to being your own boss is a huge change, and nowhere is that more obvious than at tax time. Forget about an employer neatly withholding taxes from each paycheck. That's your job now.

You're now on the hook for your own federal and state income taxes, plus the big one that's unique to freelancers and business owners: self-employment tax.

This isn't just some niche requirement; a huge and growing part of the workforce is navigating these rules. Self-employment tax is simply how you pay into Social Security and Medicare. As a W-2 employee, you split the bill with your employer. But when you're self-employed, you have to cover both halves.

The self-employment tax rate is a flat 15.3% on your net business earnings. It breaks down like this:

- 12.4% for Social Security

- 2.9% for Medicare

It's crucial to remember this is in addition to your regular income tax. You'll use a couple of specific IRS forms to sort all this out, and while they can look a little daunting at first, they're manageable once you understand their purpose.

The Key Tax Forms You'll Be Using

To get this done, you really only need to get comfortable with two main forms: Schedule C and Schedule SE. Think of them as the building blocks for your self-employed tax return.

Schedule C, Profit or Loss from Business, is where you lay out the financial story of your year. You'll add up all the gross income you received from clients or customers. Then, you'll subtract all your legitimate business expenses—everything from a new laptop to your home office costs. The number you end up with is your net profit (or loss).

Pro Tip: Your net profit from Schedule C is arguably the most important number on your entire tax return. It doesn't just determine your income tax; it's also the starting point for calculating your self-employment tax.

Once you have that net profit, you'll take it over to Schedule SE, Self-Employment Tax. This is the form where you'll do the math for that 15.3% tax.

Here’s a quick-reference table to help you keep these forms straight.

Key Tax Forms for the Self-Employed

| Form Name | Purpose | Who Needs It |

|---|---|---|

| Schedule C | To report income or loss from a business you operated or a profession you practiced as a sole proprietor. | Any self-employed individual, freelancer, or independent contractor operating as a sole proprietorship. |

| Schedule SE | To calculate the self-employment tax (Social Security and Medicare taxes) you owe. | Anyone with net earnings from self-employment of $400 or more. |

| Form 1040-ES | To calculate and pay your estimated taxes for the year in four quarterly installments. | Individuals who expect to owe at least $1,000 in tax for the year, after subtracting withholding and credits. |

Mastering these forms is a core skill in the freelance economy. With millions of Americans filing their own returns each year, a huge number are tackling Schedule C for the first time. The IRS publishes detailed filing season statistics if you're curious about the trends. Ultimately, this entire process is the answer to how you file taxes when you're self-employed: you track, you report, you calculate, and you pay.

Building a Bulletproof Record-Keeping System

Let's be blunt: great record-keeping isn't just a "good habit." It's the absolute foundation of a stress-free tax season and your number one defense if the IRS ever comes knocking. When you can pinpoint every dollar earned and every dollar spent, you're not just organized—you're in control.

If you don't have a system, you're flying blind. You’ll almost certainly miscalculate your income, miss out on valuable deductions, and turn tax time into a frantic scavenger hunt for crumpled receipts. A solid system is the only way to find every single deduction you're legally entitled to.

Choose Your Record-Keeping Tool

First things first, you need to pick a system that actually works for you. There's no magic bullet here. The best tool is the one you’ll stick with.

For freelancers just starting out, a simple spreadsheet can do the trick. Set up columns for date, client, income, expense type, vendor, and cost. It’s a no-cost, hands-on way to get a feel for your cash flow.

But as your business gets more complex, dedicated accounting software becomes a game-changer. Platforms like QuickBooks or Wave are worth their weight in gold. They sync with your bank, automate invoicing, and generate financial reports in a couple of clicks, drastically cutting down on manual errors and saving you a ton of time.

The Golden Rule: Separate Your Finances

I see this all the time, and it's one of the most expensive mistakes a freelancer can make: mixing business and personal funds. It creates a nightmare paper trail that's nearly impossible for you—or the IRS—to untangle.

The fix is surprisingly simple. Open a dedicated business bank account and get a separate business credit card. That’s it. This one move creates a clean, undeniable line between your personal life and your business.

Every cent of business income goes into this account, and every business expense is paid from it or the business card. This isn't just about being tidy; it's a critical step in proving your business is a legitimate, separate entity.

Keeping your business and personal finances totally separate gives you a pristine, transaction-by-transaction record. It makes calculating your profit and spotting deductions incredibly straightforward and removes almost all the guesswork from your tax prep.

This discipline pays for itself when it's time to fill out your Schedule C.

Your Essential Document Checklist

Knowing what to keep is just as important as how you keep it. Create a system—digital folders, physical files, whatever works—and save every relevant document the moment you get it. Waiting until tax season is a recipe for disaster.

Here’s a no-nonsense checklist of what you absolutely must hang on to:

- All Income Records: Every single Form 1099-NEC and 1099-K, all client invoices, and screenshots or records of every deposit into your business account.

- Proof of Business Expenses: Every last receipt. I mean it. Keep digital and paper copies of everything from software subscriptions and office supplies to client lunches and travel costs.

- Bank and Credit Card Statements: Your monthly business account statements are your backup. They provide a complete history that verifies your income and expense logs.

- Vehicle Mileage Logs: If you drive your car for work, you need a detailed log. Note the date, the purpose of the trip, and the total miles driven. There are apps that make this nearly automatic.

- Home Office Expense Records: Planning to claim the home office deduction? You'll need records of your rent or mortgage interest, utilities, property taxes, and home insurance.

Keeping these documents organized is non-negotiable. The IRS requires you to keep records for at least three years from the date you file your return. A good system makes this a complete non-issue. Building this habit from day one will completely change your experience with self-employment taxes.

Mastering Quarterly Estimated Tax Payments

When you're self-employed, there's no employer taking care of taxes for you. Suddenly, you're the payroll department. That means you’re on the hook for sending the government its share of your income throughout the year, and that’s done through quarterly estimated tax payments.

Ignoring this is one of the fastest ways to get into trouble with the IRS. Come April, you could be staring down a massive tax bill plus some painful underpayment penalties. The whole point is to pay your expected tax bill in four smaller chunks instead of one giant, anxiety-inducing lump sum.

Think of it as a "pay-as-you-go" system for your income and self-employment taxes. It keeps your cash flow predictable and prevents that dreaded financial shock when you file. Generally, if you think you'll owe $1,000 or more in tax for the year, you need to be making these payments.

So, How Much Do I Actually Owe?

This is the big question. To figure it out, the IRS gives you Form 1040-ES, Estimated Tax for Individuals. Don’t worry, you don’t actually file this form—it’s just a worksheet to help you do the math.

You’ll need to forecast your total income for the year, subtract all your business deductions to figure out your net profit, and then factor in any other income, adjustments, or tax credits you might have. It sounds like a lot, but it’s really just about making an educated guess.

A solid rule of thumb for many freelancers is to set aside 25-30% of your net business income for taxes. This ballpark figure usually covers your 15.3% self-employment tax (for Social Security and Medicare) and your estimated federal and state income taxes.

My Two Cents: Guessing your income is the trickiest part, especially when your business has its ups and downs. It's always better to aim a little high and get a refund than to come up short and get hit with penalties. You can always adjust your payment in a later quarter if your income changes dramatically.

This whole process is a major departure from life as a W-2 employee. The IRS takes compliance seriously, too. In fact, over 80% of recent IRS Chief Counsel cases involving the self-employed were about tax enforcement and litigation, often stemming from issues like these. You can dig into recent government reports on tax compliance to see just how common these challenges are.

What If My Income Is All Over the Place?

Welcome to the club! Very few freelancers have perfectly steady income. One quarter might be a feast, the next a famine. The IRS gets this and offers a solution: the annualized income installment method.

Instead of paying the same amount each quarter, this method lets you adjust your payment based on what you actually earned in that specific period. It’s a game-changer for managing cash flow.

Let’s look at an example:

Imagine a freelance graphic designer lands a huge project and makes $25,000 in the first quarter, but things slow down and she only earns $5,000 in the second.

- Standard Method: She'd pay an equal estimated amount each quarter, which could be a real squeeze during that slow second quarter.

- Annualized Method: Her first payment would be much larger, reflecting her big earnings. Her second payment would be tiny, matching her lower income. This keeps her tax payments in sync with her actual cash flow.

The Deadlines You Can’t Miss (And How to Pay)

Circle these four dates on your calendar in bright red ink. Missing them can lead to penalties, even if you pay everything you owe by the April filing deadline.

Quarterly Estimated Tax Due Dates:

- April 15: For income earned Jan 1 – Mar 31

- June 15: For income earned Apr 1 – May 31

- September 15: For income earned Jun 1 – Aug 31

- January 15 (of the next year): For income earned Sep 1 – Dec 31

A quick heads-up: If a due date lands on a weekend or holiday, your payment is due the next business day.

The good news is that paying is easier than ever. Forget writing checks and running to the post office. The best ways to pay are online:

- IRS Direct Pay: A free and super secure way to pay straight from your bank account.

- EFTPS (Electronic Federal Tax Payment System): Another free government service. The big advantage here is you can schedule all your payments in advance. Set it and forget it.

- Debit/Credit Card: You can also pay online, by phone, or with the IRS2Go mobile app. Just be aware that third-party processors will charge a fee.

Making these four payments a non-negotiable part of your business routine is the key. It turns a scary, once-a-year tax monster into a predictable, manageable quarterly habit.

Uncovering Every Business Deduction You Deserve

When it comes to your taxes, deductions are your best friend. Every legitimate dollar you spend on your business is a dollar that the IRS can't tax. The more of these you track and claim, the lower your taxable income will be. It really is that simple.

Most freelancers know to write off the big-ticket items—a new computer, web hosting, maybe some advertising. But the real magic, and the real savings, happens when you dig into the smaller, everyday expenses you might not even realize count.

This isn't just a minor detail; it's a critical part of being self-employed. With around 25.9 million nonemployer businesses operating in 2023, according to the U.S. Census Bureau, the freelance economy is massive. Yet, IRS data suggests that 15% to 20% of self-employed filers run into issues, often stemming from how they handle their expenses. You can see the full scope in the 2023 Nonemployer Statistics report. Nailing your deductions is your best defense.

The Home Office Deduction, Demystified

This is one of the most powerful deductions out there, but it's also one that people often get wrong or are too scared to take. If you have a dedicated space in your home that you use regularly and exclusively for your business, you can write off a chunk of your household expenses.

You’ve got two ways to do this, and the best choice really depends on your specific situation.

- The Simplified Method: This is the easy-peasy, no-math-required option. The IRS lets you take a flat $5 per square foot for your office space, capped at 300 square feet. That gives you a maximum deduction of $1,500. No need to save utility bills or calculate percentages.

- The Actual Expense Method: This one takes a bit more work, but it can often lead to a much bigger deduction. First, you figure out what percentage of your home your office occupies (for example, a 150-square-foot office in a 1,500-square-foot apartment is 10%). Then, you can deduct that percentage of your actual home-related costs, like rent, mortgage interest, utilities, and insurance.

If your rent or mortgage is high, the extra effort of the actual expense method almost always pays off in a bigger tax break.

Turning Your Car Into a Tax Write-Off

Do you drive to meet clients, pick up supplies, or travel between job sites? If so, your car is more than just a ride—it’s a source of valuable deductions. Just like the home office, there are two ways to calculate it.

- Standard Mileage Rate: For 2024, the IRS has set the rate at 67 cents per mile for business travel. You just need to keep a simple log of your business miles, multiply by the rate, and you’re done. You can also add any business-related parking fees and tolls on top of that.

- Actual Expense Method: With this method, you track everything you spend on your car for the year—gas, oil changes, insurance, repairs, depreciation, the works. You then calculate the percentage of time you used your car for business and deduct that portion of your total costs.

A quick heads-up: The IRS is very clear that commuting miles—the drive from your home to your main office or workplace—are never deductible. The key is tracking trips made specifically for your business activities.

Digging Deeper: The Deductions Everyone Misses

Okay, this is where you can seriously move the needle on your tax bill. So many self-employed people leave money on the table simply because they don't realize what they can legally claim.

To see what I mean, let's compare some of the standard write-offs with their often-forgotten cousins.

Common vs. Overlooked Business Deductions

Most people grab the obvious deductions, but the real savings are often hiding in plain sight. Here's a look at common expenses versus some equally valid but less-claimed ones you might be missing.

| Deduction Category | Common Example | Often-Overlooked Example |

|---|---|---|

| Technology | New laptop or monitor | Monthly software-as-a-service (SaaS) subscriptions (e.g., Adobe Creative Cloud, project management tools) |

| Professional Growth | A major industry conference | Online courses, workshops, relevant books, or industry magazine subscriptions |

| Financial Costs | Accounting software fees | Monthly business bank account fees or credit card processing fees from Stripe or PayPal |

| Insurance | Business liability insurance | Self-employed health insurance premiums, which are a powerful above-the-line deduction |

Think about how many of those "overlooked" examples apply to you. The small amounts add up fast.

Let’s zero in on a few of these gems:

- Professional Development: Anything you spend to get better at what you do is fair game. This includes online courses, a session with a business coach, industry journals, and even paid webinars.

- Health Insurance Premiums: This is a big one. If you’re self-employed and pay for your own health, dental, or long-term care insurance, you can typically deduct 100% of the premiums you paid. It's an "above-the-line" deduction, meaning it lowers your adjusted gross income (AGI) directly.

- Bank and Service Fees: Those little $15 monthly fees for your business checking account? Deductible. The 2.9% that payment processors take from every transaction? Also deductible. Track them!

The QBI Deduction: A Tax Break You Can't Ignore

Last but not least, we have to talk about the Qualified Business Income (QBI) deduction. This is one of the most significant tax breaks for small businesses to come along in years.

In a nutshell, it allows many freelancers and small business owners to deduct up to 20% of their business income right off the top. The rules can get a little tricky, with income limits and specific guidelines depending on your profession. The good news is that most tax software handles the calculation for you. But you need to know it exists to make sure you're actually getting it.

Putting It All Together on Your Tax Return

Alright, you’ve spent the year tracking income, hoarding receipts, and sending your quarterly payments off to the IRS. Now for the final push: getting it all onto the official forms. This part can feel like the final boss battle, but really, it's just about plugging the numbers you've already organized into the right spots.

There's a natural flow to it. You’ll tackle Schedule C first, then use that to fill out Schedule SE, and finally, carry the key numbers over to your main Form 1040. Once you see how they connect, the whole process becomes much less intimidating.

From Your Records to Schedule C

Think of Schedule C, Profit or Loss from Business, as your business's annual report card for the IRS. It’s where you lay out everything you earned and everything you spent to earn it.

You'll start by reporting your total business income at the top. This isn't just the amounts from your 1099s; it's every dollar that came in, whether from checks, cash, or payment apps like Venmo or PayPal.

Next is where your diligent record-keeping really shines. You’ll list out your categorized expenses on the designated lines—advertising, office supplies, travel, you name it. Got an expense that doesn’t quite fit? No problem, that’s what the "Other expenses" section is for.

Subtract all those business expenses from your income, and you've got your net profit. This is the most important number on this form, and it's the foundation for the rest of your self-employment tax return.

Calculating Your Self Employment Tax on Schedule SE

With your net profit from Schedule C in hand, you'll carry that number over to Schedule SE, Self-Employment Tax. The sole purpose of this form is to figure out the Social Security and Medicare taxes you owe as a business owner.

The math is pretty straightforward. First, you'll multiply your net profit by 92.35%. This little adjustment gives you your "net earnings from self-employment" and accounts for the fact that W-2 employees don't pay FICA taxes on their employer's share.

Then, the 15.3% self-employment tax rate gets applied to that adjusted number. The result is your total self-employment tax for the year. This is a separate tax from your income tax, and it’s a critical piece of the puzzle.

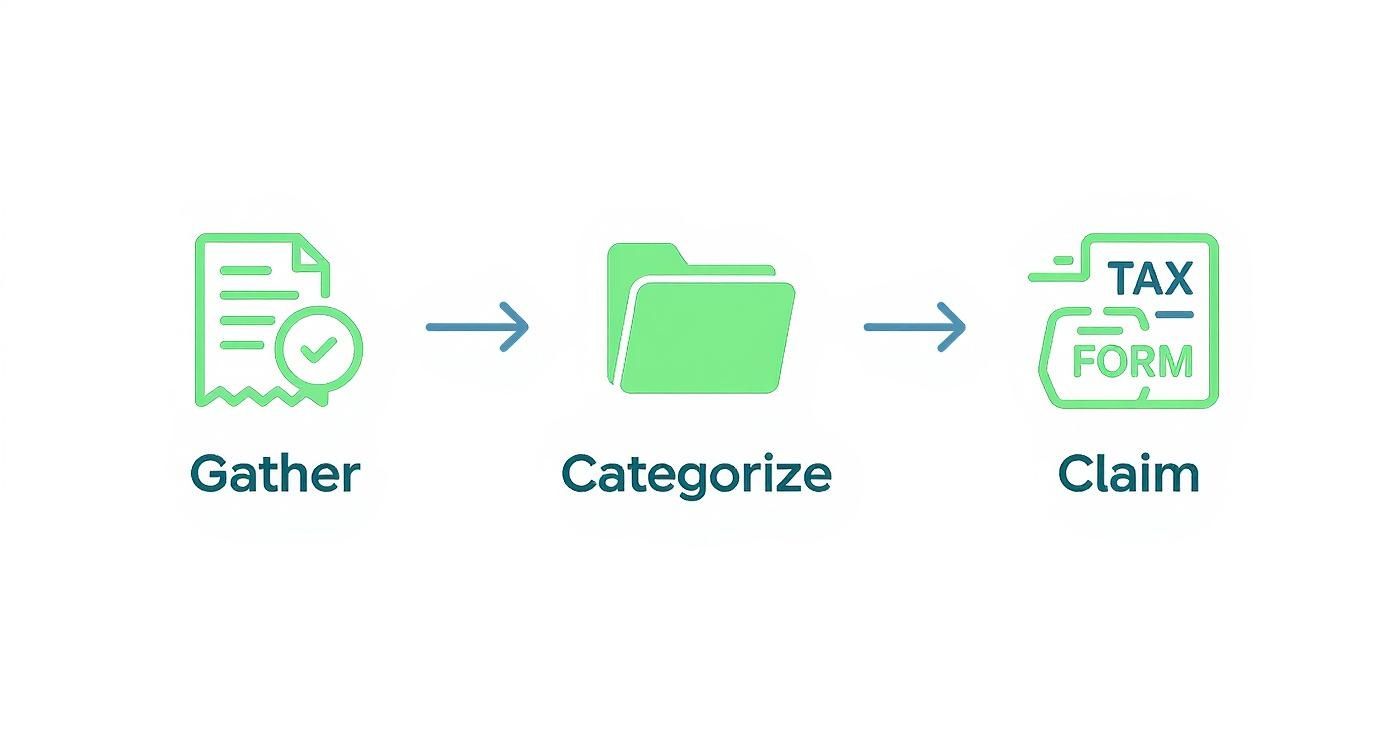

The workflow for deductions, which is the heart of your Schedule C, is all about this simple flow:

This process—gathering receipts, making sense of them, and then claiming them on your return—is exactly how you keep your tax bill as low as legally possible.

Bringing It All Home to Form 1040

Your main tax return, Form 1040, is the mothership where all these different pieces come together. The key figures you calculated on your other schedules will now find their final home here.

Here’s the rundown of how it connects:

- Your net business profit from Schedule C gets pulled onto Schedule 1 (Form 1040), where it joins any other income you might have.

- Your total self-employment tax from Schedule SE lands on Schedule 2 (Form 1040), adding to your total tax bill.

- You also get a handy deduction for one-half of your self-employment tax. You claim this on Schedule 1, and it works to lower your adjusted gross income (AGI).

Finally, you’ll enter the estimated tax payments you made during the year into the payments section of your 1040. The government subtracts those payments from your total tax bill, and that’s how you find out if you owe a bit more or if you’re getting a refund.

Expert Tip: Tax software is your best friend here. While it’s smart to understand how the forms work, a good program like TurboTax (or the software used by a professional) will handle the math and transfer the numbers between forms for you. This dramatically cuts down on the risk of a simple but costly calculation error.

Don't Forget Your State and Local Obligations

While federal taxes get all the attention, you can't ignore your state and local responsibilities. For most states with an income tax, your federal AGI is the starting point. This means your Schedule C net profit has a direct impact on how much you owe your state.

And if you’re in a place like New York City, it gets even more complicated. On top of NYS income tax, you could be on the hook for a local Unincorporated Business Tax (UBT). These rules vary wildly from one city and state to the next, so it’s critical to research your local obligations or talk to a tax advisor who knows the regional ins and outs. Staying compliant here is non-negotiable.

Knowing When to Hire a Tax Professional

DIY tax software is incredibly powerful, but it’s important to understand what it can’t do. It’s great at plugging numbers into forms, but it’s not a strategic financial partner. For many freelancers just starting out, handling your own taxes is perfectly fine. But there comes a point where going it alone costs you more than you save.

Think of it less as giving up and more as making a strategic business decision. As your business gets more complex, so do your taxes. That simple Schedule C can quickly spiral into a tangle of multi-state filings, entity choices, and retirement planning that software just isn't built to handle with any real foresight.

Key Triggers for Seeking Expert Advice

How do you know when you've hit that tipping point? A few business milestones should be your signal to start looking for a pro. If any of these sound familiar, it’s probably time to make the call.

- You formed an LLC or S Corp: The second you move beyond being a sole proprietor, the rulebook changes. A tax expert helps you navigate the new compliance requirements, figure out payroll (even if you're the only employee), and confirm if the entity you chose is actually saving you money.

- You earned income in multiple states: This is a big one. Working with clients in different states brings a whole world of State and Local Tax (SALT) headaches. A professional who understands multi-state tax issues, especially in complex areas like the NYC/NYS region, is essential to avoid mistakes and penalties.

- You receive a notice from the IRS: Nothing makes your heart sink faster than an official envelope from the IRS. Don’t panic and don’t ignore it. A CPA or Enrolled Agent can act as your representative, speak their language, and guide you through the process to get it resolved.

The real value of a tax pro isn't just about filing what's already happened. It's about proactive, year-round planning to minimize your future tax burden, something software can't do.

Hiring a professional is about more than just getting your annual return filed correctly. It’s about getting strategic advice, having support if you're ever audited, and buying back your time and peace of mind. It frees you up to focus on growing your business, knowing the financial side is in expert hands.

Frequently Asked Questions About Self-Employment Tax

When you're navigating self-employment taxes for the first time, a few questions always seem to pop up. Let's tackle some of the most common ones I hear from freelancers and independent contractors to clear up any confusion and get you filing with confidence.

How Do I Handle Both a W-2 Job and Freelance Income?

Juggling a day job and a side hustle is common, and the tax filing is more straightforward than you might think. Your W-2 income from your employer gets reported on your Form 1040 just like it always has.

For your freelance work, you'll track all your income and expenses on a Schedule C. The net profit from your business then flows from Schedule C onto your personal tax return, combining with your W-2 wages to determine your total taxable income.

One important detail to watch is the Social Security tax. The 12.4% Social Security component of self-employment tax has an annual income cap. Your W-2 earnings count towards this limit first. Good tax software handles this automatically, so you won't overpay.

Do I Need to Pay Estimated Taxes If I Barely Made Anything?

This is a great question. The IRS has a simple rule of thumb: you generally need to pay estimated taxes if you expect to owe at least $1,000 in tax for the year.

If you're just starting out and your net profit is pretty small, you might fly under that threshold. In that case, you can probably skip the quarterly payments for now.

That said, never just assume. The safest bet is to run the numbers on the Form 1040-ES worksheet. It’s far better to spend a few minutes confirming you don't owe than to get hit with an underpayment penalty later.

What's the Difference Between an LLC and a Sole Proprietorship for Tax Filing?

For a one-person business, the tax filing process is often identical for both.

-

A sole proprietorship is the default structure. You and your business are one and the same for tax purposes. You report everything on your personal Schedule C. Easy.

-

A single-member LLC (Limited Liability Company) is a legal structure, not a tax one. Its main purpose is to create a legal shield between your business debts and your personal assets. By default, the IRS considers a single-member LLC a "disregarded entity," which is a fancy way of saying it's taxed exactly like a sole proprietorship—using a Schedule C.

So, for most freelancers, the choice between the two is about legal protection, not a different tax filing experience.

At Blue Sage Tax & Accounting Inc., we turn complex tax questions into clear, actionable answers. If you need proactive planning that goes beyond the basics, visit us at bluesage.tax to see how we can help.